Despite softer labor conditions, the US economy enters 2026 on solid footing, with growth expected to remain in the 2.0% to 2.5% range. While inflation remains above trend, wage growth continues to outpace consumer prices, helping sustain household spending and extend the expansion. Against this backdrop, global central bank easing is expected to pause as fiscal spending and economic resilience keep long‑term yields anchored to policy expectations, with US rates following a familiar midterm‑year pattern of early strength and late‑year decline. With yields elevated but spreads tight, we view 2026 as an “income” year for bonds — where carry, sector selection, and cash‑flow generation drive returns. In this environment, high‑quality sectors such as Agency MBS remain compelling, supported by still‑attractive spreads and a market increasingly focused on income rather than aggressive rate positioning.

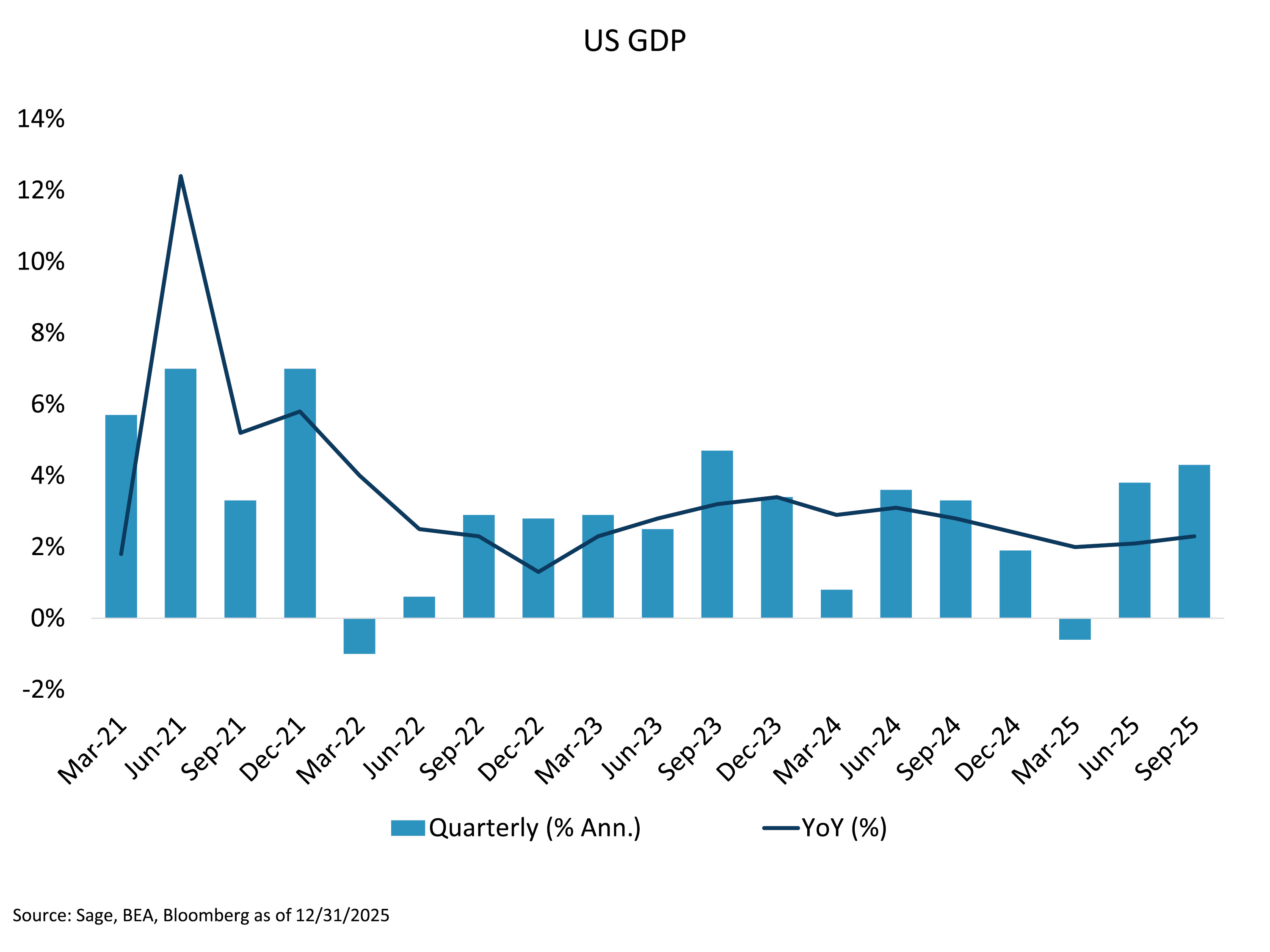

The US Economy Remains in Expansion, Despite Labor Weakness and Tariff Shock

Quarterly GDP bars and YoY growth around ~2.5% over the past three years point to a continued expansion backdrop into 2026. Even with labor soft spots and tariff-related noise, easier monetary policy and expansionary fiscal policy should keep growth supported. In short, we see a steady-growth baseline that anchors our fixed income assumptions.

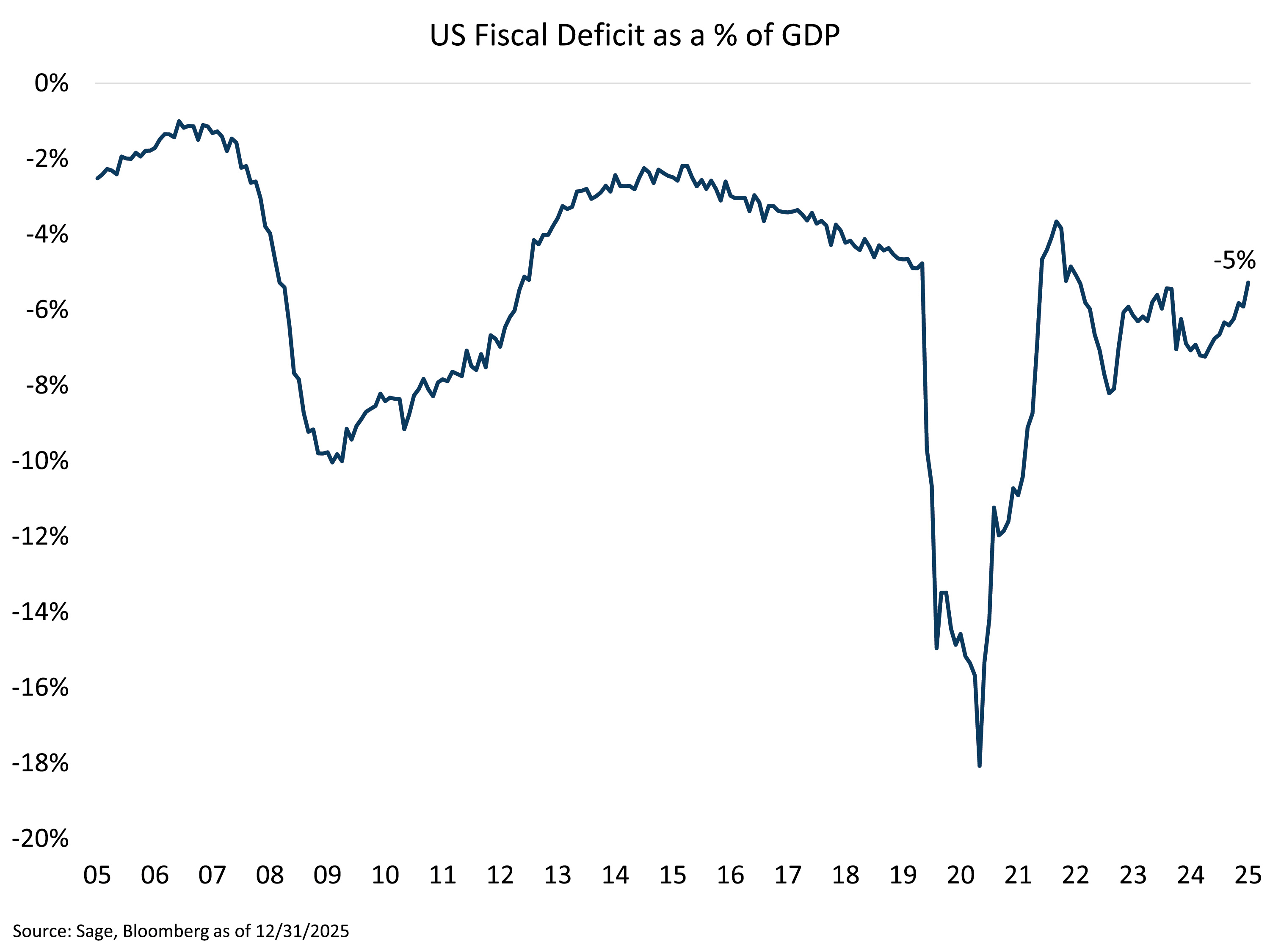

Slight Improvement for Fiscal Deficit Going into Midterm Election Year

After widening to ~7% of GDP, the US fiscal deficit improved to ~5% in 2025, reducing — but not removing — fiscal vulnerabilities. Midterm-year dynamics could reintroduce risks via “stimulus checks” or other spending pledges, potentially reversing recent improvement. It’s too early to call the final fiscal stance, but we are mindful of policy optionality and headline sensitivity.

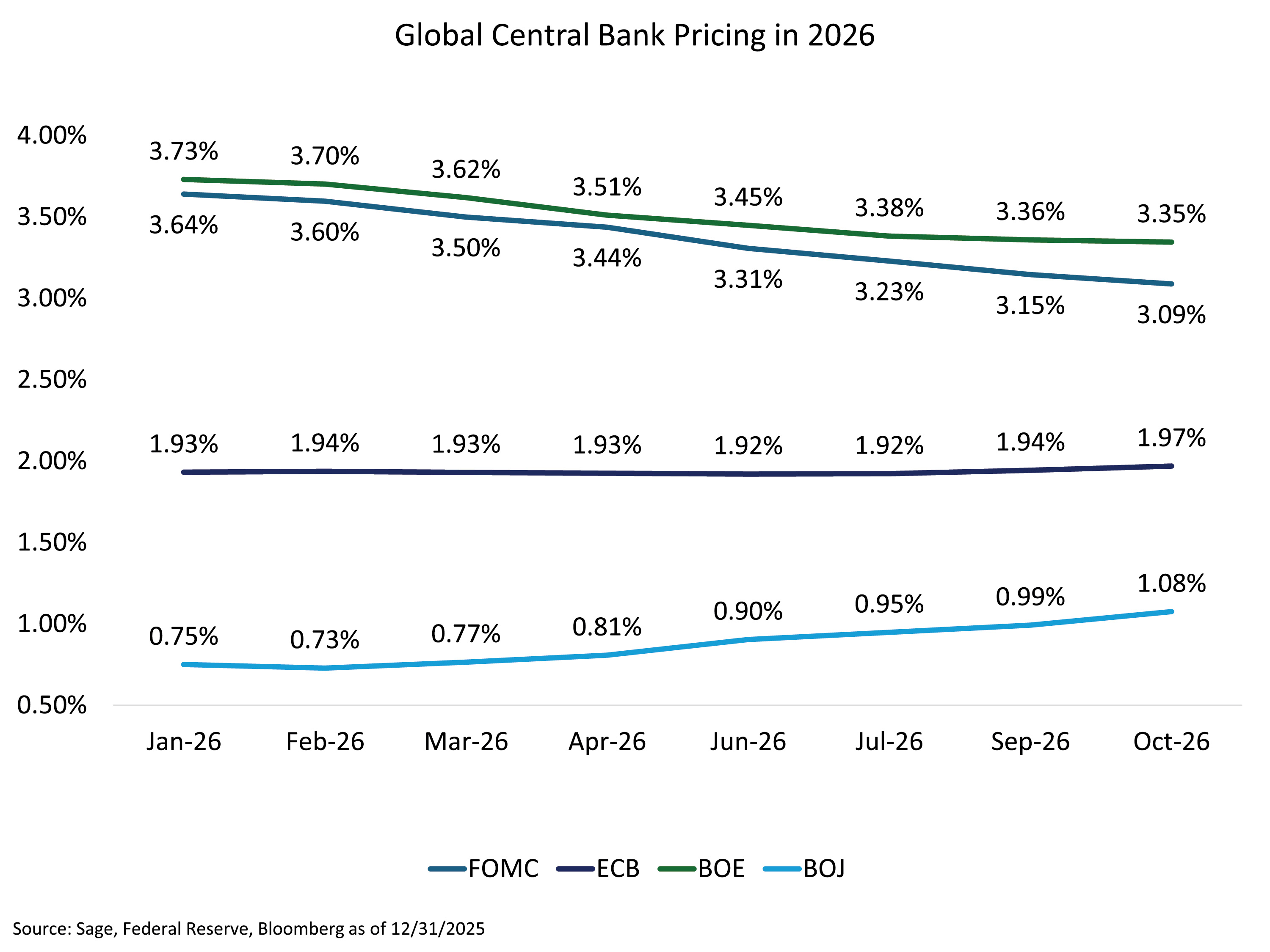

The Era of Aggressive Rate Cuts Is Over According to the Market Implied Policy Path

Market-implied paths for major developed market central banks through 3Q26 suggest a more balanced phase: the ECB pausing, the BOJ hiking, and modest cuts (~50 bps) from the BOE and the Fed this year. With robust growth and ongoing fiscal deficits, markets are pricing an end to the aggressive cutting cycle. For fixed income, this supports an “income-first” approach over chasing large rate rallies.

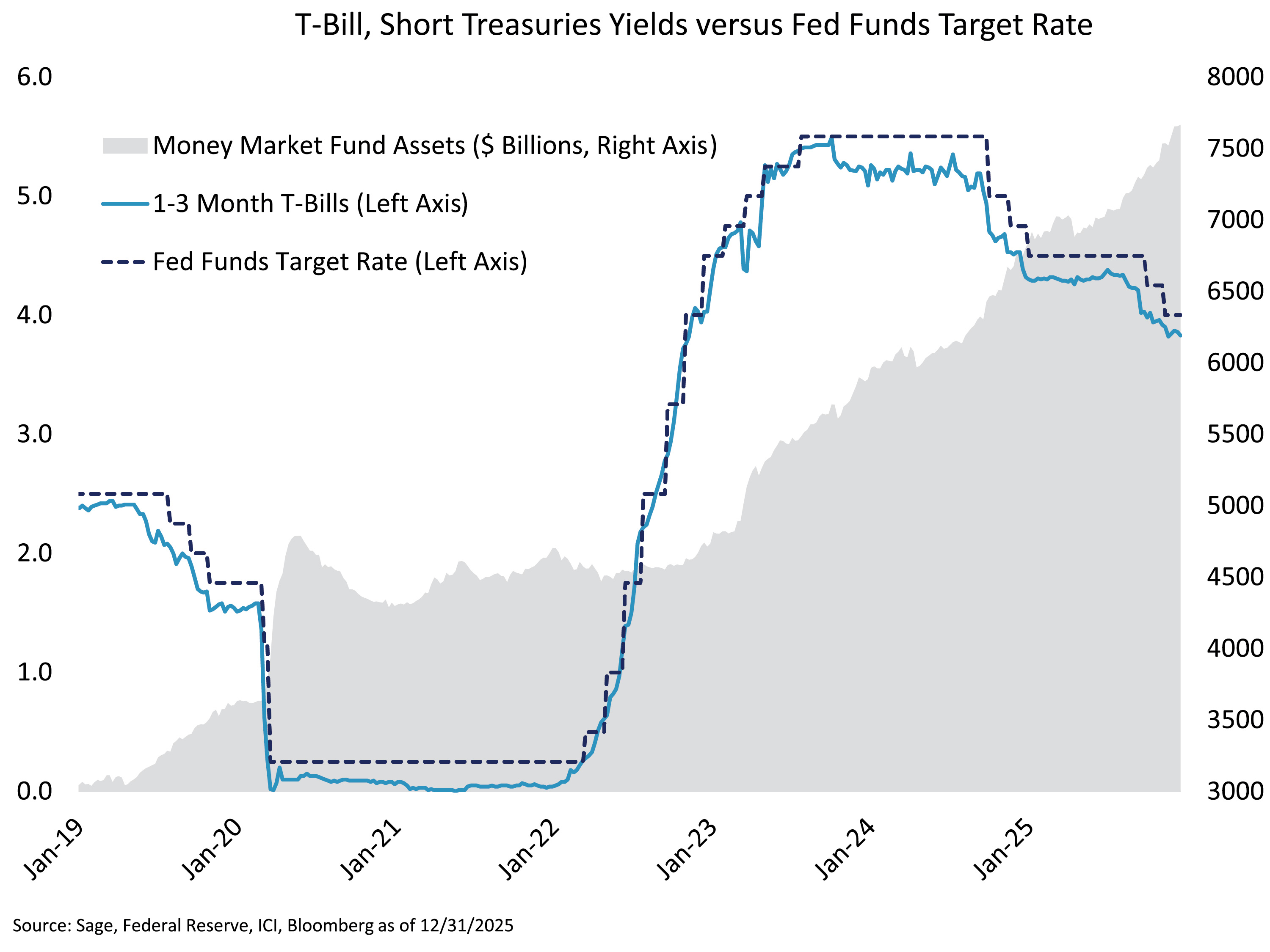

Declining Money Market Yields Amid Record Cash Could Spur Reallocation

Record money market assets (~$7.6T) and T‑bill yields tracking the fed funds rate lower set the stage for a gradual rotation out the maturity/risk spectrum as cash income compresses. As savings rates decline, the marginal bid for duration and spread assets should strengthen, providing a technical tailwind for core fixed income allocations.

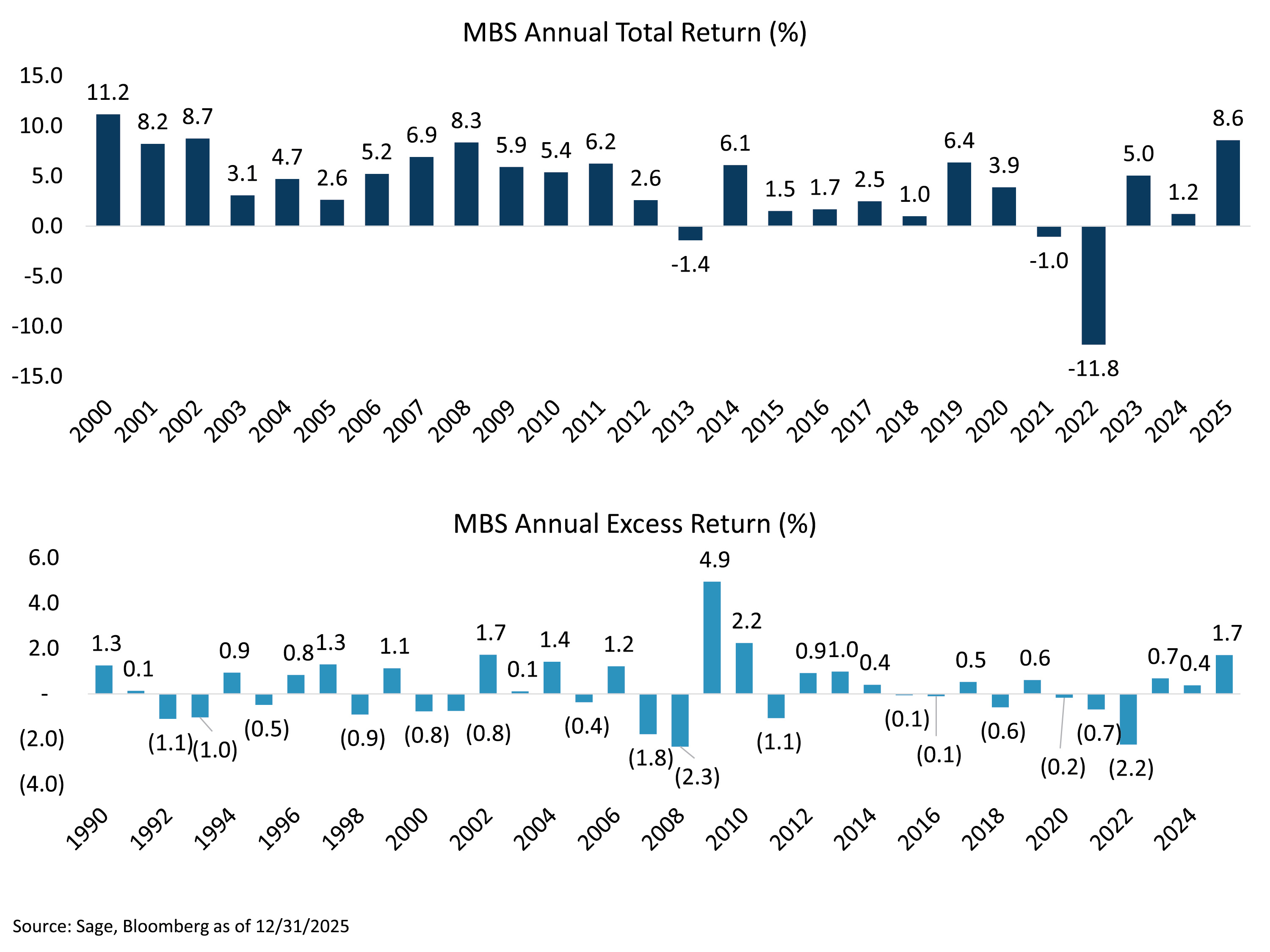

Agency MBS Posted the Best Total Return Since 2002, Best Excess Return Since 2010

Agency MBS was a standout performer in 2025, and nominal spreads remain historically attractive. Given carry, high-quality collateral, and still-compelling valuations, we see scope for continued outperformance versus broad fixed income — supporting an overweight to Agency MBS in portfolios where quality and income are paramount.