A confluence of factors has translated into a notable resurgence in bank M&A activity. Transaction volumes rose meaningfully in the second half of 2025 and multiple deals were already announced early in 2026. Given the continued fragmentation of the US banking system — now numbering more than 4,000 institutions — and a regulatory regime that has materially shortened approval timelines, consolidation activity appears well positioned to persist over the coming years.

As banks close out the fourth quarter earnings season and outline initial expectations for 2026, the operating backdrop remains firmly constructive across the industry. Institutions both large and small continue to benefit from a favorable combination of fundamentals, including sustained net interest income growth driven by loan growth and a steeper yield curve. At the same time, fee income has gained traction on the back of strong capital markets conditions and improved investment banking activity. Asset quality trends have remained relatively stable, and the regulatory environment has shifted in a more constructive direction.

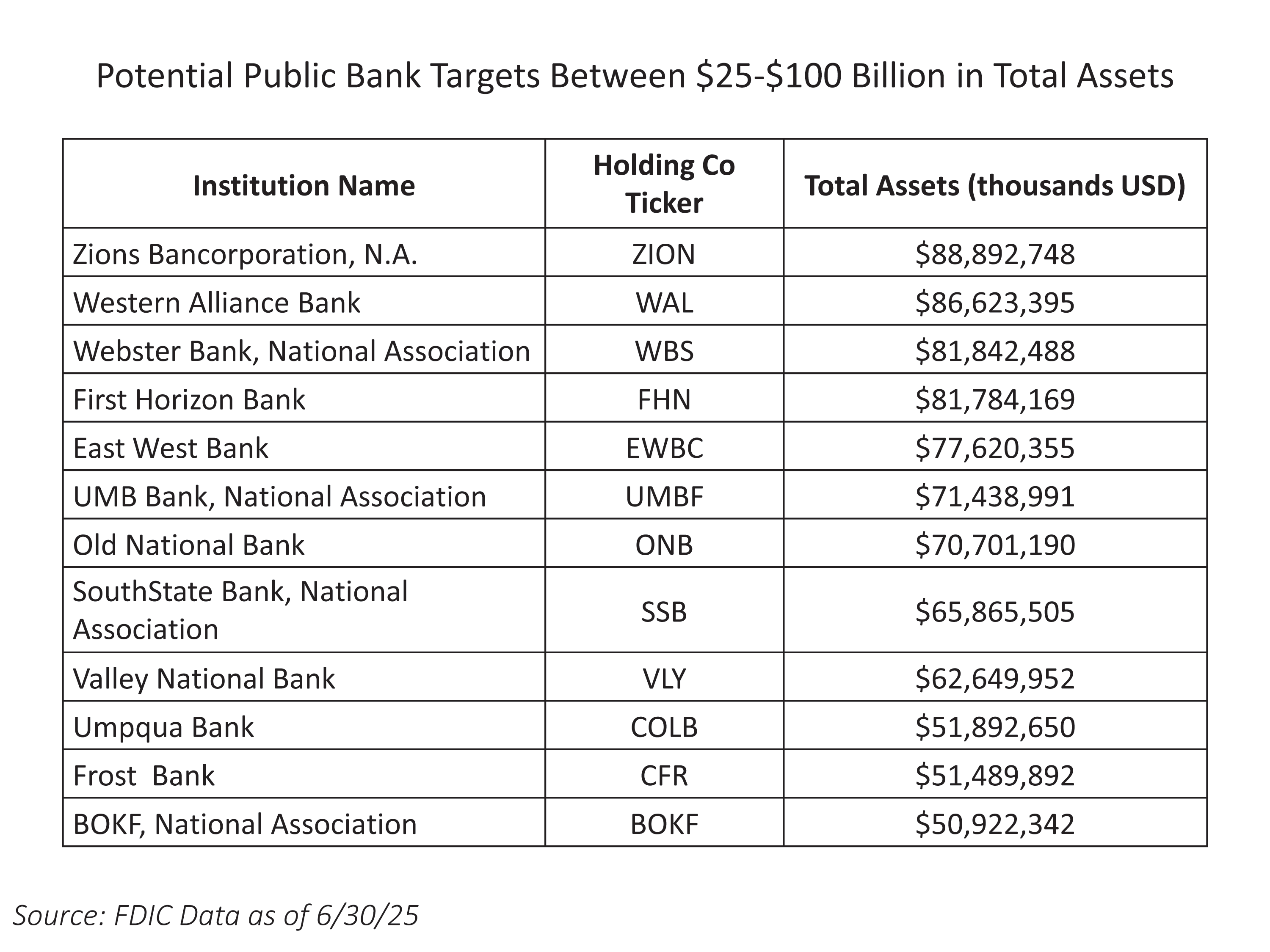

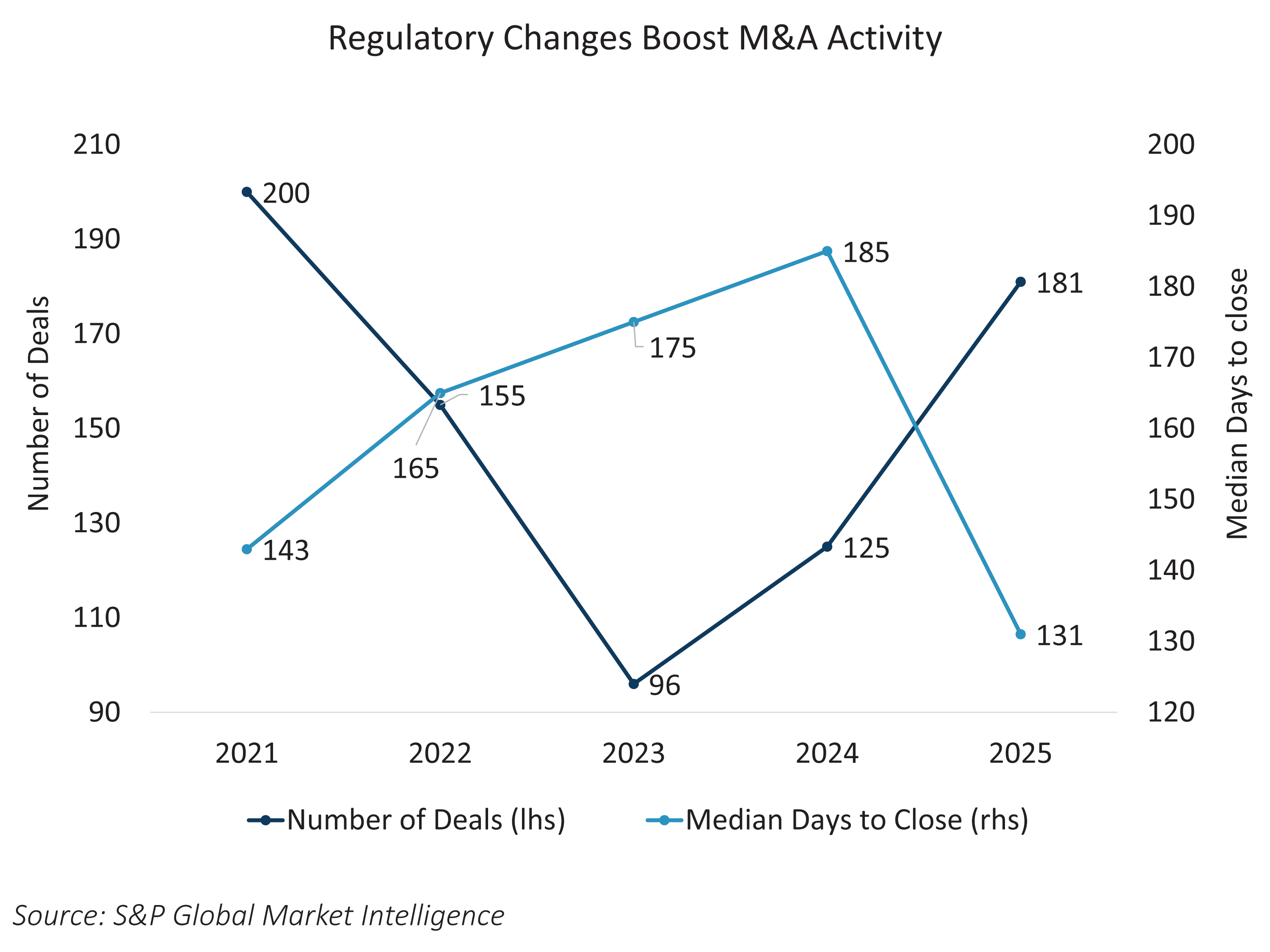

After several quieter years shaped by regulatory uncertainty and lingering caution following the 2023 regional banking stress, 2025 marked a clear inflection point for industry consolidation. Bank M&A deal counts increased to 181 (Source: S&P), the highest level since 2021. The sheer number of remaining institutions leaves ample opportunity, particularly among community and regional banks, but increasingly extending to larger national franchises, such as U.S. Bancorp and PNC.

Recent deal activity highlights the breadth of strategic objectives driving current transactions. Two recent tuck-in acquisitions were announced in early 2026: U.S. Bancorp purchased BTIG to enhance its equity capital markets capabilities, and Capital One acquired Brex to expand its footprint in corporate credit cards. These announcements coincide with peers, such as PNC, Huntington Bancshares, and Fifth Third Bancorp, actively closing and integrating previously announced acquisitions, underscoring a renewed confidence in executing strategic combinations.

A key catalyst supporting this momentum has been the sharp improvement in regulatory approval timelines. Recent transactions involving PNC, Huntington, and Fifth Third received regulatory clearance in fewer than 100 days, contributing to a steep decline in the industry’s median time to close. In 2025, the median close period fell to 131 days from 185 days in 2024 (Source: S&P). Greater speed and certainty of execution, combined with higher bank equity valuations, have become central drivers of the current consolidation wave.

From a credit perspective, bank M&A is typically less disruptive than corporate M&A, as transactions are predominantly equity financed rather than dependent on incremental leverage. That said, acquirers must still navigate execution and integration risks, including the potential absorption of loan portfolios that may not perfectly align with existing underwriting standards or credit culture. These risks are often mitigated by the benefits of increased scale, including cost synergies, improved operating efficiency, and a strengthened funding profile as banks deepen deposit penetration in existing markets or expand into new geographies with access to lower cost funding.

While the largest banking institutions may continue to face heightened scrutiny for transformational mergers, institutions with total assets below $700 billion appear particularly well positioned to pursue scale enhancing acquisitions in the current environment. Regional bank credit spreads have already compressed significantly toward those of money center banks, though further tightening opportunities remain — especially for institutions viewed as credible acquisition candidates. Taken together, the combination of supportive fundamentals, streamlined regulatory oversight, and strategic imperative suggests that bank M&A will remain a prominent theme in the industry over the next several years.