Energy is the New Inflation Wildcard

June 16, 2025 By Sage Advisory

While recent inflation readings have been softer than expected, the more immediate inflation risk may come from rising energy prices driven by renewed geopolitical instability. Tensions between Israel and Iran have pushed oil prices higher, reminding policymakers and markets that while spot inflation is cooling, energy remains the most likely catalyst for near-term inflation surprises.

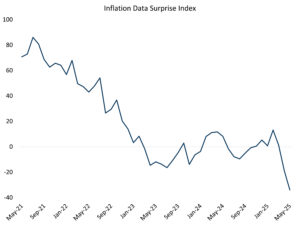

Core inflation has eased in recent months. May’s CPI came in below expectations, rising 0.08% on the month (2.35% YoY), with core CPI rising 0.13% in May (2.79% YoY). PPI has softened as well, with little sign of upstream pressures feeding into consumer prices. Most importantly for the Fed, recent inflation readings mean that core PCE should be lower than previously thought as well.

Source: Citi, Bloomberg

While tariffs can raise input costs, the muted market response and recent prints suggest these effects may take time to work through the supply chain. This reflects the narrow scope of the tariffs. Many affected goods are a small share of consumer spending, and producers may initially absorb costs. Broader disinflationary trends — inventory normalization, lower shipping costs, and weaker discretionary demand — could have offset tariff pressures.

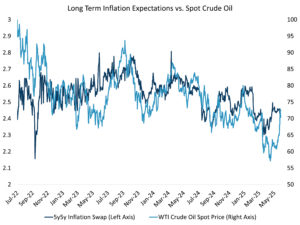

In contrast, oil’s rise introduces a more immediate inflation risk. Middle East tensions have escalated, raising concerns over crude supplies through the Strait of Hormuz. Since early May, WTI crude has climbed from a low of $55 to the low $70s. Markets are pricing in higher risk premiums as broader conflict risks rise. As we’ve mentioned in a prior Notes, the price movement of spot crude moves in-line with long-term inflation expectations. Long-term inflation expectations have not responded to the recent oil price shock, although it could be too early to call as it has been less than two trading sessions as of the writing of this Notes.

Source: Bloomberg

Oil price spikes filter into inflation quickly. Higher energy prices push up headline CPI directly and raise transportation, utility, and input costs. If oil stays elevated or climbs, inflation prints could rise by late summer, just as the Fed faces key rate cut decisions.

Markets have priced in nearly two 25 bps rate cuts through December, encouraged by softer inflation and a cooling labor market. But renewed energy volatility complicates that outlook. While the Fed has signaled that it can look past short-term energy swings, sustained price increases spilling into core inflation or expectations may force the Fed to stay on hold for longer. For now, expectations remain anchored, but another oil surge could challenge whether policy is “sufficiently restrictive.”

Recent data suggests that the US economy is absorbing tariff shocks better than feared, with price effects unfolding gradually. This gives the Fed room and keeps the disinflation narrative intact. But energy markets could change that calculus. As geopolitical risks remain, energy prices now represent the clearest upside risk to inflation. If oil continues climbing or stays elevated, the second half of 2025 may become a more complicated balancing act — resilient disinflation on one hand, and renewed energy-driven pressure on the other.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.