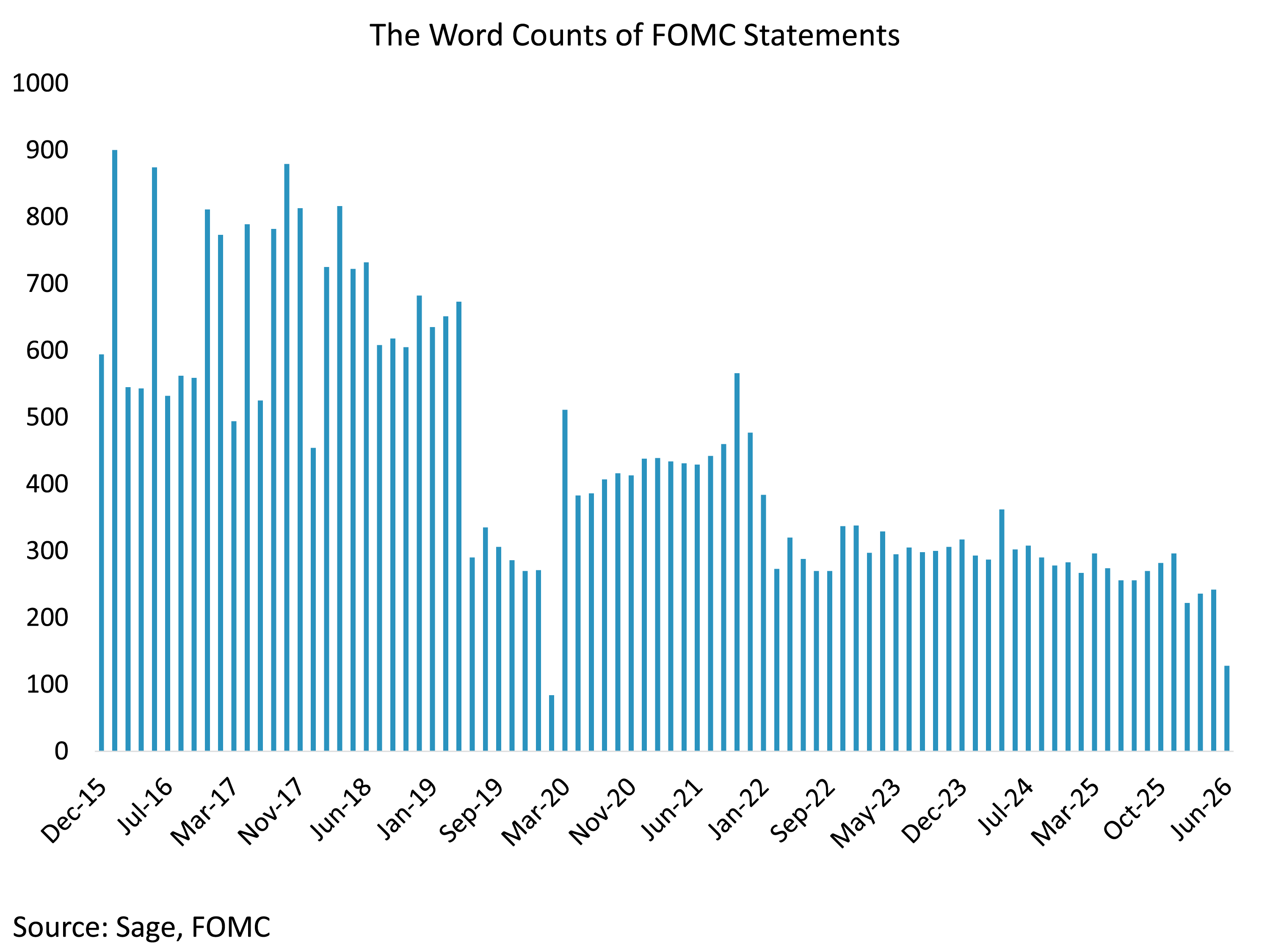

The June FOMC statement ran just 131 words, its shortest outside of the COVID emergency cut, and a 45% reduction from March. Brevity, it turns out, was the point. Chair Kevin Warsh used his first meeting to signal a clear departure from the Powell-era reliance on forward guidance, and markets are now recalibrating to a Fed that intends to say less.

Last week, oil prices retreated sharply as Fed policy returned to center stage — reinforcing that these are the two factors driving US fixed income markets in 2026. Most of the move higher in yields has come from the FOMC’s pivot from a cutting bias to an “on hold” stance, with oil acting as the secondary driver through inflation expectations.

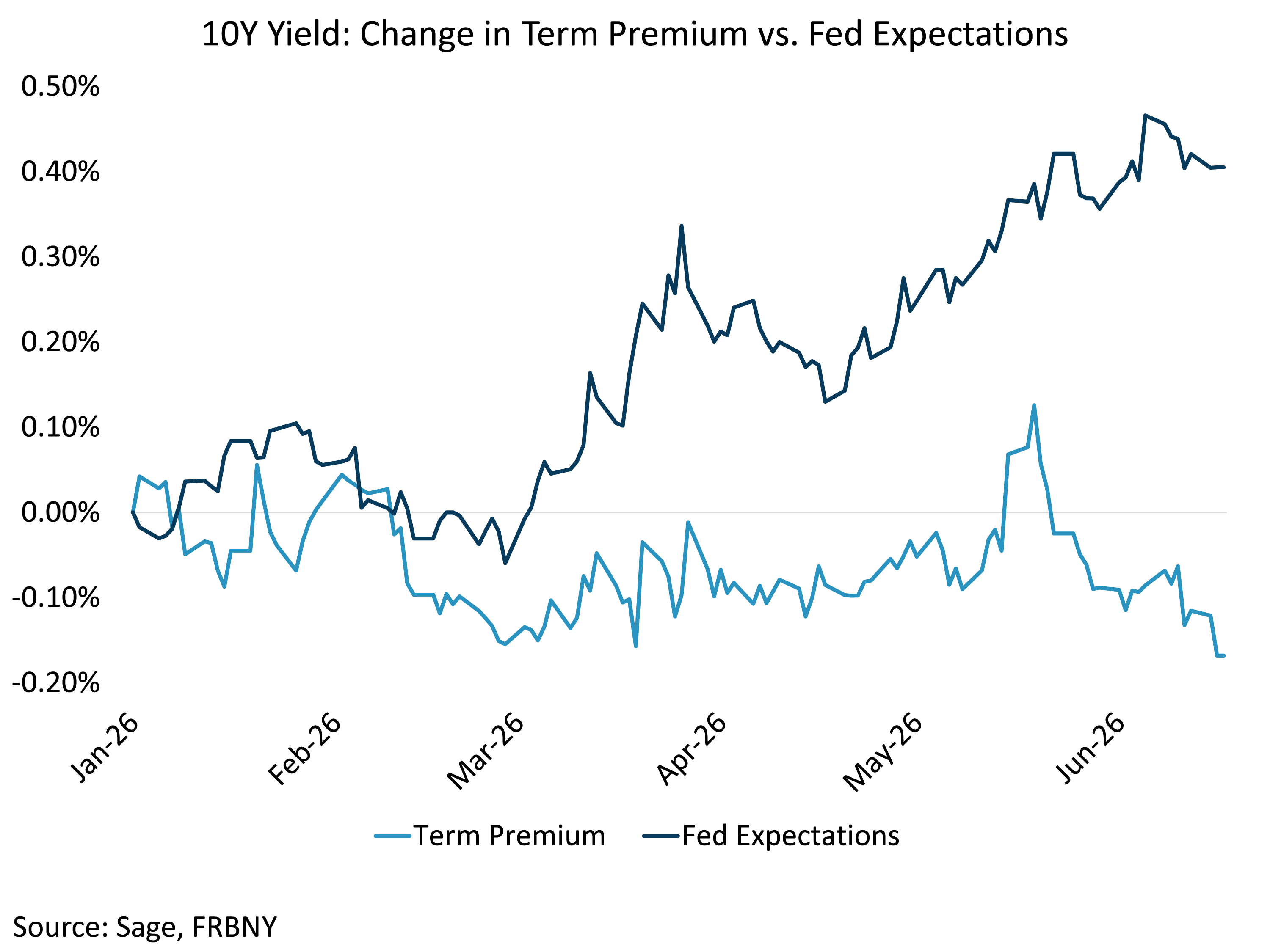

Decomposing the Move in Yields

Theoretically, changes in the 10-year Treasury yield can be broken into two components: the market’s expectation of the path of short-term interest rates set by the Federal Reserve, and the term premium –the extra yield investors demand for locking up their money in longer-duration bonds rather than rolling shorter-term securities. Fed expectations are shaped by incoming economic data, as well as the Fed’s own communication on the policy path. The term premium reflects a broader set of risks: fiscal sustainability, Treasury supply, inflation persistence, and geopolitical risk.

With this framework in mind, the year-to-date story becomes clear. As the chart below shows, the entire 2026 move higher in the 10-year yield has come from the expectations component — term premium has actually compressed.

The yield curve has repriced from a modest easing cycle at the start of the year to one that now prices a rate hike by year-end. Meanwhile, the decline in term premium suggests that headlines around fiscal deficits and the un-anchoring of inflation expectations have not played an outsized role in driving yields higher — at least not yet.

A Hawkish Hold

On Wednesday, the FOMC delivered a hawkish hold — no move on rates, but a notably tougher tone. The statement dropped the easing bias language that had persisted under Powell, replacing it with neutral language and an emphasis on price stability that opens the door to tightening. The dot plot shifted higher, as we expected, with the median now projecting one 25-basis-point hike by year-end and rates remaining on hold through 2027.

Notably Warsh, consistent with his long-standing skepticism of forward guidance, did not submit his projections to the dot plot. That same philosophy showed up in the statement itself: at 131 words, it was the shortest non-emergency statement on record.

Less Guidance, More Volatility

Warsh’s press conference emphasized the committee’s commitment to price stability and the decrease in forward guidance, hinting at more changes to come through the formation of task forces around Fed communications, balance sheet policy, data sources, productivity and labor, and inflation frameworks. This reduction in forward guidance will be a cornerstone of the Warsh Fed.

For investors, the implications are meaningful. Less information from the committee shifts the burden of price discovery onto the market and should raise rate volatility around key economic releases like CPI and payrolls. With task forces yet to report and the policy framework still in flux, more unknowns lie ahead. In a regime where the Fed says less, markets will have to say more — and Fed policy will remain the dominant driver of rate moves in the months ahead.