Executive Summary

Catastrophe Bonds (Cat Bonds) and Insurance Linked Securities (ILS) have delivered equity-like returns with bond-like volatility and low correlation to traditional markets, yet this attractive market sector remains largely underrepresented across institutional and private portfolios. Recent market data show a sector with expanding issuance, deepening liquidity, and improving transparency. Based on our research, Sage believes an allocation within diversified portfolios to the Cat/ILS sector can enhance risk-adjusted returns, reduce drawdowns, and shift the efficient frontier in investors’ favor. This research analysis consolidates the performance evidence, risk characteristics, and practical implementation pathways in support of why a thoughtful Cat/ILS allocation makes compelling sense for 2026 diversification and return optimization efforts.

Market Overview & Growth Momentum

- Record Issuance & Market Size: In 2025, Cat/ILS issuance reached $25.6B, with outstanding market size climbing to $61.3B — a 24% YoY increase and more than double 2016 levels. New sponsors and repeat issuers broadened participation, deepening liquidity and confidence.

- Product Evolution: Coverage now spans US/international property catastrophe perils as well as wildfire, windstorm, earthquake, cyber, and mortgage risks, offered via indemnity, industry loss, and parametric structures.

Why Cat Bonds & ILS Are Overlooked

Allocations typically remain below 5% due to familiarity bias, historical capacity constraints, limited insurance risk expertise within investment committees, policy/regulatory barriers, and reporting/benchmarking challenges (e.g., reconciling net vs. gross series). Despite these headwinds, empirical performance and diversification merits argue for increased adoption.

Comparative Performance & Risk Characteristics (as of Q3 2025)

| Asset Class / Index | 1-Yr | 3-Yrs | 5-Yrs | 10-Yrs | Volatility (Annualized) | Sharpe | Sortino | Basis |

|---|---|---|---|---|---|---|---|---|

| Private Credit (CDLI) | 9.65% | 11.32% | 10.06% | 9.55% | ~3-5% | ~0.6 | ~0.5 | Gross‑of‑fees |

| Cat Bonds (Swiss Re) | 14.10% | 12.20% | 8.80% | 7.15% | ~2.5-4.0% | ~1.3 | ~0.8 | Gross‑of‑fees |

| ILS Funds (Eureka) – net | 10.50% | 8.95% | 6.10% | 4.40% | ~3.5% | ~0.9 | ~0.7 | Net‑of‑fees |

| ILS Funds (Eureka) – gross | 11.75% | 10.20% | 7.35% | 5.65% | ~3.5% | ~1.0 | ~0.8 | +1.25% p.a. add‑back |

| Bloomberg US Aggregate Bond Index | 7.29% | 4.70% | -0.33% | 2.04% | ~3.0% | ~0.3 | ~0.2 | Gross‑of‑fees |

Notes: The “Eureka gross” series is constructed by adding a uniform +1.25% per annum to the net annualized returns of the Eurekahedge/With Intelligence ILS Advisers Index to approximate a gross‑of‑fees series and enable like‑for‑like comparisons with CDLI and Swiss Re indices. Actual net‑of‑fees returns to Q3 2025: 1Y 10.50%; 3Y (ann.) 8.95%; 5Y (ann.) 6.10%; 10Y (ann.) 4.40%. Sources: Bloomberg, Man Group Cat Bonds Primer; Eurekahedge methodology; Cliffwater CDLI; Swiss Re Global Cat Bond Index; Artemis Q4 2025 report. The Sharpe and Sortino ratios were calculated using annualized returns over a 10-year horizon as of 9/30/2025.

Modern Portfolio Theory (MPT) Justification

MPT favors assets with low/negative correlation to traditional holdings, as they can increase expected returns for a given risk or reduce risk for a given return. Because Cat/ILS returns are driven by insurance event risk rather than economic cycles or credit spreads, their correlation to equities and core bonds is near zero, enabling a meaningful shift of the efficient frontier for diversified portfolios.

Strategic Portfolio Benefits

1) Diversification & Uncorrelated Returns: Cat/ILS sector exposure is largely independent of macroeconomic drivers that impact the private credit and traditional fixed income sectors.

2) Resilience in Stress: Historical experience shows Cat/ILS returns have been flat‑to‑up during systemic sell‑offs (e.g., GFC, COVID), while private credit and equities fell; catastrophe‑heavy years saw modest sector drawdowns which were followed by significant recoveries.

3) Attractive Risk‑Adjusted Returns: historically low return volatility (≈3%) with Sharpe ratios up to ~1.3 and higher Sortino ratios compares favorably to most other credit market sectors.

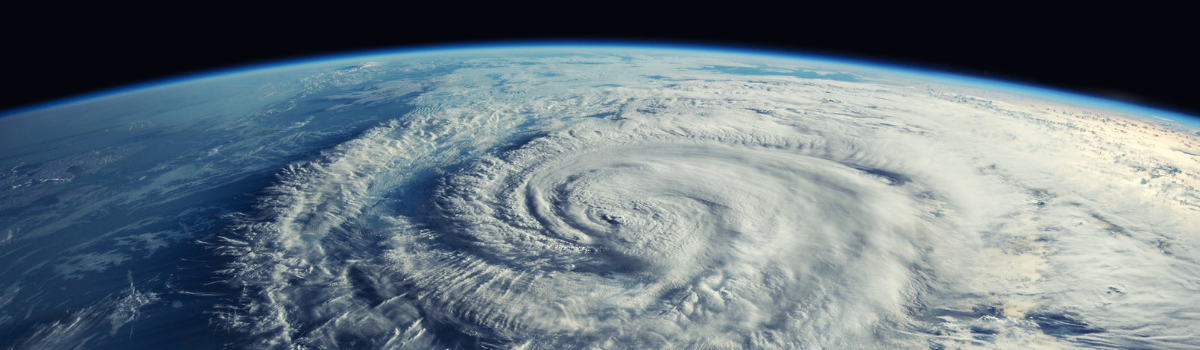

4) Sustainability Alignment: Cat/ILS capital supports climate resilience and disaster recovery, aligning with investors’ sustainability mandates.

Key Risks & Mitigation Strategies

| Risk | Mitigation |

|---|---|

| Event Risk: Exposure to severe insurance events (hurricanes, earthquakes, wildfires, cyber). | Diversify by peril, geography, sponsor; favor managers with robust catastrophe modeling and disciplined risk selection. |

| Liquidity Risk: 144A Cat Bonds provide quarterly liquidity and active secondary markets; certain private ILS vehicles may have lock‑ups/gates. | Align allocations with investment horizon; consider interval/listed vehicles for periodic liquidity. |

| Basis Risk: Trigger structure (indemnity, parametric, industry loss) can influence payout vs. actual losses. | Match triggers to objectives; diversify trigger types. |

| Manager Selection Risk: Dispersion exists across underwriting/modeling skill and portfolio construction. | Rigorous due diligence on performance transparency, process, and governance. |

| Policy/Regulatory Risk: Some IPS/regulatory frameworks still constrain ILS allocations. | Update policies, document gross vs. net basis, fee assumptions, and risk controls. |

Implementation Guidance

Access Vehicles

- 144A Cat Bonds: Standardized, tradable securities for qualified institutional buyers; transparent, liquid, and broad peril coverage.

- Private ILS Mandates: Tailored exposure (collateralized reinsurance, retrocession, sidecars) to specific perils/regions/risk layers.

- Interval/Listed Vehicles: Diversified portfolios with periodic liquidity and simplified access for certain investor types.

Portfolio Construction

- Core‑Satellite: Private Credit or traditional fixed income as core; Cat/ILS as a 5–15% satellite for drawdown reduction and higher risk‑adjusted returns.

- Barbell: Pair income‑generating private credit with uncorrelated Cat/ILS event risk; adjust tactically as spreads and expected losses move.

- Dynamic Overlay: Increase Cat/ILS when insurance spreads/yields are elevated or traditional risks are concentrated.

Future Market Trends & 2026 Outlook

- Issuance & Depth: With significant maturities slated and robust investor demand, issuance momentum is expected to remain strong.

- Perils & Structures: Ongoing expansion into cyber, mortgage, climate‑linked risks with innovative trigger designs.

- Sponsor Base: More insurers/reinsurers/corporates entering, increasing deal flow and diversification.

- Technology & Data: Advancements in cat modeling, analytics, and risk transfer platforms improve transparency and pricing efficiency.

- Policy Evolution: As familiarity grows, allocation constraints are expected to ease.

- Sustainability: Investors increasingly recognize Cat/ILS’ role in supporting climate resilience and disaster recovery, aligning with sustainability goals.

Conclusion

Catastrophe Bonds and ILS have progressed from niche alternatives to essential diversifiers. Their combination of uncorrelated event premia, low volatility, and strong risk‑adjusted performance is particularly valuable in an environment marked by macro uncertainty and concentration risks. When implemented with diversified vehicles, robust manager selection, and alignment to liquidity and governance needs, Cat/ILS can unlock resilient performance long hidden in plain sight.

Sage believes Cat Bonds & ILS are increasingly compelling for astute investors designing 2026 strategies. The sector’s robust historical record, near‑zero correlation to equities/core bonds, and demonstrated resilience during stress support both diversification and return optimization objectives. In a year likely to be defined by macro cross‑currents and heightened focus on sustainability, Cat/ILS stand out because they:

- Provide true uncorrelated exposure that can materially reduce portfolio volatility and drawdowns.

- Deliver higher risk adjusted returns relative to many credit segments and the US Aggregate benchmark, enhancing the overall risk/reward posture of a diversified portfolio.

- Exhibit stability during market downturns, cushioning portfolios when credit spreads and equities widen.

- Channel capital toward resilience, supporting communities’ recovery from disasters—an increasingly central pillar of investor sustainability frameworks.

- Move the efficient frontier meaningfully, per MPT, enabling higher expected returns for a given risk or lower risk for a given return.

Bottom Line

For investors seeking resilient, future‑ready portfolios in 2026 and beyond, Cat Bonds & ILS should no longer be overlooked or underutilized within alternative or traditional allocations.

References

- Swiss Re Capital Markets — Global Cat Bond Index performance & market insights; issuance/sponsor trends.

- Cliffwater CDLI — Private Credit performance metrics and methodology.

- Eurekahedge / With Intelligence ILS Advisers Index — Net returns, methodology, and index construction.

- Artemis — Cat/ILS market reports and sector commentary.

- Bloomberg — Bloomberg US Aggregate Bond Index historical performance (annualized trailing returns).