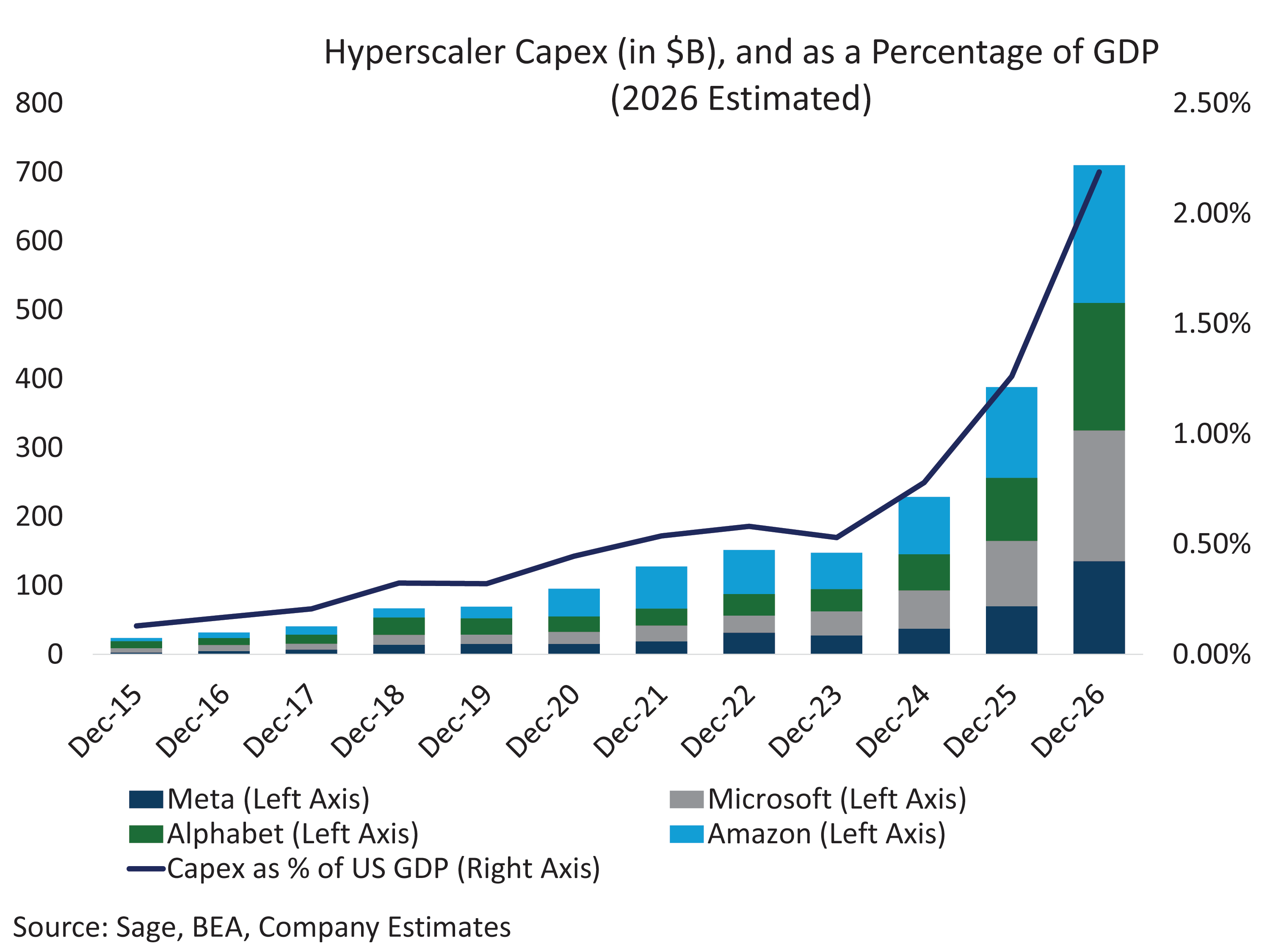

The crescendo of AI-related spending is affecting all corners of the capital markets. Debt financing has been especially impacted this year given the epic financing needs of the largest hyperscalers. The big four — Meta, Microsoft, Alphabet, and Amazon — are slated to spend at least $700 billion in 2026, roughly 80% higher than 2025’s record figure. That amounts to 2.2% of GDP in AI capex from these four names alone, before accounting for the many other companies investing at similar scale.

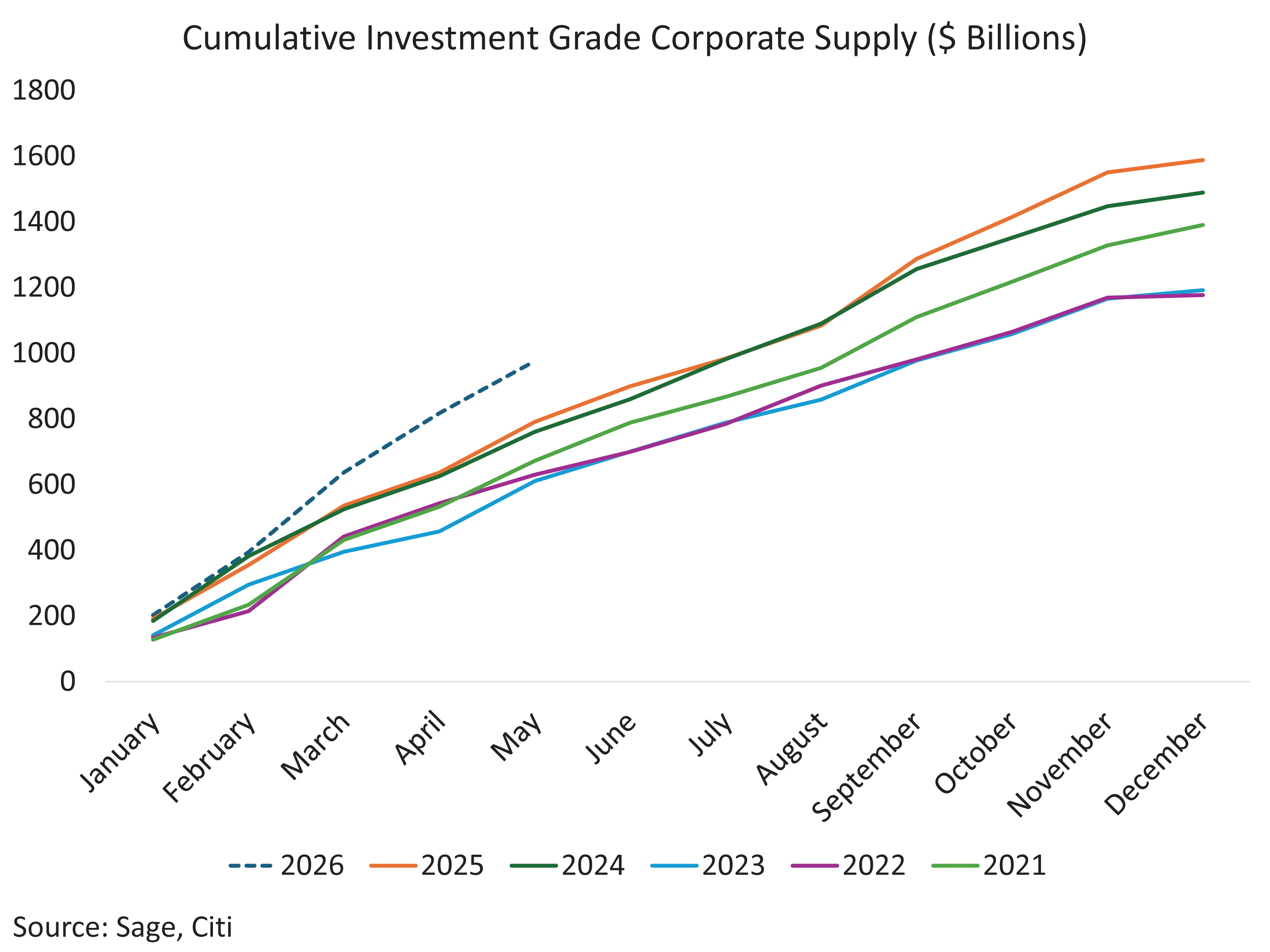

These capex plans do not come cheap, and the debt markets are bearing much of the load. Investment grade corporate issuance has already cleared $976 billion through May, running well ahead of the record pace set in each of the past five years, including 2025 — itself a record. Hyperscalers are the marginal driver: Alphabet, Amazon, Meta, Microsoft, and Oracle have priced roughly $110 billion of US paper year-to-date, accounting for nearly 16% of IG issuance, versus just 3% a year ago.

Yet spreads have barely flinched as demand is meeting supply. IG spreads sit near 80 basis points, consistent with the tightest levels since the mid-1990s. Yield buyers, such as pensions, insurance companies, and other liability-driven allocators have absorbed the supply, happy to harvest all-in yields that remain above 5% for IG corporates, even as spread compensation shrinks.

Spreads this tight leave little margin for error. A rebound in M&A activity, a stumble in hyperscaler return on AI investment, or a bout of supply indigestion could easily reverse positive sentiment on corporates. Hyperscaler spreads already trade more than 25 bps wider than the broader IG index, a 10-year high, hinting that the market is beginning to differentiate among issuers. Spreads are priced for a perfect AI capex cycle, but the supply imbalance will eventually correct through a buyer’s revolt. Whether that comes in three months or three years is uncertain, but the current spread setup leaves little cushion when it does. All-in yields still look attractive; however, with corporate spreads offering little downside protection, we prefer to source yield from sectors with better risk-adjusted compensation.