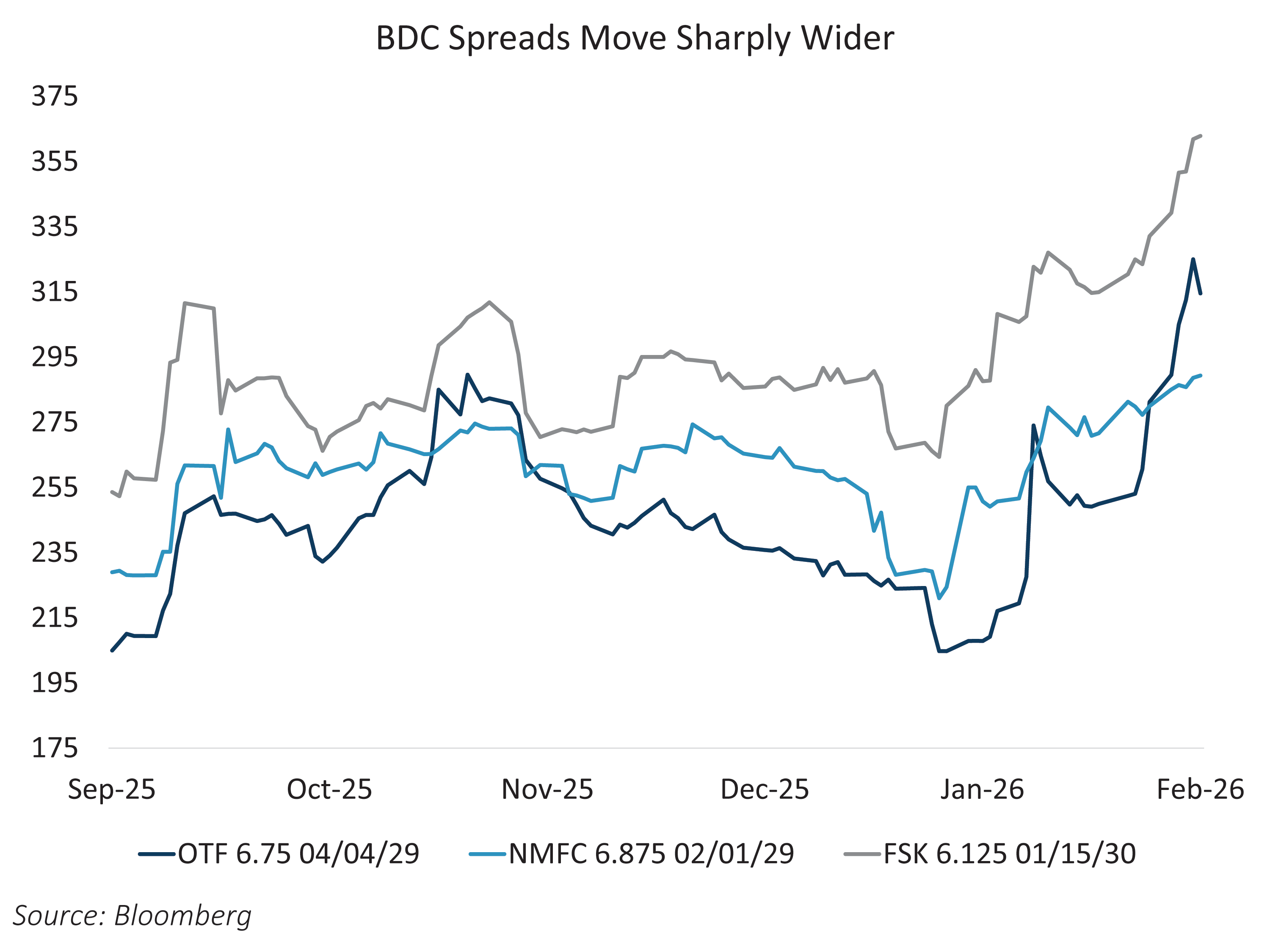

Headline risk in the BDC sector continues to build following the initial fallout from the software‑led selloff (see our previous Notes: From Bulletproof to Broken). As the public‑market cousins of private credit, BDCs share many of the same structural features, most notably assets that are not marked‑to‑market. This feature leaves investors exposed to jump‑to‑default risk as deteriorating credits often surface abruptly rather than gradually through pricing. The central question for bondholders is, when does elevated headline risk migrate into fundamental impairment? While the market continues to debate this inflection point, BDC bond spreads have steadily widened amid a growing list of idiosyncratic disclosures, underscoring investor sensitivity to delayed transparency in underlying credit quality.

First, Blue Owl (OTF) — long viewed as a flagship sponsor within private credit and a significant investor in technology — announced the sale of $1.4 billion of private credit assets at an average price of 99.7% of par. The transaction raised questions around ecosystem interconnectedness, as one of the buyers, Kuvare, maintains a relationship with Blue Owl, which acquired Kuvare’s asset management business in 2024 and currently acts as an investment advisor. Although ownership does not overlap and the transaction was conducted at arm’s length, the announcement only triggered a brief rally across Blue Owl managed BDCs before selling pressure resumed.

Additional Blue Owl related headlines emerged on February 20, when two alternative asset managers specializing in closed end funds offered liquidity to three private Blue Owl BDCs — OCIC, OBDC II, and OTIC — at discounts of 20–35% to par, to be determined at final tender. These vehicles have experienced elevated redemption requests in recent quarters, consistent with broader industry trends. While the provision of liquidity is constructive for the sector, the magnitude of the proposed discounts was perceived negatively. Private perpetual BDCs typically offer quarterly redemptions capped at less than 5% of NAV, transacted at NAV, underscoring investor sensitivity to discounted exits.

On February 25, New Mountain Finance (NMFC) sold $477 million of BDC assets to Coller Capital at approximately 94% of par, resulting in a markdown to the fund’s NAV. Management cited portfolio diversification as a driver, noting that roughly 33% of the assets sold were software related investments.

Also on February 25, FS KKR Capital (FSK) reported earnings that highlighted a 5% sequential decline in NAV driven by both realized and unrealized losses, alongside a dividend cut. The results triggered a roughly 15% decline in the company’s equity and a 25 basis point widening across its bonds. FSK reported an increase in non accruals, with several investments contributing to the deterioration, including Medallia, an enterprise SaaS company held across multiple BDC platforms. With negative outlooks from Moody’s and Fitch at the BBB level, FSK now sits on the cusp of a downgrade to high yield, potentially joining TCPC and PSEC, as fundamental dispersion within the sector continues to widen.

With asset marks deteriorating across quarterly earnings, and persistent headlines tied to technology exposure and rising redemption activity, we believe the credit profile of the BDC sector remains under pressure. Should net redemptions turn structurally negative, the sector could face more significant and lasting challenges.