Rising Interest Rates: A Short Guide for ETF Investors

May 2, 2018 By Sage Advisory

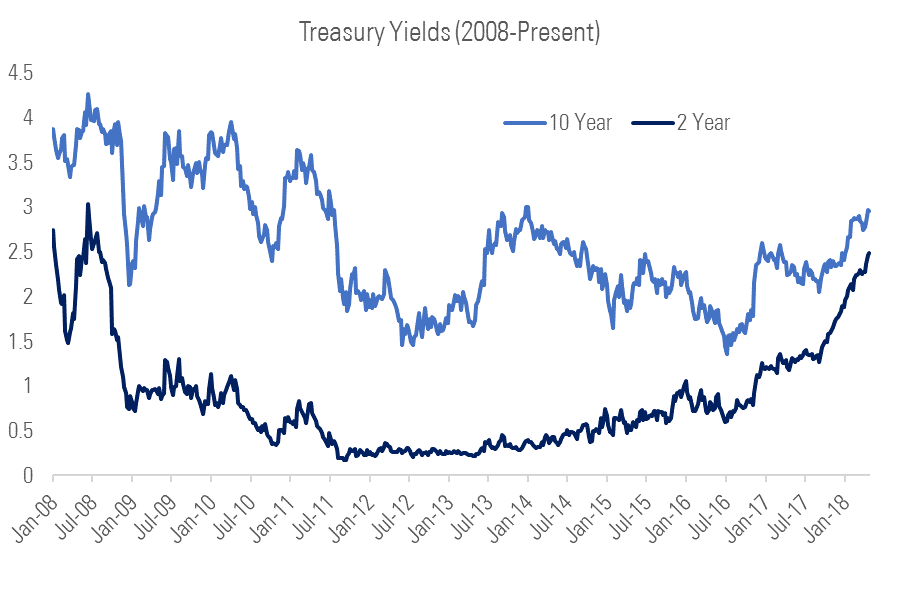

A rising tide lifts all boats, but do rising rates lift all assets? The yield on 10-year Treasury notes rose above 3% last week – the highest it’s been since 2014 – and the yield on two-year Treasury notes hasn’t been this high since the 2008 financial crisis.

When interest rates rise, many investors fear a negative effect on the economy. A combination of rising inflation, increased bond supply, and the Federal Reserve’s tightening policy have caused the recent increase in yields. In what ways could higher rates lead to lower growth, and more importantly, how should we as ETF investors position ourselves?

Higher Rates – A Risk Factor for The Economy?

Here are how higher interest rates could negatively affect growth:

- Rising interest expense for the corporate sector. Companies that finance their operations with debt incur interest expense, which drives down profit margins. According to JPMorgan, a 100 basis point increase in bond yields typically results in a 1.5% drag on S&P 500 earnings (not including financial services companies, which would see a benefit to earnings). Until recently, rates had remained relatively low since the financial crisis, and the lower interest expense has been a huge driver of corporate profit margins. Increasing rates would in theory reverse that trend. However, the impact of higher rates is mitigated by the fact that corporate debt has generally been issued at longer maturities (an average of 10-plus years) and at fixed rates, so rising interest expense is not an immediate concern at the macro level.

- Lower consumer demand due to rising interest expense for households. Higher interest expense decreases the level of disposable income, which should lower consumption and as a result, reduce GDP growth. This impact is somewhat mitigated as households have deleveraged over the past decade, and household debt service ratios remain at multi-decade lows.

How Higher Rates Negatively Affect Equities:

- Reduced value of future earnings. In its purest form, equity prices reflect the discounted future earnings of a company. Higher interest rates increase the discount rate, thereby lowering the company’s present value. If rising interest rates aren’t offset with higher top-line growth, either through higher prices (inflation) or higher volume (more demand), then equities could be in trouble as market participants price in a higher discount rate.

- Declining attractiveness of equities as earnings yields decline. When earnings yields significantly exceed bond yields, it becomes cheaper for companies to finance projects, M&A, and share repurchase programs. When the difference between earnings yields and bond yields is zero or negative, the equity-market boosting behaviors could slow or stop. With increasing bond yields and high stock valuations, that gap has been decreasing, but it still remains at above-average levels. So while it’s not a red flag yet, if the gap continues to narrow, it could drive stock prices lower.

A rising rate environment does not signal immediate danger for the economy, since the private sector has deleveraged a great deal since the crisis and the Fed has been very methodical in communicating future rate hikes. However, markets are forward-looking and investors could start to price in the effect of higher interest rates on financial assets before they actually materialize. At Sage, we believe sectors that stand to outperform from rising rates are financial services, such as banks and insurance companies; inflation-protected bonds; and the senior loan market, which provides exposure to corporate debt without the corresponding interest rate risk.

Disclosures: This is for informational purposes only and is not intended as investment advice or an offer or solicitation with respect to the purchase or sale of any security, strategy or investment product. Although the statements of fact, information, charts, analysis and data in this report have been obtained from, and are based upon, sources Sage believes to be reliable, we do not guarantee their accuracy, and the underlying information, data, figures and publicly available information has not been verified or audited for accuracy or completeness by Sage. Additionally, we do not represent that the information, data, analysis and charts are accurate or complete, and as such should not be relied upon as such. All results included in this report constitute Sage’s opinions as of the date of this report and are subject to change without notice due to various factors, such as market conditions. Investors should make their own decisions on investment strategies based on their specific investment objectives and financial circumstances. All investments contain risk and may lose value. Past performance is not a guarantee of future results.

Sage Advisory Services, Ltd. Co. is a registered investment adviser that provides investment management services for a variety of institutions and high net worth individuals. For additional information on Sage and its investment management services, please view our web site at www.sageadvisory.com, or refer to our Form ADV, which is available upon request by calling 512.327.5530.