In recent months, the cost of living has consistently polled as the top issue for American voters, with housing affordability standing out as one of the biggest pressure points. This issue is shaped by a collection of forces — mortgage rates, home prices, household incomes, and inventory — and has increasingly drawn policy attention in Washington as affordability becomes a priority for the midterm agenda. These conditions and policy stance should continue to support mortgage-backed securities (MBS) as a source of high quality spread over Treasuries in the coming months.

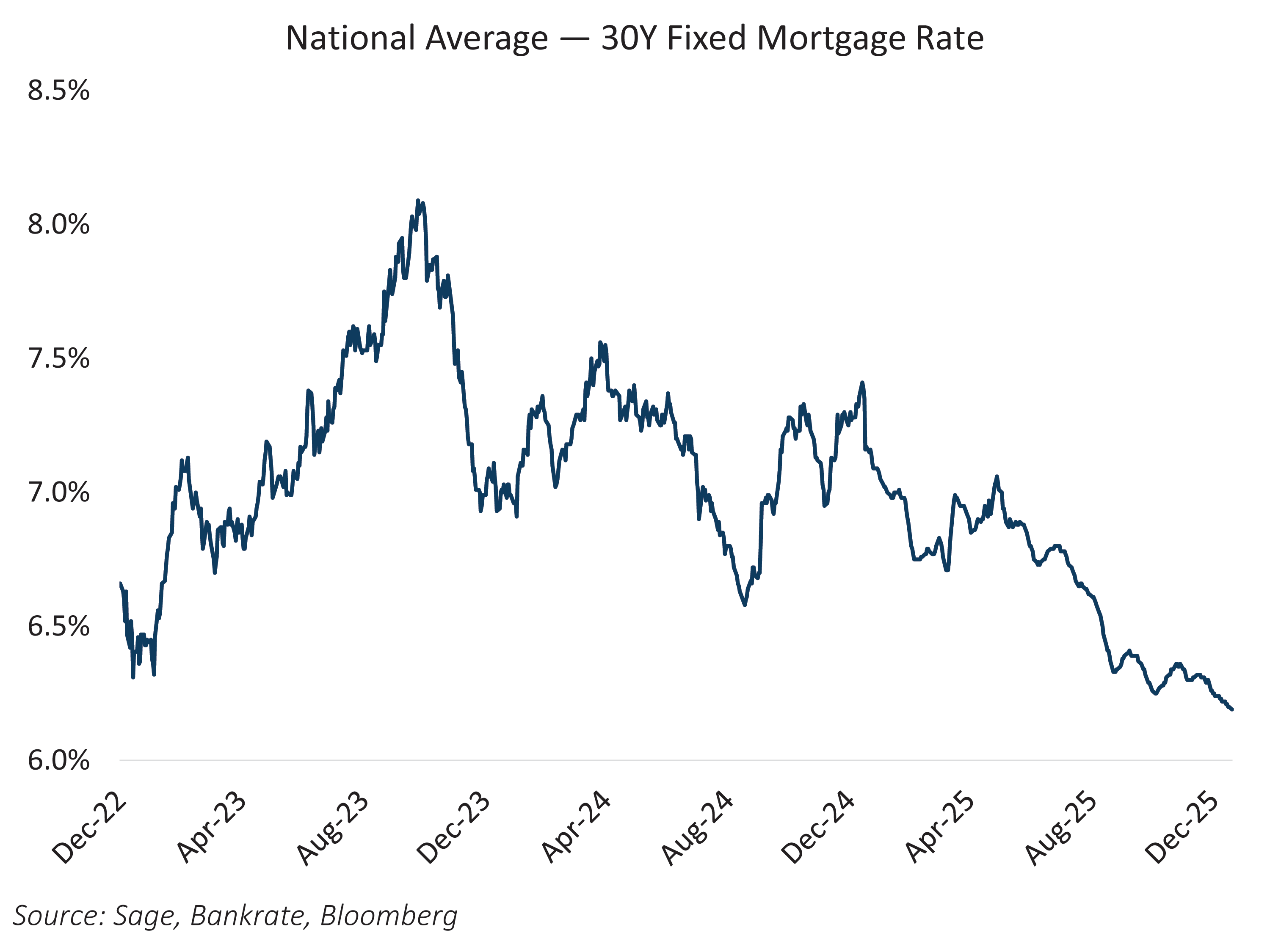

Home affordability has been strained for several years, with high borrowing costs driving many would‑be buyers out of the market. Over the past year, however, mortgage rates have begun to decline from their peak levels. The average 30‑year fixed mortgage rate recently declined to 6.19%, down from a peak near 8% just over two years ago, and could fall below 6% later this year — easing monthly payment burdens compared with peak‑rate periods. This easing in borrowing costs has provided some incremental relief for affordability.

Even with improving mortgage rates, inventory remains tight, and many sellers are reluctant to list their homes while they sit on deeply attractive pandemic‑era mortgage rates. Still, the supply picture is inching in the right direction. Falling mortgage rates have contributed to greater pricing flexibility, with price cuts rising nationally near the end of 2025. Meanwhile, broader measures of inventory tracked by the National Association of Realtors indicate that 2025 also saw a rise in listings. These shifts signal a market transitioning closer to equilibrium.

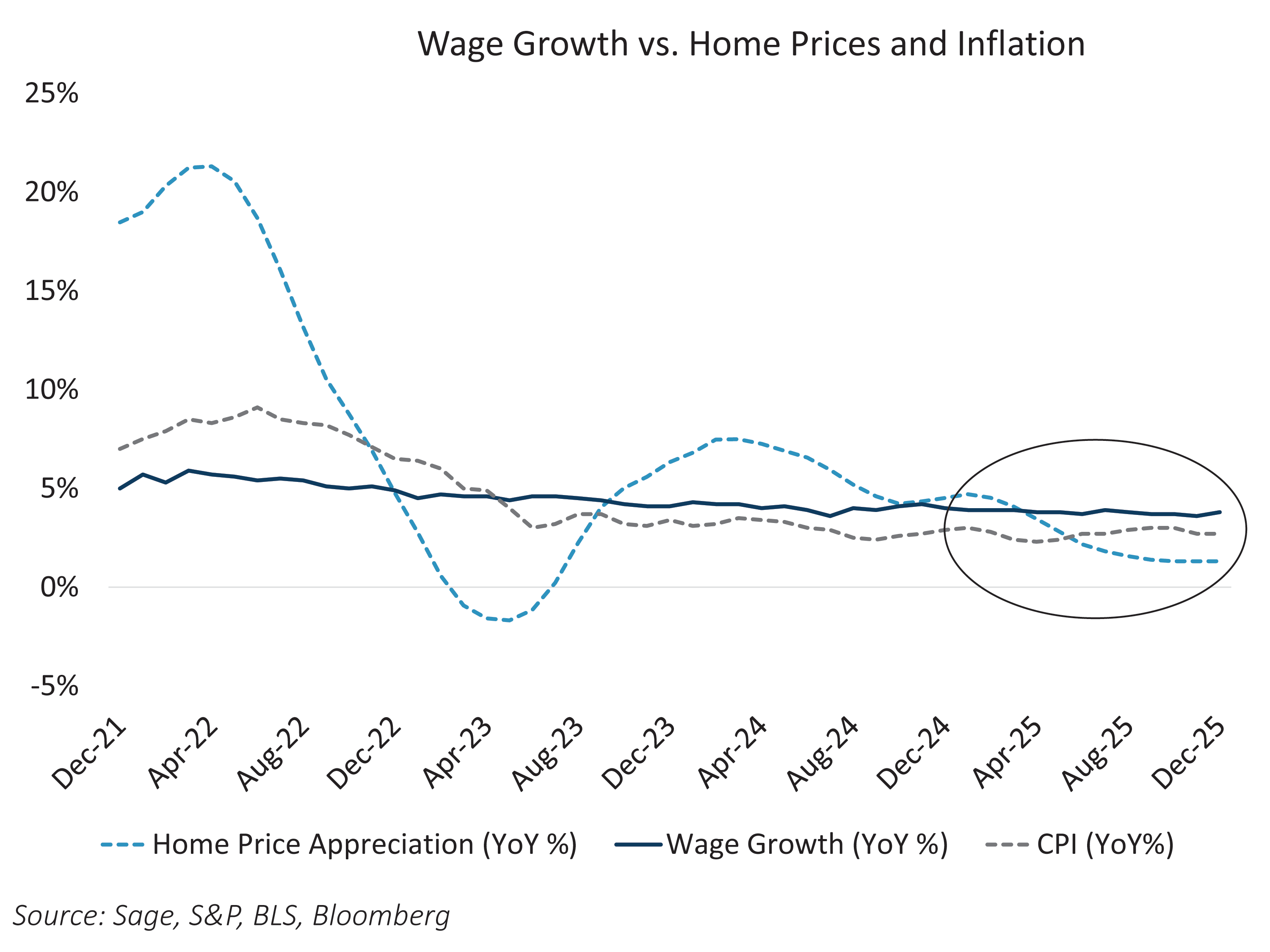

Household income dynamics add a layer of improvement to affordability. Wage growth is currently outpacing broad inflation and home‑price appreciation. Combined with stabilizing mortgage rates, this should pull monthly mortgage payments down and reduce the typical payment burden.

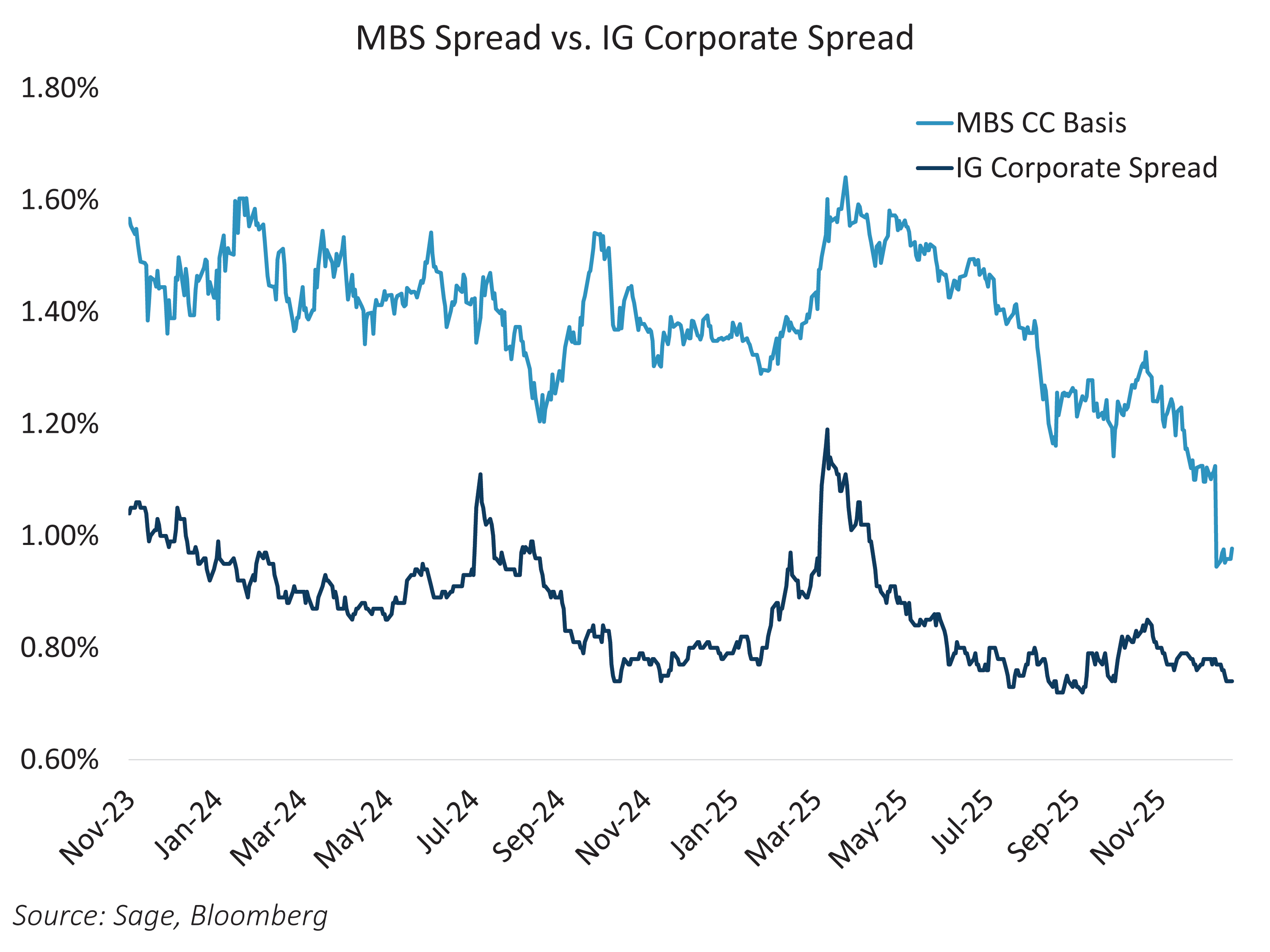

All of this is unfolding as policymakers ramp up their attention to housing affordability in advance of the midterms. Proposals circulating now range from restricting institutional ownership of single‑family homes to large‑scale mortgage‑backed securities purchases; the latter is already influencing MBS valuations. President Trump’s recent push for the government‑sponsored enterprises to buy $200 billion in MBS triggered a nearly immediate tightening in MBS spreads as markets priced in the impact, leaving MBS as one of the standout performers in fixed income over the past several months.

While MBS spreads have repriced much tighter so far this year, the sector will remain well supported and continue to provide high quality spread over Treasuries. If affordability remains a signature political priority, policymakers have a strong incentive to support mechanisms that directly influence mortgage rates. That dynamic, coupled with improving supply conditions and gradual income growth, creates a supportive backdrop for MBS.