The past week has been marked by a sudden and unexpected escalation in the Iran conflict, adding a new layer of uncertainty to an already complex macro backdrop. Geopolitical shocks of this nature can reverberate quickly through markets. In the near term, the conflict clouds the outlook for both the real economy and interest rates, just as markets had grown more comfortable with a narrower range of outcomes and a consensus view centered on continued economic expansion.

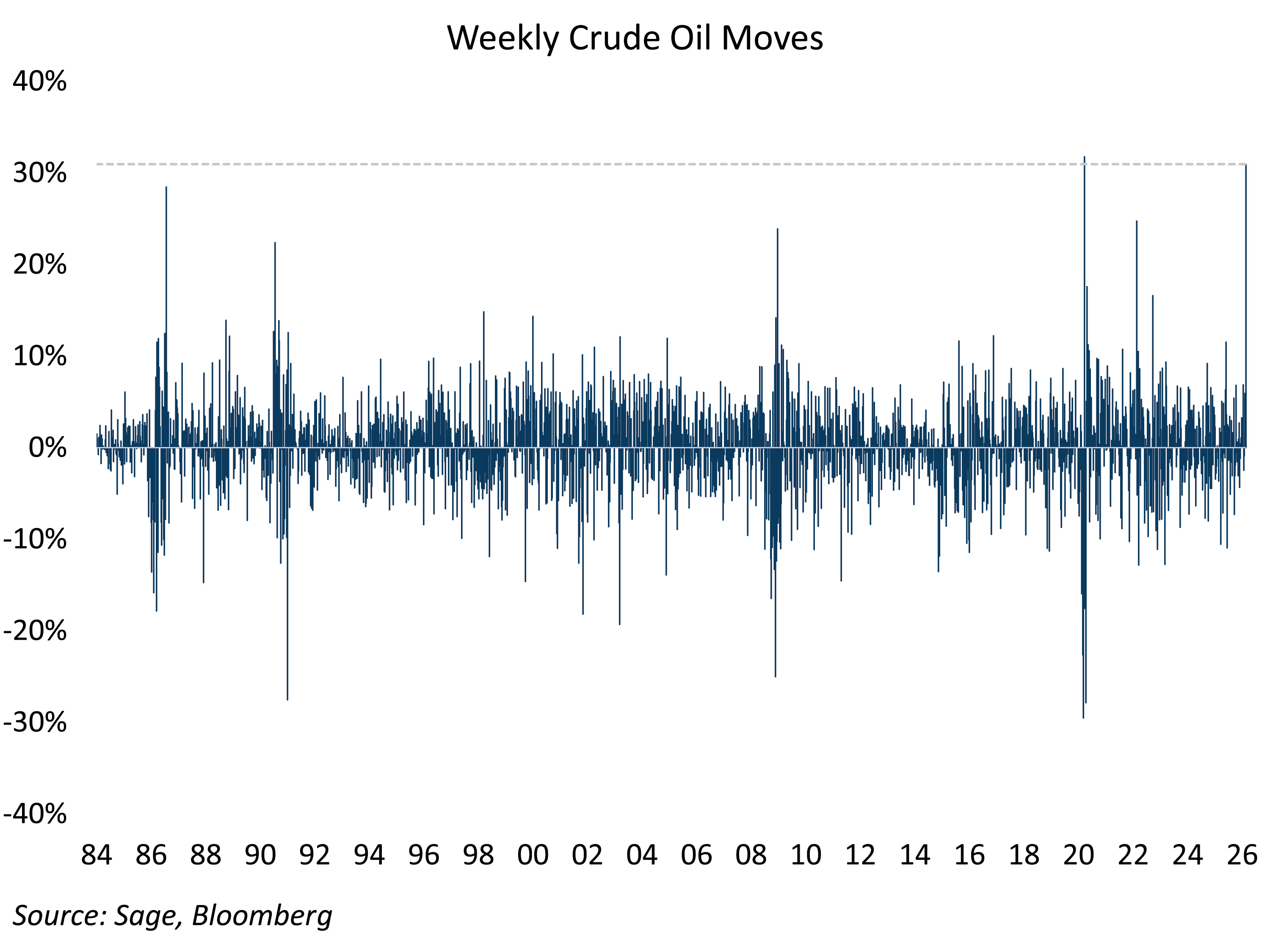

The following chart highlights just how extreme last week’s move in crude oil was historically. Going back to 1984, weekly changes in WTI have clustered within a modest range, with only a handful of episodes registering as true tail events. Last week’s 31% rise in spot crude oil stands out as the largest weekly increase outside of April 2020, which equates to a 6.5 standard deviation weekly move over that time period.

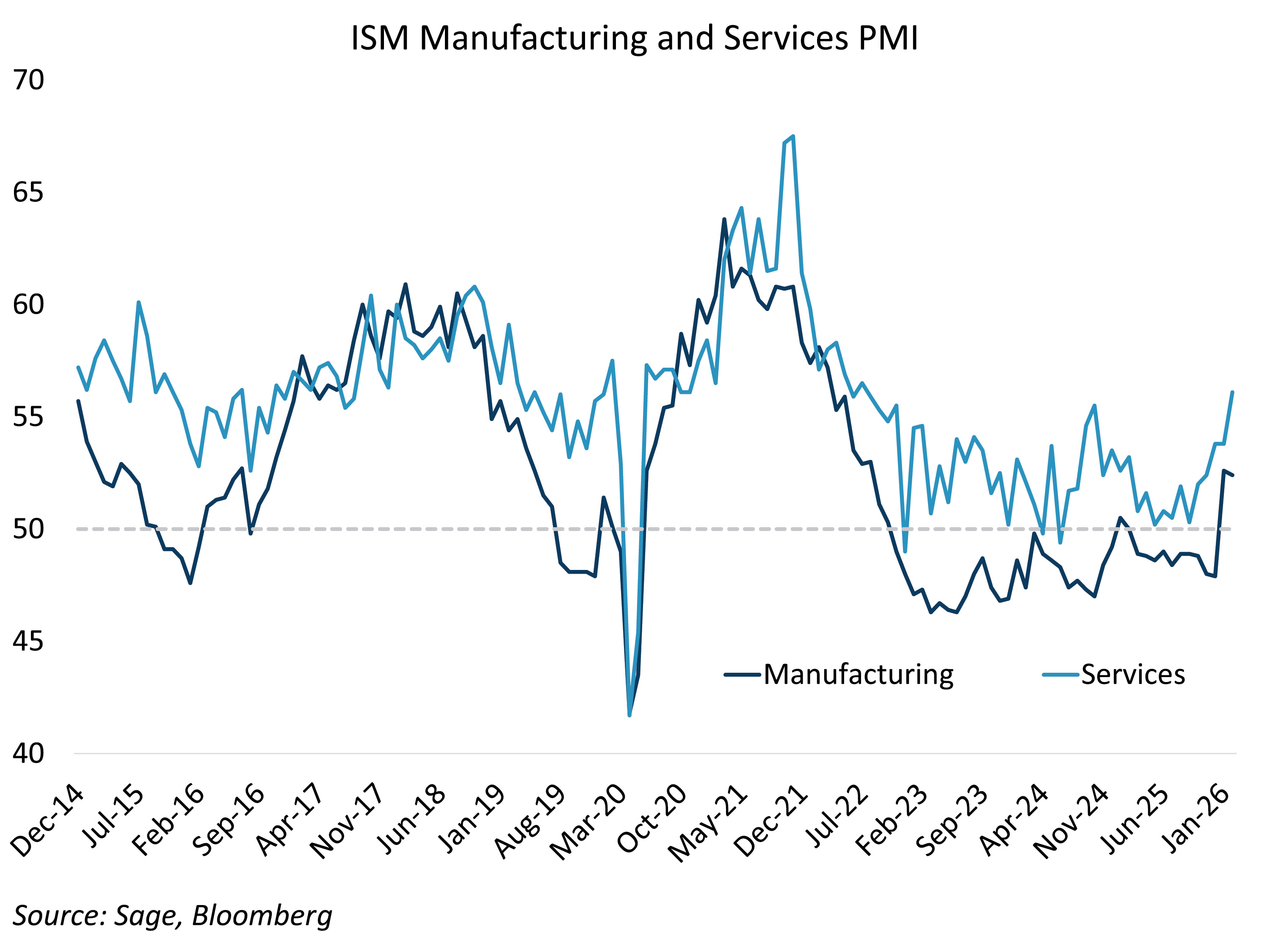

The sharp move in oil meaningfully complicates an economic picture that had been showing encouraging signs. Last week’s payroll report reinforced the theme of a jobless expansion, with labor demand cooling without a corresponding deterioration in broader activity. At the same time, ISM data continued to point toward a nascent pickup in manufacturing, suggesting that growth was stabilizing rather than rolling over. Into that backdrop, the oil shock arrives as an exogenous tightening force, raising the risk that higher energy costs bleed into consumption, margins, and inflation expectations just as momentum was beginning to firm.

The key variable now is time. A brief spike in oil prices would likely be absorbed with limited macro fallout, but a prolonged period of elevated energy prices would pose a more material threat to the improving growth outlook. Thus far, markets have been relatively restrained in their response. Treasury yields remain confined to a historically tight range, and credit spreads continue to trade near cycle tights, signaling little immediate concern about downstream economic stress. That calm, however, stands in contrast to the scale of the oil move itself, underscoring how quickly the balance of risks could shift should geopolitical tensions persist and energy prices remain elevated.