Market Outlook

Fixed income markets have largely interpreted the Iran war as a near‑term, supply‑driven inflation event. In Q1, yields moved higher and curves flattened as markets pushed expected Fed easing out of 2026, with the 2s10s curve flattening by roughly 20 basis points. Near‑term inflation expectations repriced sharply, with one‑year TIPS‑implied inflation rising above 5%, though longer‑term expectations remained anchored near 2.25%. Most core investment‑grade markets delivered flat total returns, as higher yields were offset by strong income carry. Credit modestly underperformed amid risk‑off sentiment and supply pressures, with spreads widening by roughly 10 basis points. Higher‑quality sectors outperformed, including agency MBS, which generated small positive returns (+0.4%) for the quarter. Among non‑core markets, income partially offset spread widening in high yield, resulting in modest losses (-0.3%). Emerging market debt lagged further (-2%), while pressures in private credit were most evident in business development companies, with BDC fixed income down 1% and BDC equities down roughly 10%.

Our view into 2026 was to lean on income generation, but more carefully with a defensive credit posture, a focus on selection, and a higher quality bias. This has been the right call as income generation has offset rate volatility and spreads have moved higher from historical lows. Despite uncertainty with Iran, the forward return outlook into Q2 looks attractive given an aggressive repricing in yields and even higher income carry. Any easing of hostilities in the Middle East would likely bring oil prices lower, relieve near‑term inflation pressure, and reopen the discussion around rate cuts. Under incoming Fed Chair Kevin Warsh, that would put policy flexibility back on the table. In that environment, intermediate‑maturity bonds are well positioned to benefit, offering both durable income today and potential capital appreciation if rate expectations normalize. In our view, the 1‑to‑10‑year maturity range offers the best risk‑reward profile in fixed income today. This part of the curve has fully priced out future Fed cuts while assuming a high level of short‑term inflation pressure.

Our broad positioning themes of income generation and defensive credit risk remain intact, though recent volatility in yields and spreads has created opportunities to tweak tilts. Where duration was skewed to the lower end of benchmarks earlier in the year, we have reversed course and moved duration modestly above benchmarks as Fed pricing has become overly aggressive. Within our sector allocation, credit remains a balance between spreads that are still too tight and yield levels that are attractive and supportive of continued inflows. Our response has been to maintain full credit exposure to harvest yield, while taking a defensive posture within credit. This includes a bias toward the front end of the curve and issuer and sector selection aimed at avoiding private credit risk and AI‑related disruption. We continue to overweight MBS, which we view as offering the best risk‑reward profile within core fixed income. Within core plus strategies, we maintain moderate and well‑diversified exposure to non‑core sectors. We reduced high‑yield and loan exposure in the second half of 2025, reallocating toward preferred stock and higher‑income securitized exposure.

Fixed Income Allocations & Recent Changes

| Sector | Positioning & Recent Changes |

|---|---|

| Duration/Curve | US Treasury yields moved higher over March as resilient economic data and renewed inflation concerns pushed investors to reprice the policy outlook. The escalation of the Iran war added a geopolitical risk premium to the front end of the curve, while rising oil prices reinforced fears that energy-driven inflation could reaccelerate. As a result, expectations for Federal Reserve easing were largely erased, with markets shifting toward a higher-for-longer stance. Looking ahead to the coming quarters, our base case is that the Fed delays any near-term policy changes as energy-related inflation works its way through the economy. While core inflation has continued to improve, higher fuel costs and upstream pricing pressures make it difficult for policymakers to move quickly, keeping yields range-bound but biased higher until inflation risks are better contained. |

| Investment Grade Credit | After investment grade spreads widened by nearly 20 basis points from their 20‑plus‑year tights, they have settled equidistant from the wides and the tights of the year. At current levels, valuations are not particularly compelling. Recent volatility has been driven by uncertainty surrounding the Iran conflict as well as concerns about private credit. Yields remain elevated, which is supportive, and 48 consecutive weeks of positive inflows underscore that yield continues to matter. We believe it makes sense to stay invested, but from a defensive posture — positioned to avoid private credit risk, favor hard assets that are unlikely to be disrupted by AI, and participate in AI‑related growth through non‑speculative exposures. |

| Securitized | Agency mortgages underperformed over the past several weeks, tied to rising Treasury yields and volatility resulting from the tensions with Iran. During the month of March, the MOVE Index increased from 73 to 115, widening the current coupon spread from 109 basis points to 130 basis points. Wider spreads and higher Treasury yields pushed mortgage rates up significantly, giving some relief to prepay expectations on high coupon MBS. Performance in the sector is likely to remain choppy until interest rate volatility eases; however, we believe the income compensates for the risk. We have used this opportunity to increase our mortgage overweight. Within the coupon stack we favor higher coupons for income, barbelling that exposure with lower coupons, which would likely outperform in an interest rate rally. We believe spreads will tighten in the weeks ahead, and in the meantime, carry remains king. |

| High Yield | High-yield markets in 1Q26 were shaped by pronounced sector- and quality-specific dislocations rather than broad-based credit deterioration. Notably, BBs underperformed CCCs on a total-return basis — an atypical outcome largely driven by the longer duration profile of higher-quality cohorts amid the rate selloff — which we view as a selective opportunity given the historical infrequency of such reversals. Sector dispersion was evident in the relative strength of Energy, a bifurcation within Technology, and modest weakness in Financials. Software credits rebounded sharply in March following an initial sell-off tied to AI-related disruption concerns; however, we remain cautious on highly levered issuers where accelerating AI adoption may erode competitive moats, pressure longer-term credit fundamentals, and constrain refinancing optionality. High-yield Financials lagged during the quarter amid the Iran-related stagflationary rate shock, compounded by smaller idiosyncratic factors. Overall, markets remain constructive but increasingly differentiated, underscoring the importance of disciplined, bottom‑up security selection over broad beta exposure. |

| Municipal | The municipal bond market delivered a tale of two quarters in Q1 2026, beginning with exceptional January strength driven by the January Effect before succumbing to significant rate volatility in March. The Bloomberg Municipal Bond Index ended the quarter with a -0.18% return, with the belly of the curve experiencing the worst performance. Year-to-date yield changes were substantial across the maturity spectrum, with intermediate maturities experiencing the most pronounced increases. From a credit and structure perspective, results were relatively compressed but still revealed clear leadership trends. Credit returns improved incrementally moving down the ratings spectrum, with A‑rated bonds delivering the strongest performance among traditional ratings at ‑0.03%, while AAA bonds lagged at ‑0.34% as high-grade sectors absorbed disproportionate selling pressure. Sector performance was mixed, with Transportation emerging as the top-performing subsector at 0.08%, supported by defensive characteristics, while Resource Recovery and Education represented the weakest areas of the market. |

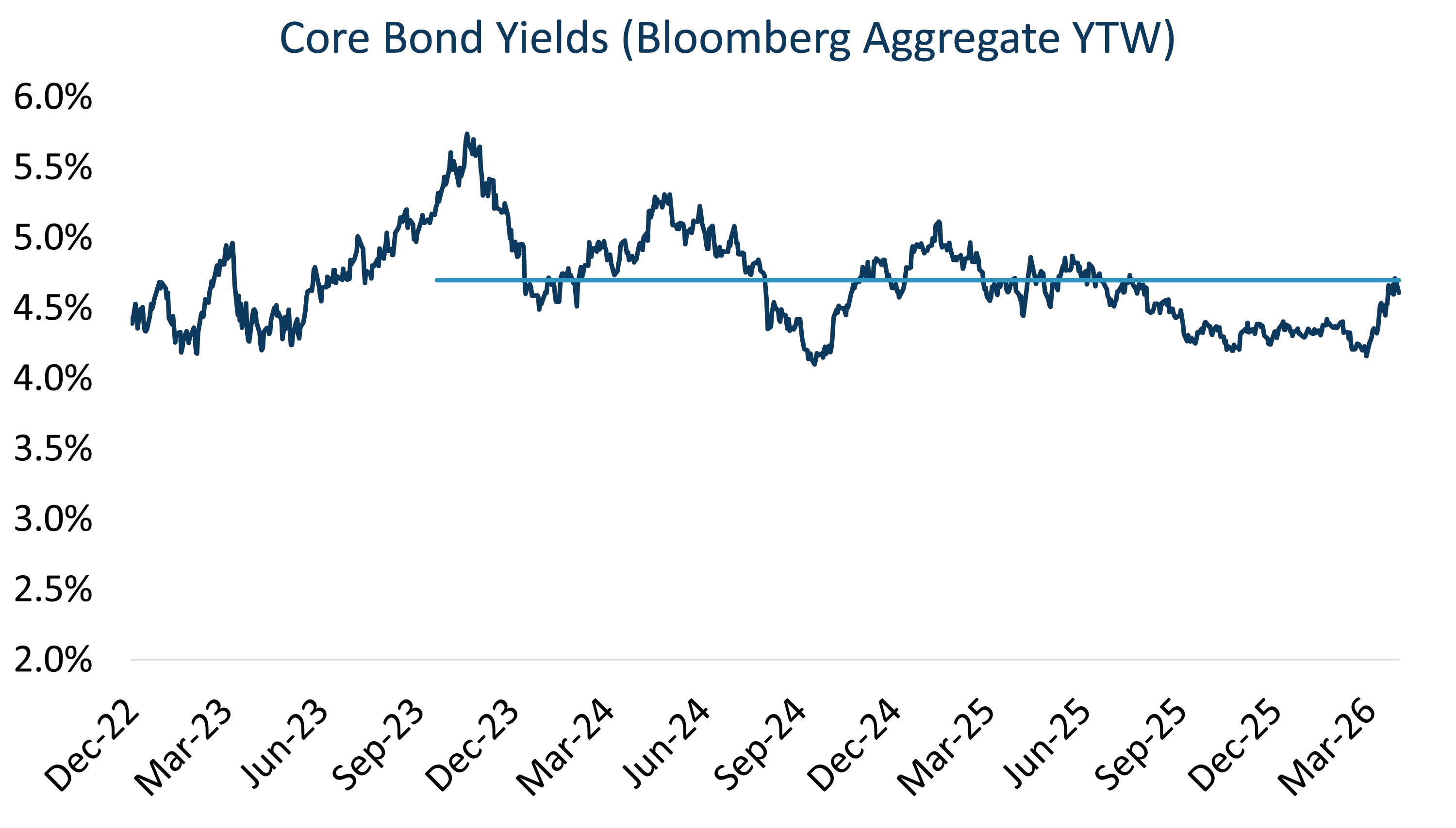

Yield Levels Are More Attractive

Core aggregate bond yields have moved back to roughly last year’s highs, reversing much of the rate rally and restoring income levels that historically have been strong entry points for long‑term investors. At current yield levels, carry and roll once again do most of the work, reducing dependence on the precise timing of rate cuts. For investors underweight duration, this reset offers an opportunity to re‑establish core exposure at yields that meaningfully compensate for uncertainty.

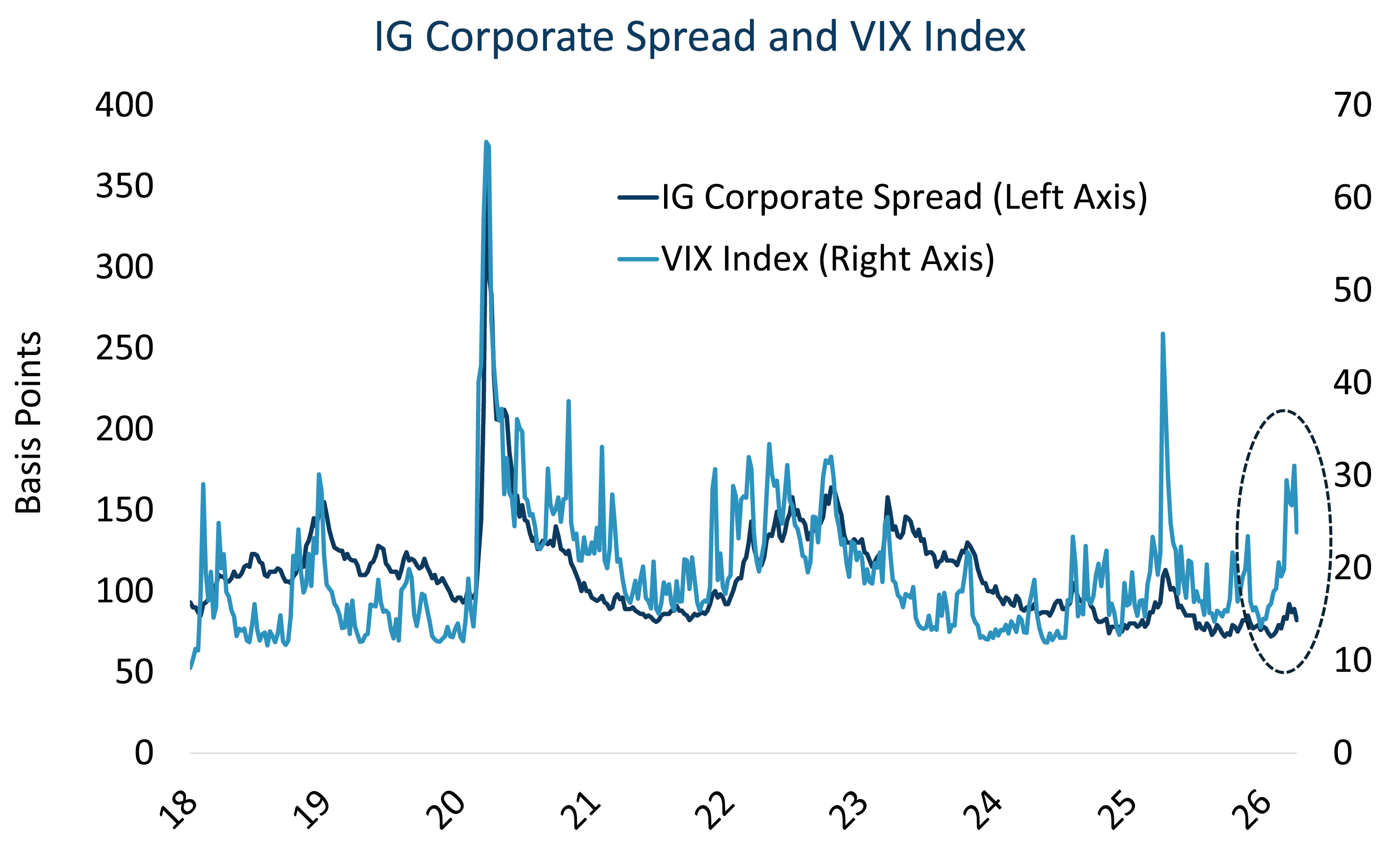

Market Volatility Has Not Spread to Credit

Unlike recent historical episodes of equity volatility, credit spreads have seen little impact. Even in the face of record supply and private credit concerns, IG spreads are at tighter levels than on February 28th when combat operations began in Iran. We attribute this to a few factors: buyers are yield-motivated and being paid to tolerate uncertainty; issuer fundamentals remain solid; and demand continues to overwhelm even heavy supply. This supports our view to hold a full allocation of credit but to do it from a defensive posture, where selection and curve positioning can garner yield but lower overall risk.