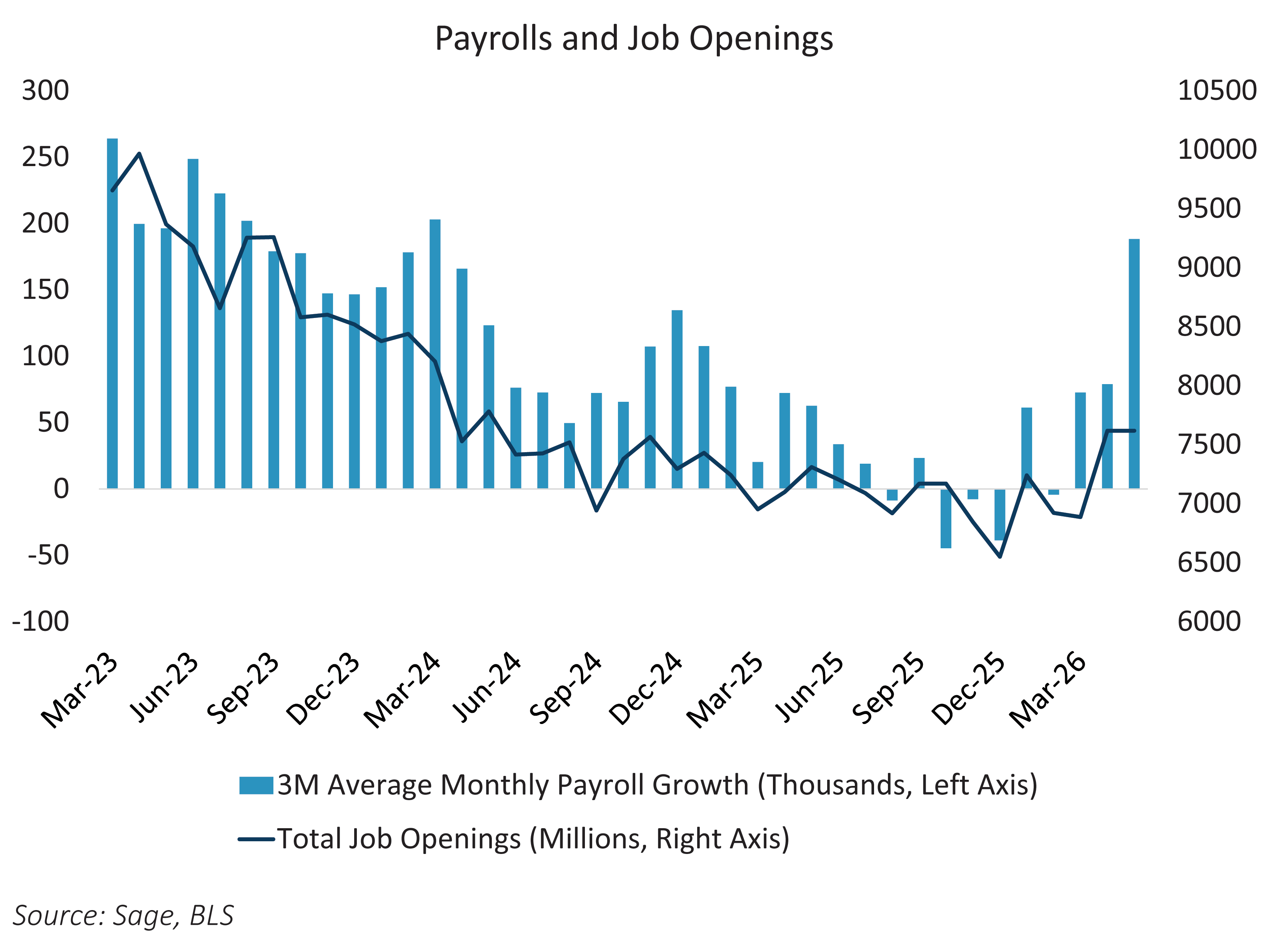

Volatility and the US economy are both heating up just in time for summer. May’s non-farm payrolls landed at 172k, blowing past expectations to the upside, while upward revisions totaling 93k across the prior two months lifted the three-month average to a robust 188k. The unemployment rate declined on the back of that strength, and ADP corroborated the picture with a healthy 122k print. JOLTS job openings surged by 731k to 7.62 million in April, well above consensus, even as the quits rate fell to 1.9%, the hiring rate dipped to 3.2%, and the layoff rate declined to 1.1%. Taken together, the labor market, which had stagnated to start the year, now looks unambiguously strong.

This strength persists despite fears of AI-driven displacement and rising energy costs from the closure of the Strait of Hormuz. We believe the Fed will likely remain on hold through the rest of the year rather than hike rates, but there is little impetus for lower bond yields if the economy and labor market continue to march forward while inflation fears linger. The bar for cuts keeps rising, and the bar for hikes, while still high, is no longer out of sight.

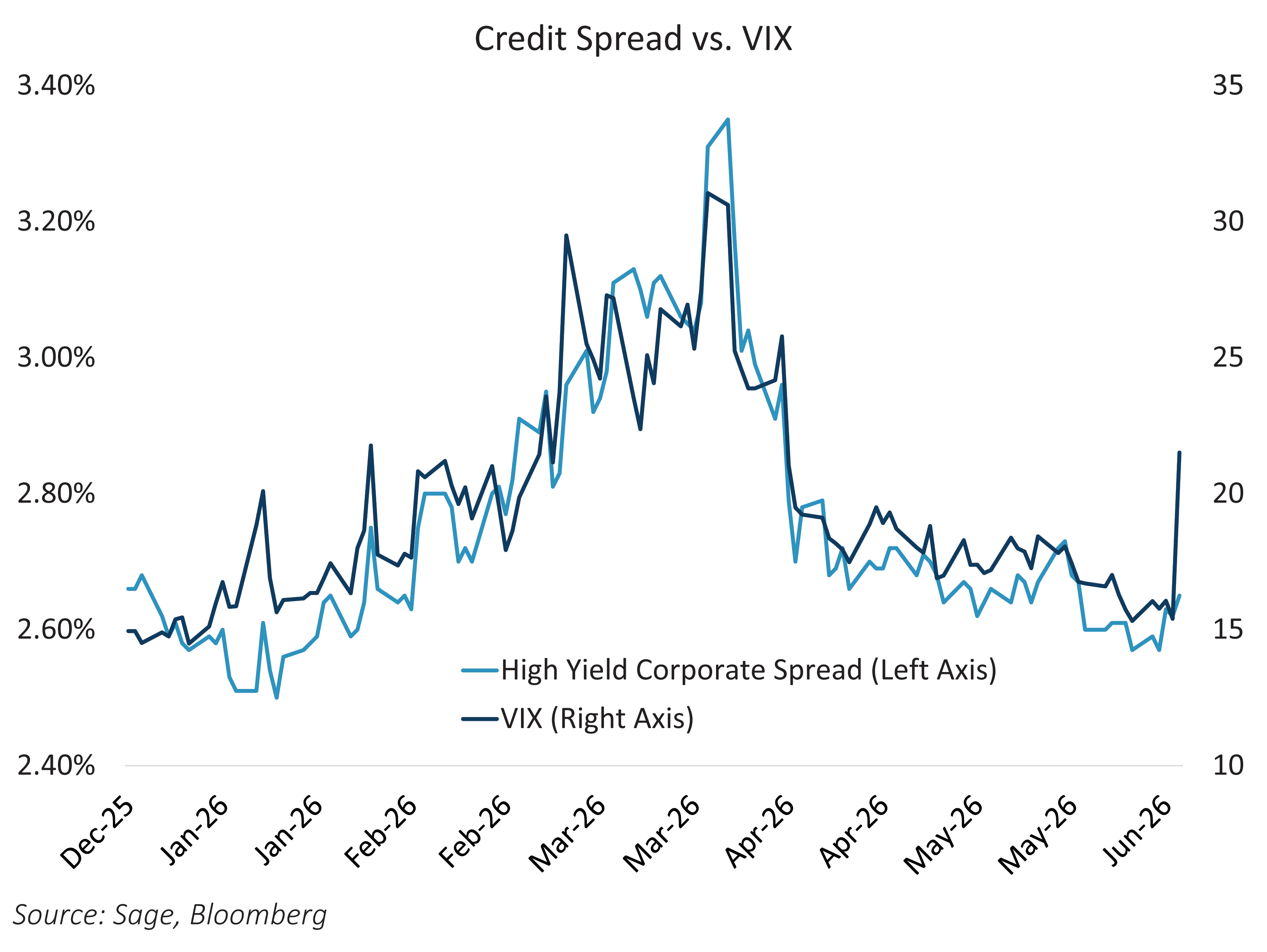

Risk sentiment took a hit last week, particularly in the highest-octane segments of the market. AI and momentum equities led the selloff as questions around funding sustainability moved to the fore. Alphabet announced $85 billion in equity issuance to fund the data center buildout, ahead of SpaceX’s anticipated $75 billion IPO later this month and looming public offerings from both Anthropic and OpenAI. Meta has reportedly explored equity raises in the “tens of billions” as well. The sheer volume of equity supply, combined with crowded positioning and stretched valuations, sent equities lower. Credit, however, did not participate in the stress.

The VIX spiked to 21, but high yield spreads only widened from 262 to 265 basis points, and investment grade corporate spreads moved from 72 to 73 on Friday, June 5th, reflecting little immediate fallout to credit markets. One interpretation is that heavy equity issuance could actually reduce the need for debt financing, all else equal, helping credit technicals. It is also possible that credit simply has not caught up yet. Risk sentiment globally could deteriorate further in the coming days given the overhang from the Iran conflict, as well as next week’s CPI print and Fed Chair Warsh’s first FOMC meeting. For now, though, credit is not signaling widespread stress, and the divergence between equity volatility and credit spreads is worth watching closely as summer gets underway.