Market Outlook

Global markets struggled in the first quarter as the Iran war and resulting energy shock weighed on both equities and fixed income. Markets entered the quarter already contending with concerns around AI margins and private credit, but the escalation in Iran triggered a sharp rise in energy prices, a deeper equity correction, and higher rates driven by near‑term inflation fears. Inconsistent messaging from the Trump Administration has amplified volatility in oil prices and broader markets, though by quarter‑end the damage, while widespread, remained modest. Global equities fell 3.3% for the quarter, while US investment grade bonds were roughly flat.

The near term remains challenging for risk assets, with visibility around an easing of the Iran conflict and energy crisis remaining the key factor — and still elusive. Our base case, and the way markets have repriced so far, assumes a reasonable timeline, limited damage to growth, and only short‑term inflation effects. That keeps our medium‑term outlook constructive. A resilient US consumer remains a bedrock of the expansion. While higher gas prices will likely slow spending, it would take a more severe market correction to meaningfully impact higher‑income consumers and shift consumption into a sustained headwind. Beyond Iran, private credit and AI margin pressures remain areas of concern, but business sentiment appears to have bottomed. Productivity gains and spending outside of core AI — particularly in AI‑adjacent industries, as well as defense and energy — remain important tailwinds.

Given these views and recent equity weakness, we have adjusted our multi‑asset allocations. We have increased equity exposure across balanced accounts, funded from fixed income, and raised our US weighting relative to international markets. In the US, equity multiples have compressed while full‑year earnings expectations remain positive, supporting a rotation toward US growth equities. In fixed income, yields have moved too aggressively toward pricing hikes, creating an attractive window to add duration. Higher yields have also improved forward return expectations for core fixed income through stronger income carry. Any easing of hostilities in the Middle East would likely bring oil prices lower, relieve near‑term inflation pressure, and reopen the discussion around rate cuts. In that environment, intermediate‑maturity core bond and income-based strategies are well positioned to benefit, offering both durable income today and potential capital appreciation if rate expectations normalize. We continue to overweight MBS across income allocations, which we view as offering the best risk‑reward profile, combining attractive yields relative to credit with a higher‑quality profile. Within core plus strategies, we maintain moderate and well‑diversified exposure to non‑core sectors. We reduced high‑yield and loan exposure in the second half of 2025, reallocating toward preferred stock and higher‑income securitized exposure.

Equities vs. Fixed Income

We carry an overweight in equities vs. fixed income. Given our base case that the US will avoid a recession and benefit from supportive monetary and fiscal policy in 2026, we see relative upside potential in equities compared to bonds.

| Equity | View | Reasoning |

|---|---|---|

| US Equities | Positive | We recently moved to an overweight in US equities relative to international markets. Near-term risks appear more skewed to the upside with a multiple compression in the face of still-solid earnings outlooks, a potential fiscal boost during April tax season, and the likelihood of a scaling back of combat operations in Iran during this period. |

| Developed International | Negative | International developed markets, particularly Europe, the UK, and Japan, remain vulnerable to elevated energy prices due to their reliance on energy imports. Slowing growth in these regions could pressure returns, leading us to reduce EAFE exposure into 2Q. |

| Emerging Markets | Neutral | We maintain a neutral allocation to EM as valuations are attractive and there is growth upside in India and parts of Asia and LATAM. This is countered by structural weakness in China and elevated macro and geopolitical risks globally. |

| Style/Sector/Factor | Growth | From a style and sector perspective, we favor growth, having increased our exposure during Q1 as valuations became more attractive, and cyclicals, given their still?solid growth outlook. We have also tilted exposure toward heavy industry and power infrastructure to benefit from the capex spending theme. |

| Fixed Income | View | Reasoning |

|---|---|---|

| US Treasuries | Underweight | We are underweight Treasuries overall with a tilt toward longer-duration exposure. This is balanced with a credit allocation biased toward the front-end, to tamp down overall spread volatility. This positioning also allows us to keep modestly longer-than-benchmark duration at the portfolio level to balance our non-core risk and increased securitized exposure. |

| Investment Grade Credit | Market Weight | Market weight-type exposure still makes sense in IG credit given strong fundamentals and demand for yield but full valuations. We continue to have a tilt toward short-dated credit to enhance quality and liquidity, and we continue to diversify our overall spread risk with increased MBS exposure. |

| Securitized | Positive | We continue to like the agency mortgage sector from both a relative value and macroeconomic standpoint. Mortgages offer attractive yields to Treasuries and IG credit without the credit risk and should benefit from lower rate volatility. We have increasingly skewed exposure toward actively managed ETFs as issuer and structural selection are an important excess return driver within securitized markets. |

| Non-Core Fixed Income | Moderate | We believe a moderate allocation to non-core assets is appropriate to diversify sources of yield and return. Given tight US credit spreads and an easing Fed, we have lowered high yield and loan allocations in favor of increased preferred stock and high-income securitized exposure. |

Illustration of Themes – What Matters in 2026

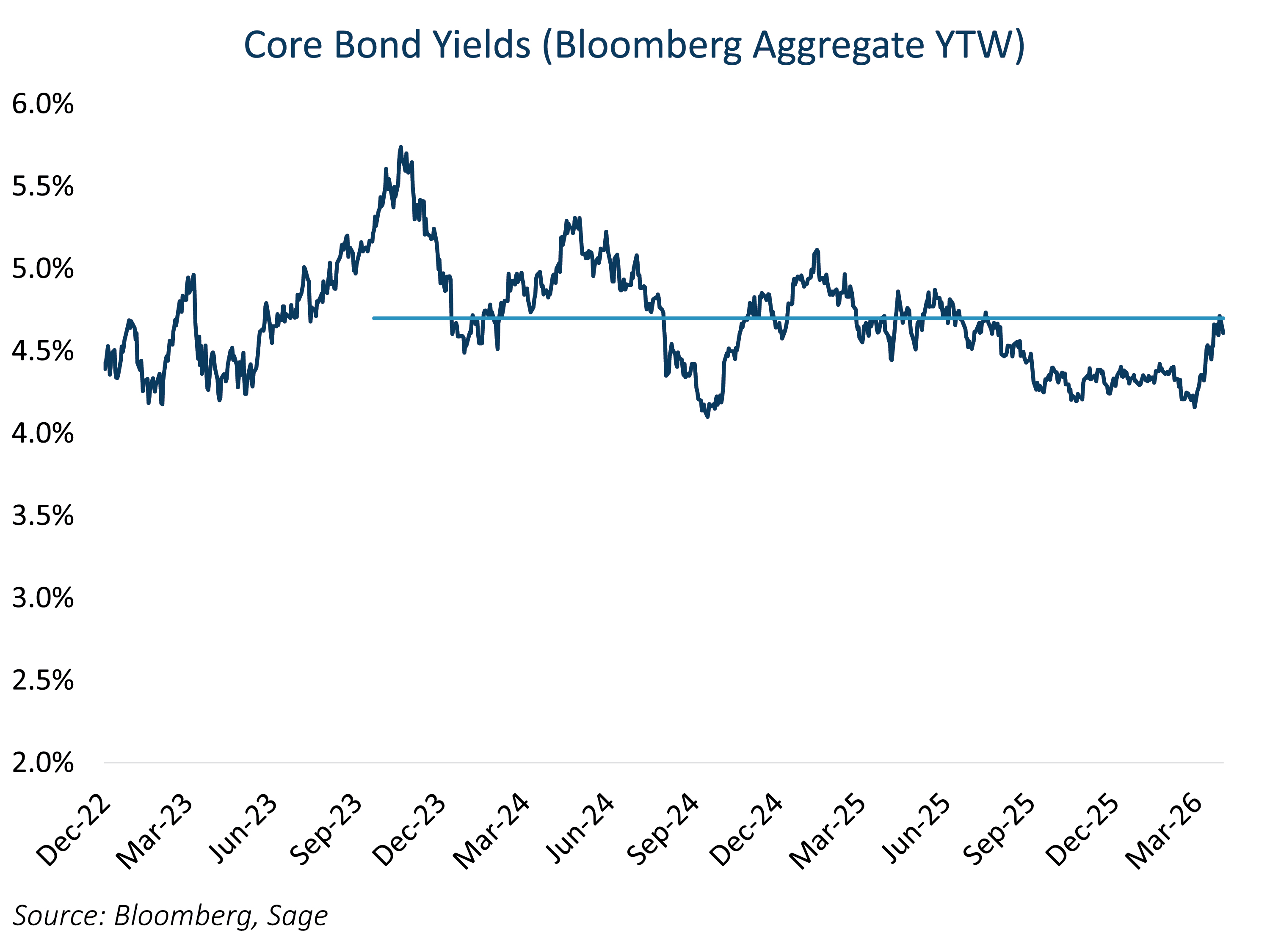

Yield Levels Are More Attractive

Despite continued uncertainty in the Middle East, the forward return outlook into Q2 appears attractive, reflecting an aggressive repricing in yields and higher income carry. Any easing of hostilities would likely bring oil prices lower, relieve near‑term inflation pressure, and reopen the discussion around rate cuts. Under incoming Fed Chair Kevin Warsh, that would put policy flexibility back on the table.

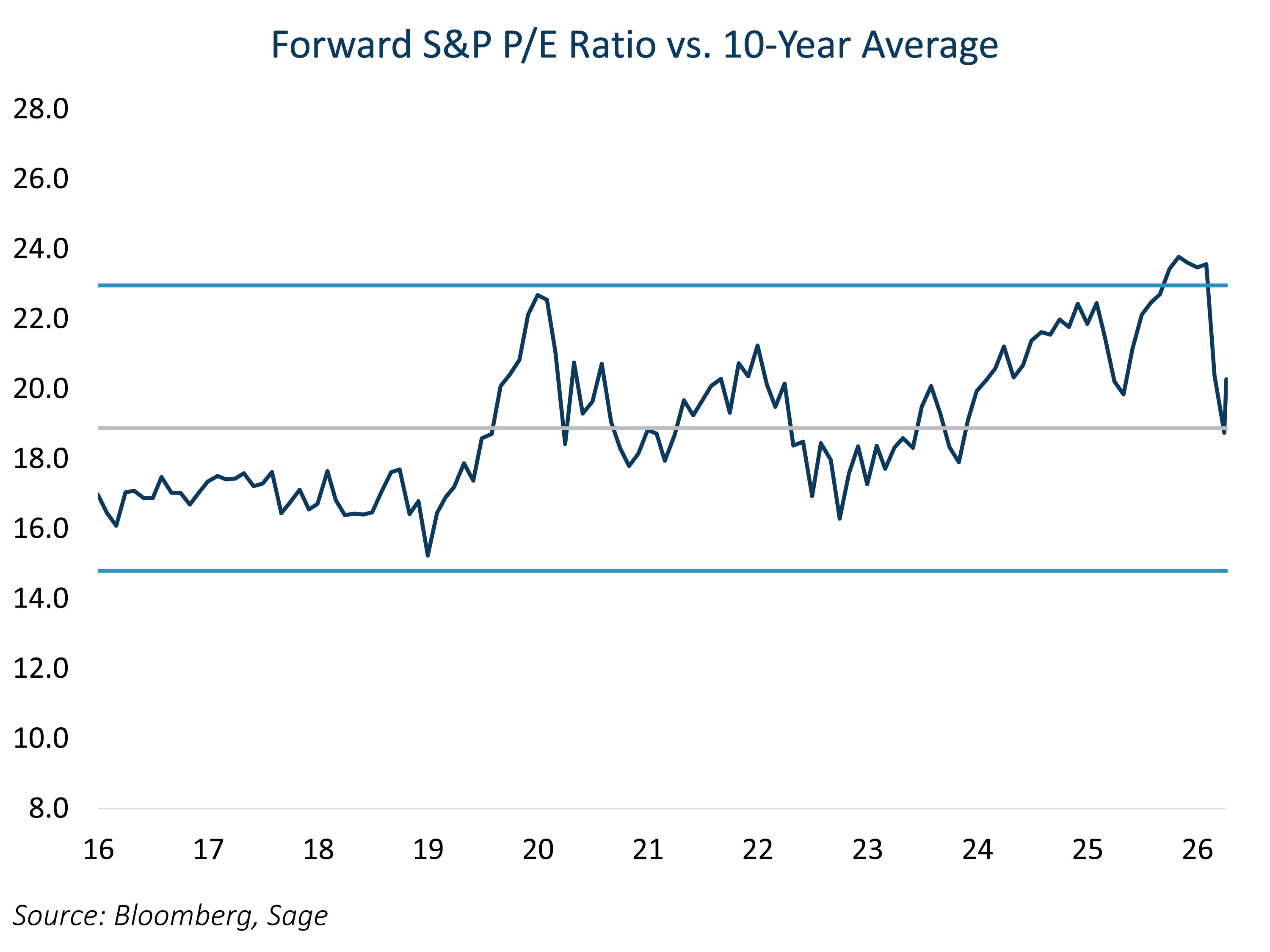

US Equity Multiples Have Also Compressed

US forward P/E multiples have compressed meaningfully, even though price declines have been relatively modest, reflecting resilient earnings expectations rather than a deterioration in fundamentals. This valuation adjustment has created an attractive window to add US equities within balanced strategies, particularly when reallocating from markets more exposed to prolonged energy and inflation headwinds.