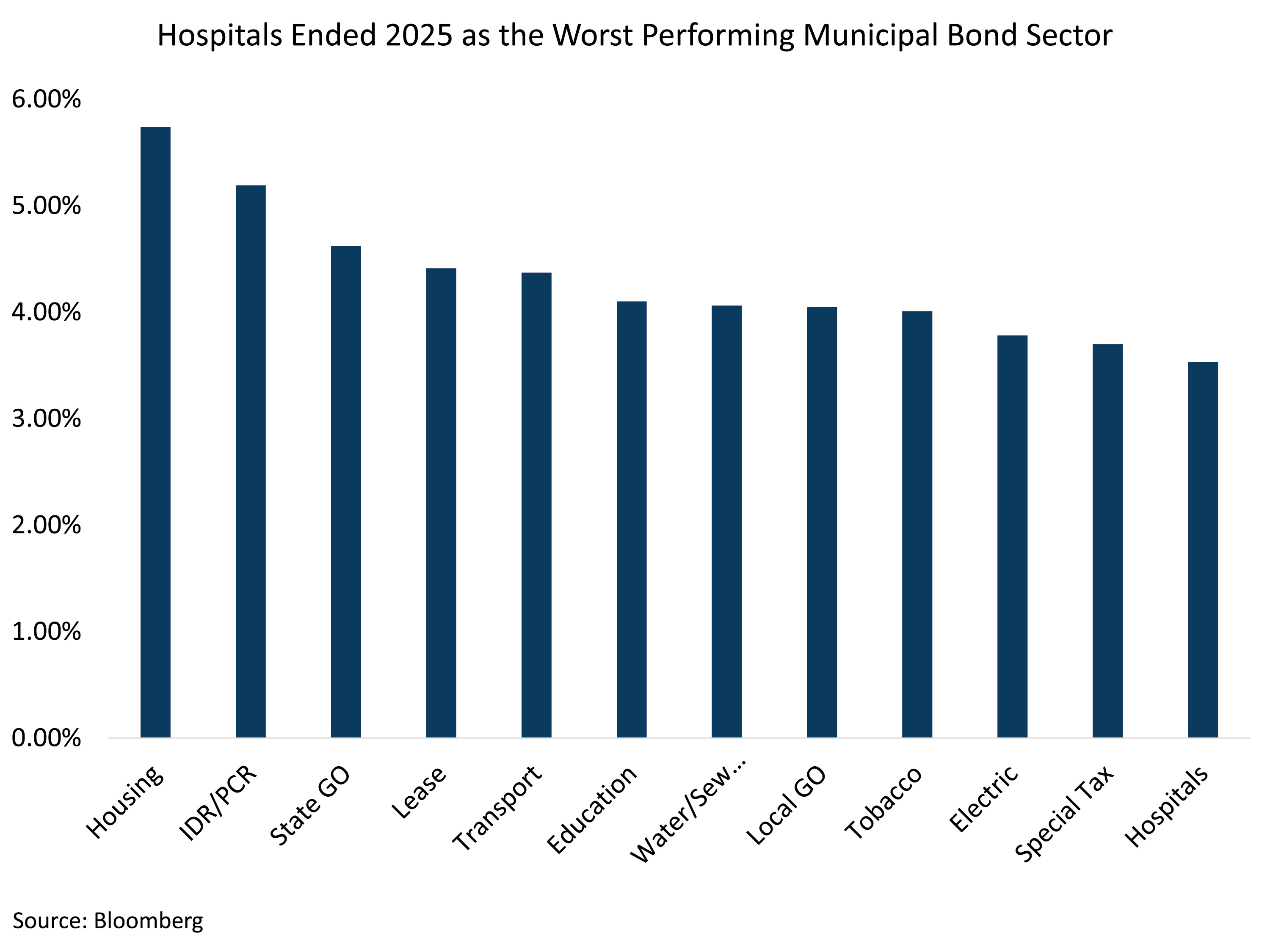

Investors have expressed significant concerns regarding the termination of the enhanced Affordable Care Act (ACA) subsidies, which officially expired at midnight on December 31, 2025. Fueling the unease was a report released last year by the Urban Institute, which projected that ACA enrollment would decline by 20% in 2026. On the heels of this, not-for-profit hospitals ended 2025 as the worst-performing sector in the municipal bond market, while numerous health insurers experienced heightened market volatility. However, recent data released by the Centers for Medicare & Medicaid Services suggests that these fears are overblown, with 2026 ACA enrollment currently declining by only 1.4 million — far less than early estimates suggested.

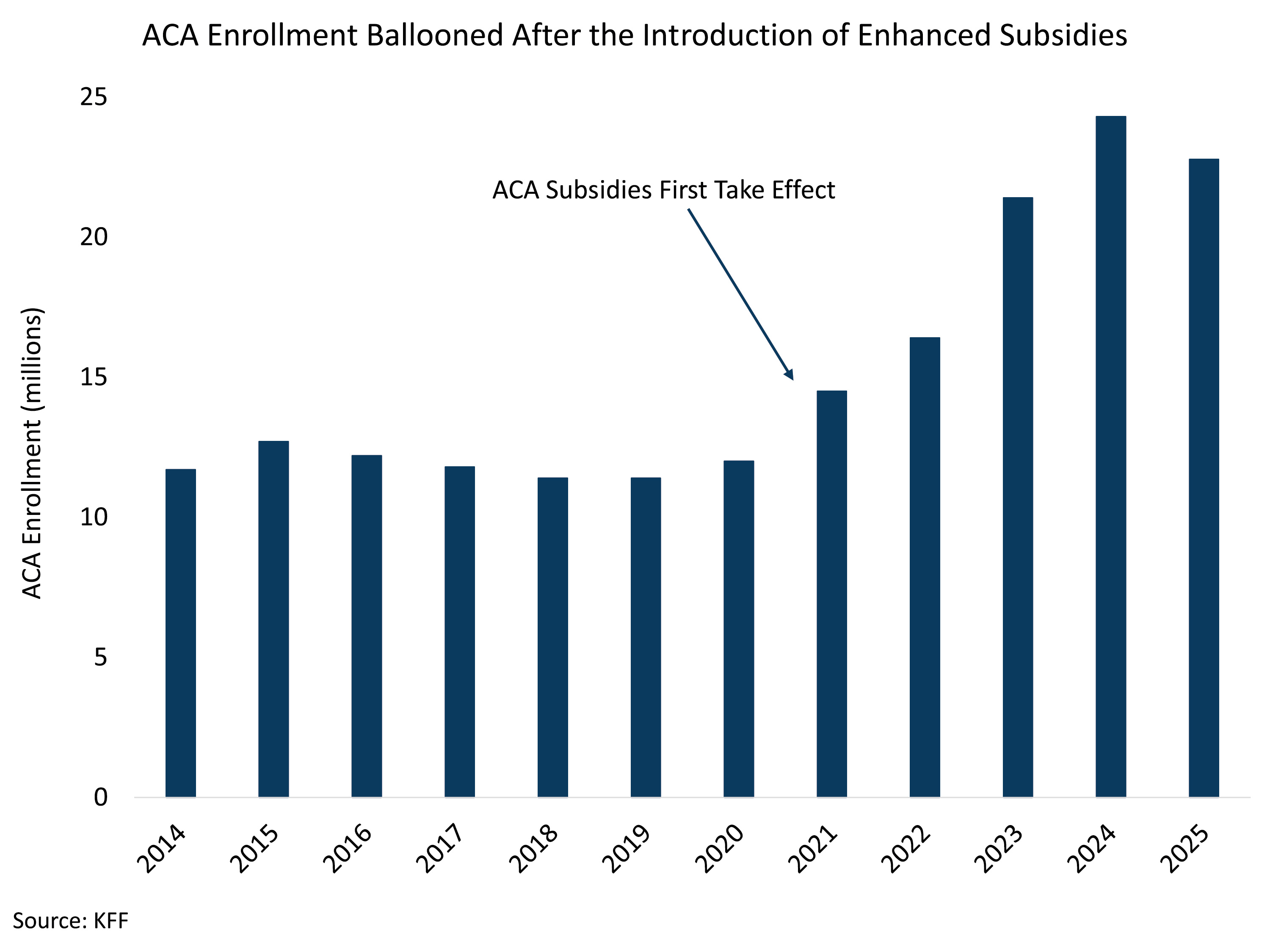

Post-Covid Subsidies Doubled ACA Enrollment

The ACA subsidies, which were first introduced under the American Rescue Plan Act (ARPA) in 2021 and later extended through 2025 via the Inflation Reduction Act, allowed individuals earning up to 150% of the federal poverty level to pay $0 in monthly health care premiums, while also reducing premiums for many higher‑income enrollees. As a result, ACA enrollment more than doubled between 2021 and 2025, reaching 24.3 million participants.

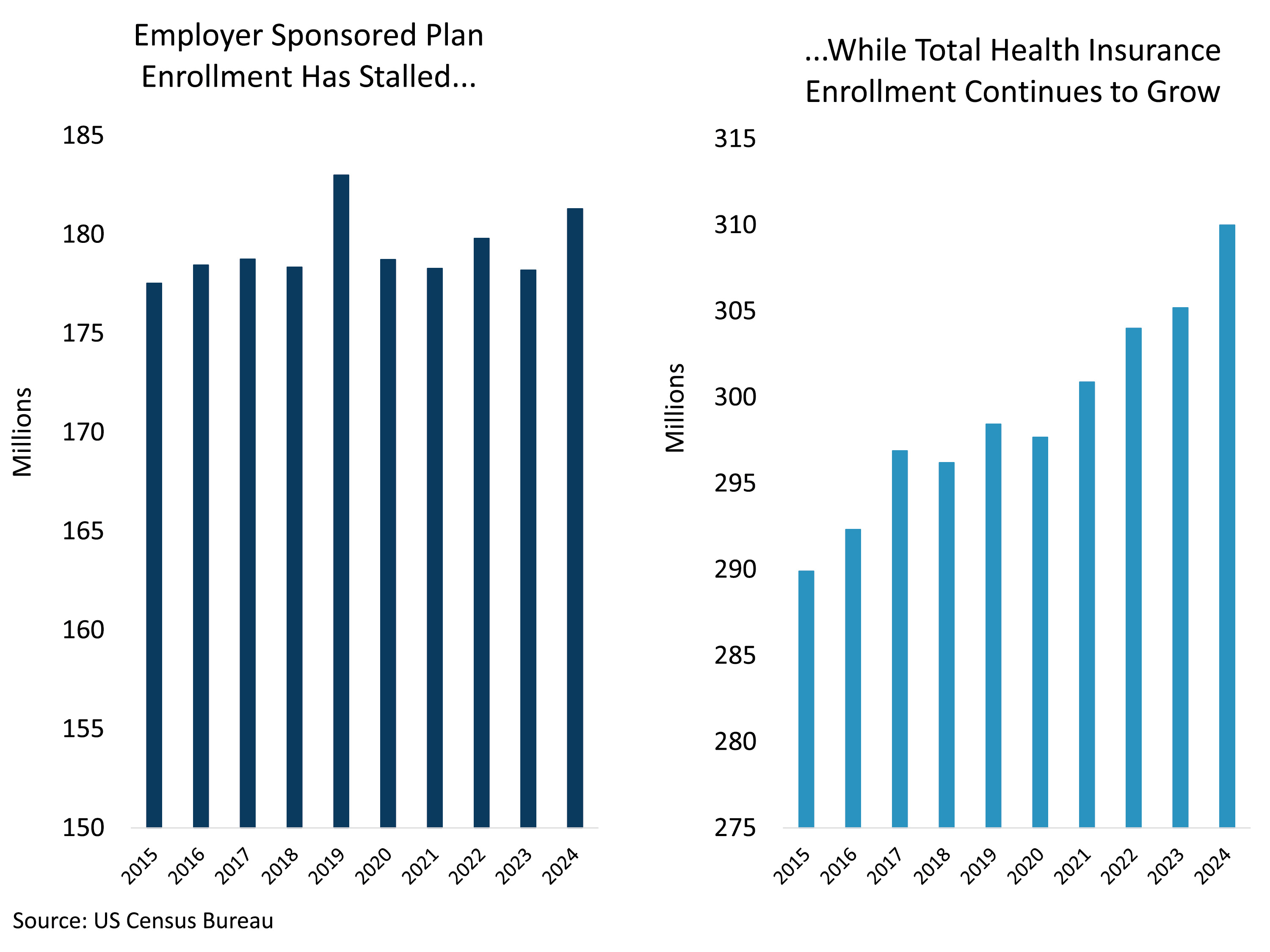

Individuals May Turn Back to Employer‑Sponsored Plans

While ACA enrollment has surged in recent years, employer‑sponsored participation still sits below its 2019 peak, even as overall insurance enrollment and employment have continued to grow. This pattern suggests that individuals pivoted from employer plans to the more affordable ACA Marketplace coverage made possible by the enhanced subsidies. With those subsidies now expired, employer‑sponsored insurance may once again be the more economical option for many. As a result, some of the reported decline in ACA enrollment may simply reflect individuals returning to employer coverage rather than becoming uninsured.

The Impact on Not-For-Profit and For-Profit Hospitals Has Been Relatively Muted

Despite the significant underperformance of municipal hospitals last year, we expect the loss of the enhanced ACA subsidies on both not‑for‑profit and for‑profit hospitals to be negligible for a couple of reasons. Even if all 1.4 million enrollees who left the Marketplace became uninsured, this would represent just a 0.45% decline in the insured population nationwide. Such a small shift is insufficient to materially affect hospital financial performance. Additionally, some health care systems could experience a benefit if patients move from ACA plans to employer‑sponsored insurance, which typically reimburses hospitals at higher rates.

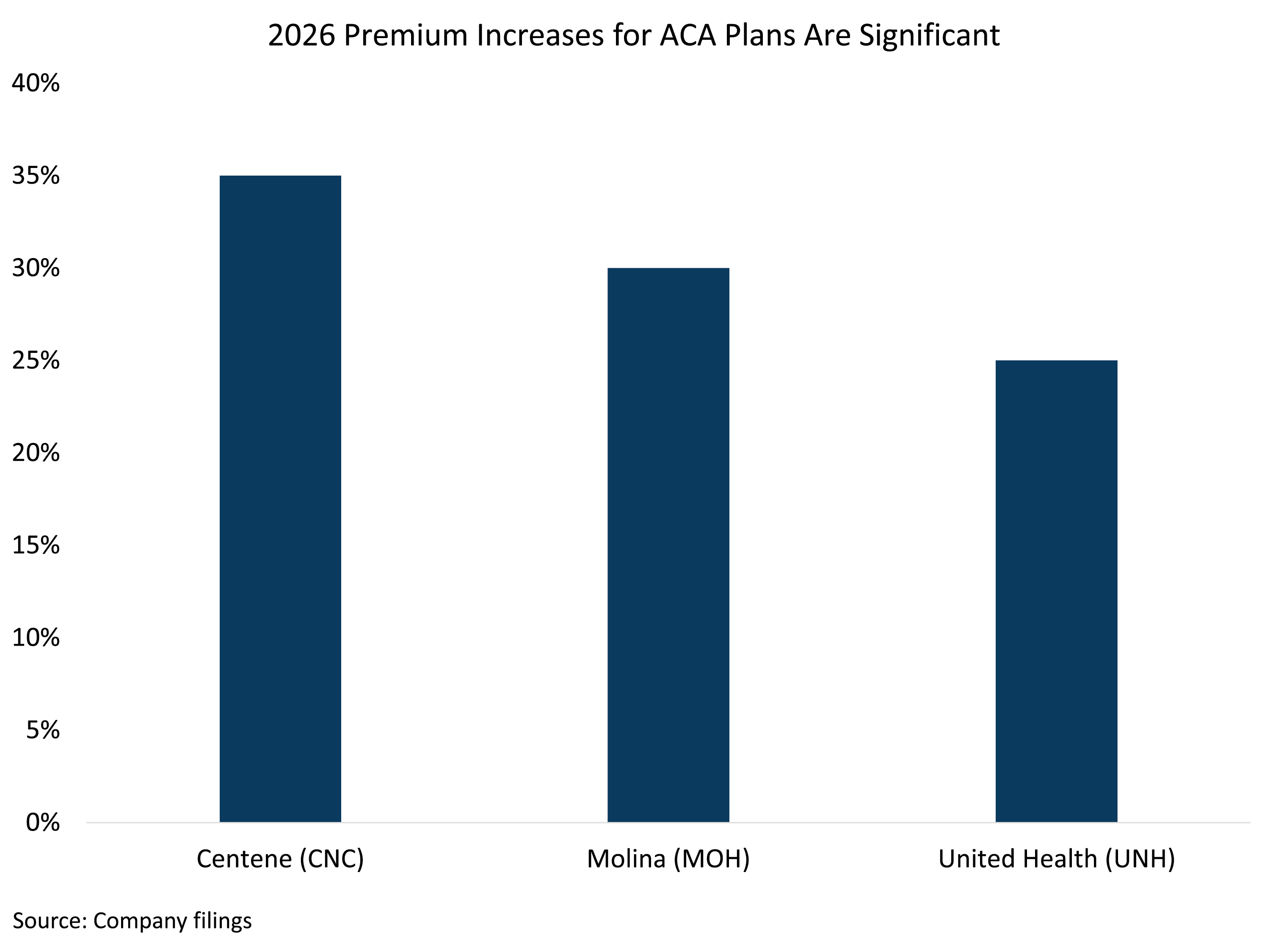

Premium Adjustments Will Help to Limit the Impact on Insurers

The expiration of enhanced ACA subsidies has been less disruptive to insurers than initially anticipated, with enrollment proving more resilient than expected, highlighting the relatively inelastic demand for Marketplace coverage. Following a difficult 2025 — when many managed care providers saw weaker ACA results because they were covering higher‑acuity members with higher medical costs — the industry is now repositioning for margin recovery through significant premium increases averaging 20%. These pricing actions reflect both the adverse cost trends of the prior year and expectations that the risk pool could deteriorate in the wake of subsidy expiration.

A more stable enrollment base should help improve underwriting performance by broadening and balancing the risk pool, thereby mitigating the relative impact of higher‑acuity members. With enrollment now stabilizing and the cumulative effect of 2025–2026 rate increases taking hold, managed care providers appear on track toward a more sustainable margin profile.

The Bottom Line

Despite heightened media focus on the lapse of the ACA enhanced subsidies, we see no evidence that the change will create material financial headwinds for insurers or health care providers.