There has been no shortage of market‑moving events in 2026, and the pace of headlines alone has been enough to keep investors on edge. Geopolitical concerns remain elevated, the labor market is decelerating, trade policy uncertainty continues to hang over corporate decision‑making, and pockets of stress have emerged in areas of the credit markets. Yet despite this backdrop, there has been no discernible weakness in the private sector. Earnings growth remains positive, and both the consumer and the broader household sector continue to look remarkably resilient.

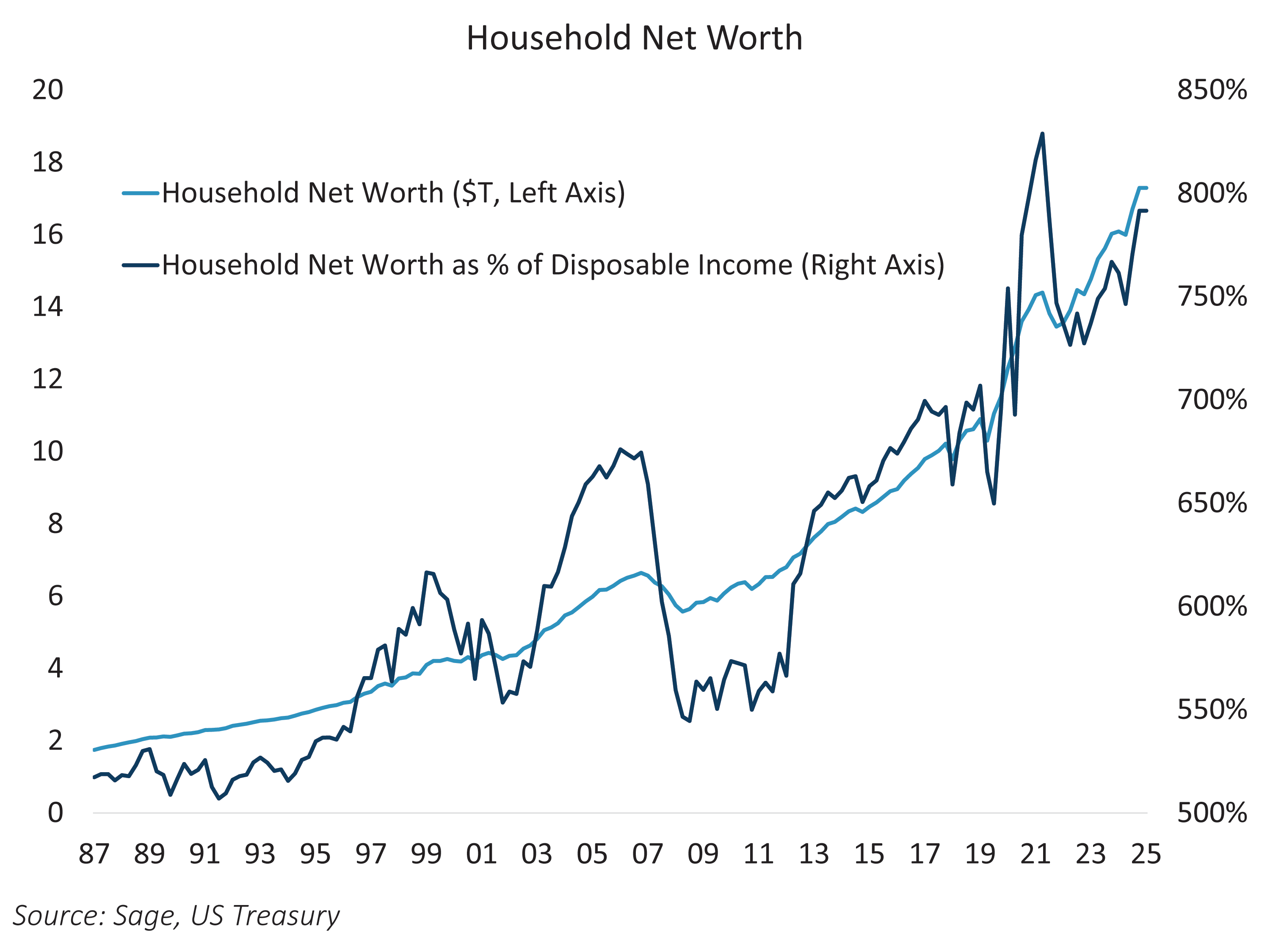

This resilience is most evident in the balance sheet of the household sector itself. Household net worth now stands at roughly $18 trillion, a level that equates to approximately 800% of disposable income. That ratio alone highlights how dramatically asset markets have grown in importance to the health and behavior of the private sector relative to prior cycles.

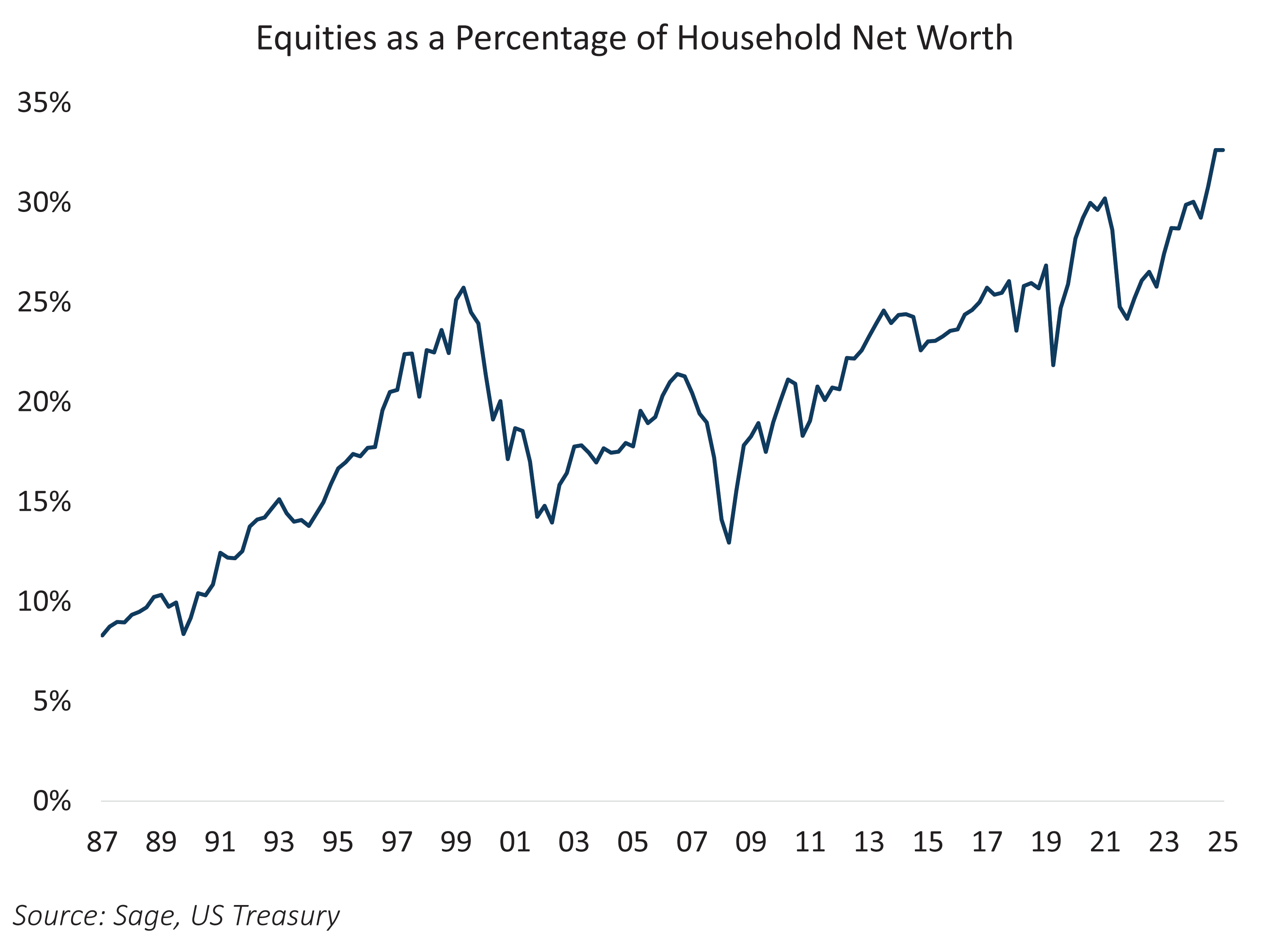

The composition of that wealth is notable. According to US Treasury Flow of Funds data, roughly 33% of household net worth is now held in corporate equities and mutual funds. That represents a dramatic shift from 40 years ago, when equity holdings accounted for less than 10% of household wealth. Over multiple decades, rising asset prices, financialization, and increased participation in capital markets have fundamentally altered the way households build and sustain wealth.

As a result, financial markets now play a more central role in shaping real economic outcomes. Equity market drawdowns increasingly have the potential to create negative feedback loops that spill into consumption, confidence, and ultimately real economic activity. A sharp or prolonged decline in asset prices could present a systemic risk, not because of traditional leverage or banking stress, but because of its impact on household behavior in an economy where wealth effects matter more than ever.

This shift helps explain why both the Federal Reserve and the Treasury are likely to show greater sensitivity to equity markets and overall financial conditions. When household balance sheets are tied so closely to asset prices, sharp tightening in financial conditions can translate into slower growth. Recent volatility in private credit and business development companies, combined with ongoing geopolitical risks such as the Iran conflict, could weigh on growth and inflation — particularly if household confidence or spending weakens — keeping risks to rates skewed to the downside.