While the equity market has its well‑known “January Effect,” credit markets also show a seasonal pattern. Looking back over nearly three decades of data, January tends to be one of the better months for corporate bond spreads. The question is whether this early‑year strength typically carries through to the rest of the calendar year, and what it might mean for 2026.

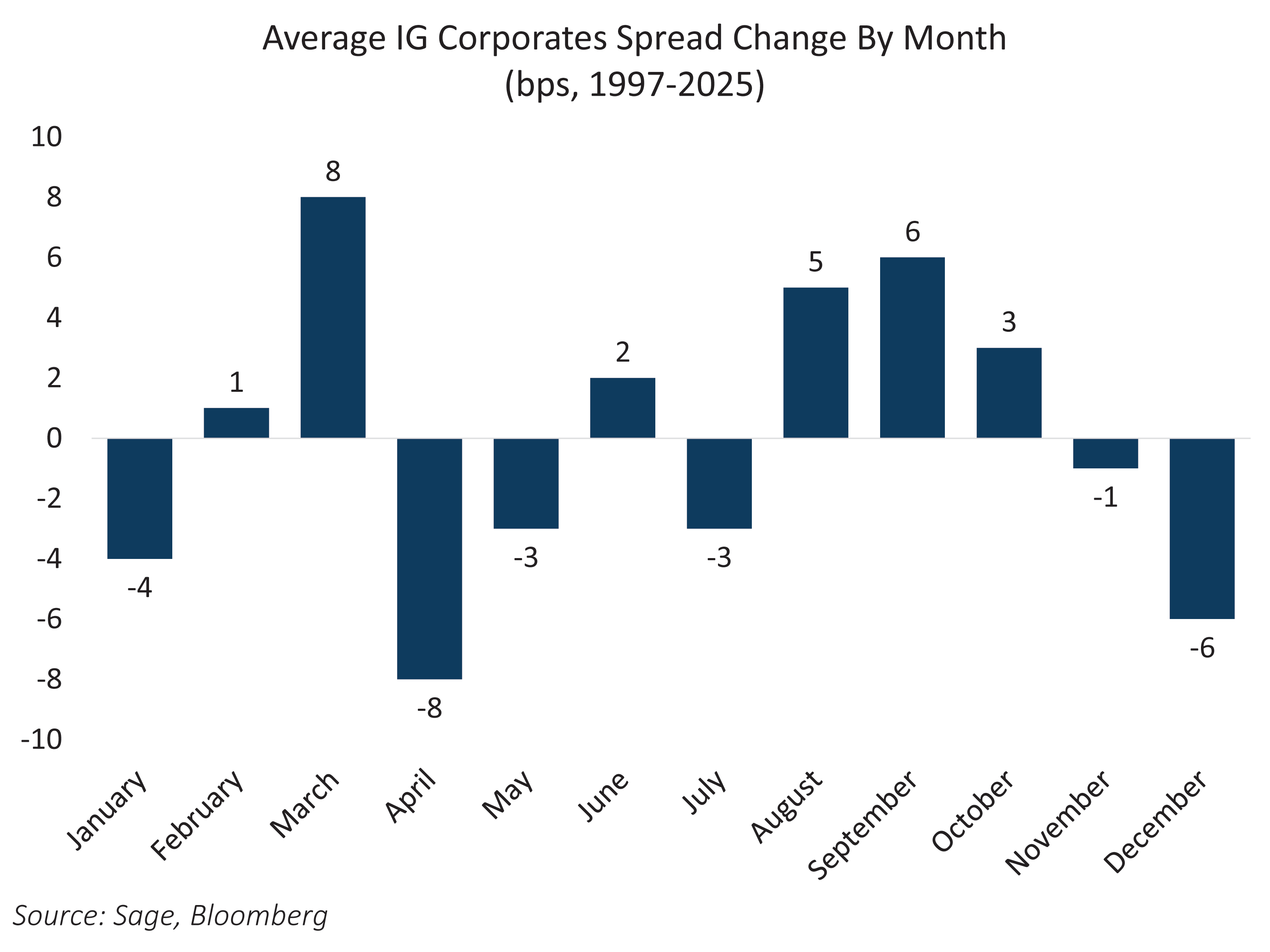

This trend is especially pronounced in investment‑grade corporates. Since 1997, January has seen spreads tighten by about 4 basis points on average, the third-best month of the year, behind April and December. This year has already exceeded the historical average: IG spreads have tightened by 6 basis points so far.

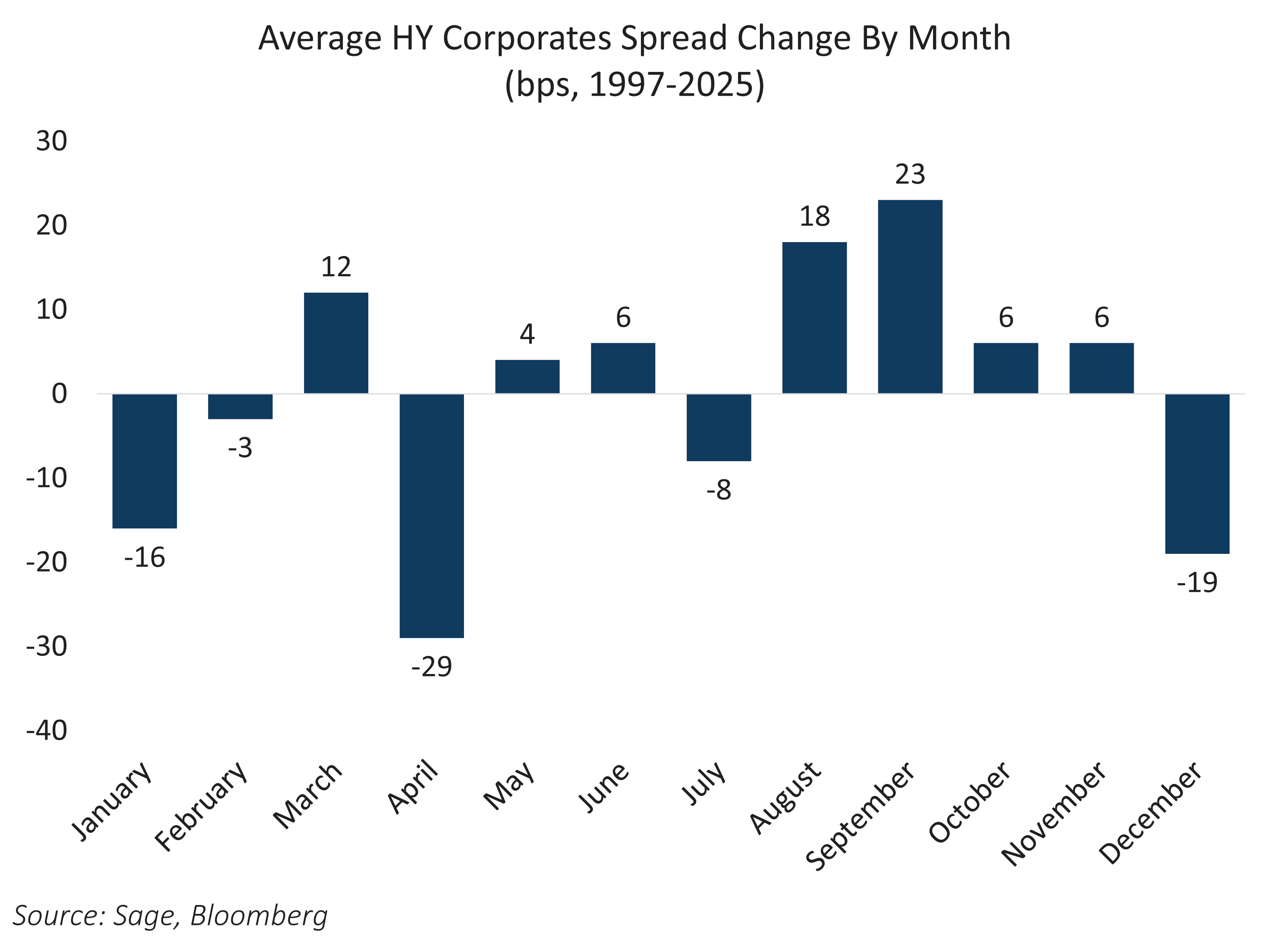

High yield exhibits a similar seasonal pattern. January has historically been the third‑best month for high-yield as well, averaging a 16‑basis‑point tightening. HY spreads have already tightened by 10 basis points in 2026.

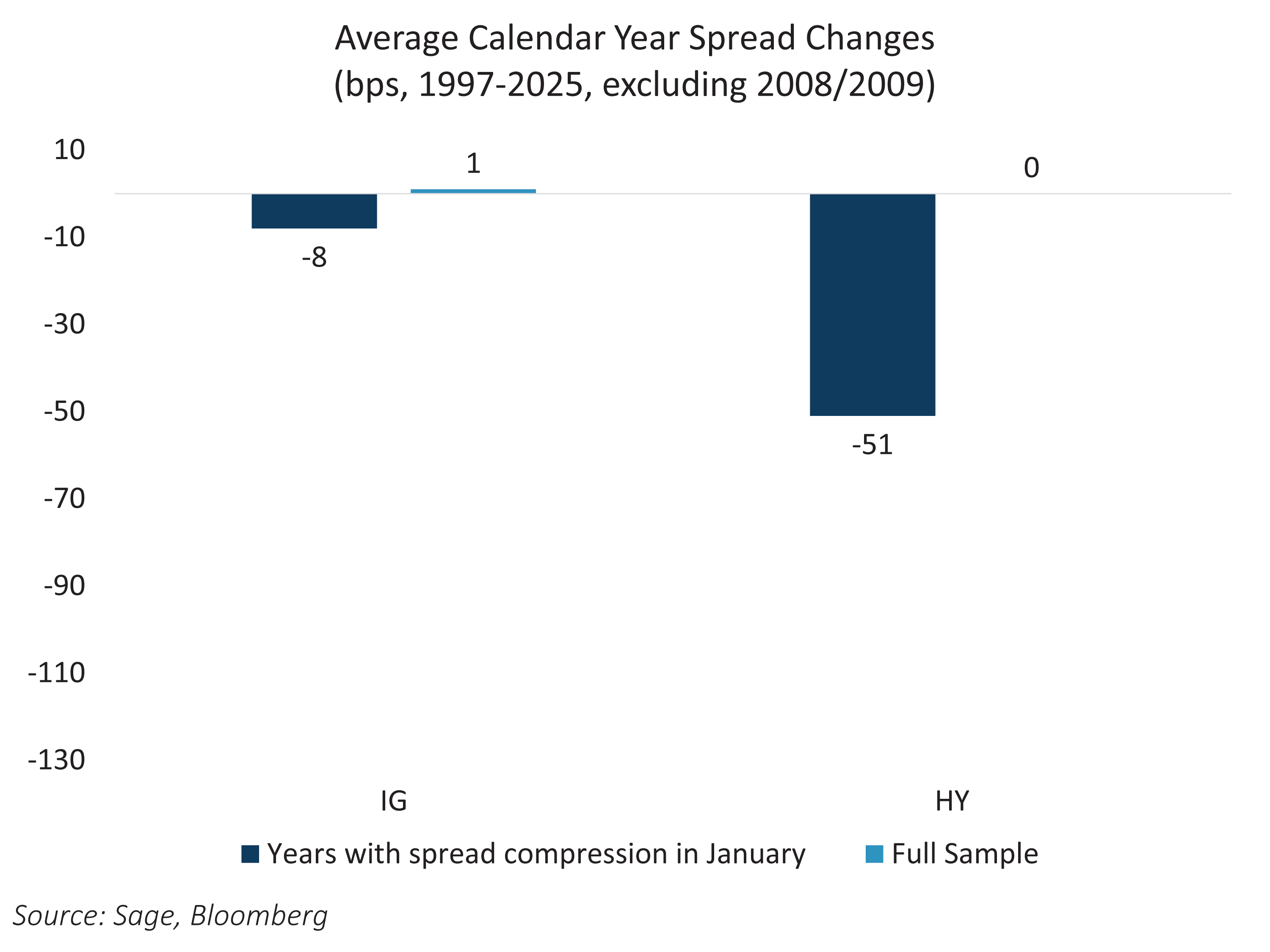

The more interesting question is whether a strong January tends to correspond with strong full‑year performance. Historically, it often does. In years when IG spreads tightened in January, the full‑year average is -8 basis points, compared with an +1 basis point average across all years since 1997 (excluding 2008-09). High yield shows the same tendency: in years when HY spreads tightened in January, the remainder of the year averaged a -51-basis-point move, versus roughly flat across all years. There appears to be a meaningful seasonal pattern — early-year strength has often aligned with tighter spreads over the balance of the year.

However, both investment grade and high yield spreads are already entering 2026 near historic lows — around 74 basis points for IG and 250 basis points for HY. So, while the seasonal signal points to continued tightening, current valuations suggest that even if spreads stay firm, the magnitude of further compression may be modest. With risk premiums already thin, strong economic fundamentals and policy support become the key forces that can keep spreads stable at today’s rich levels.