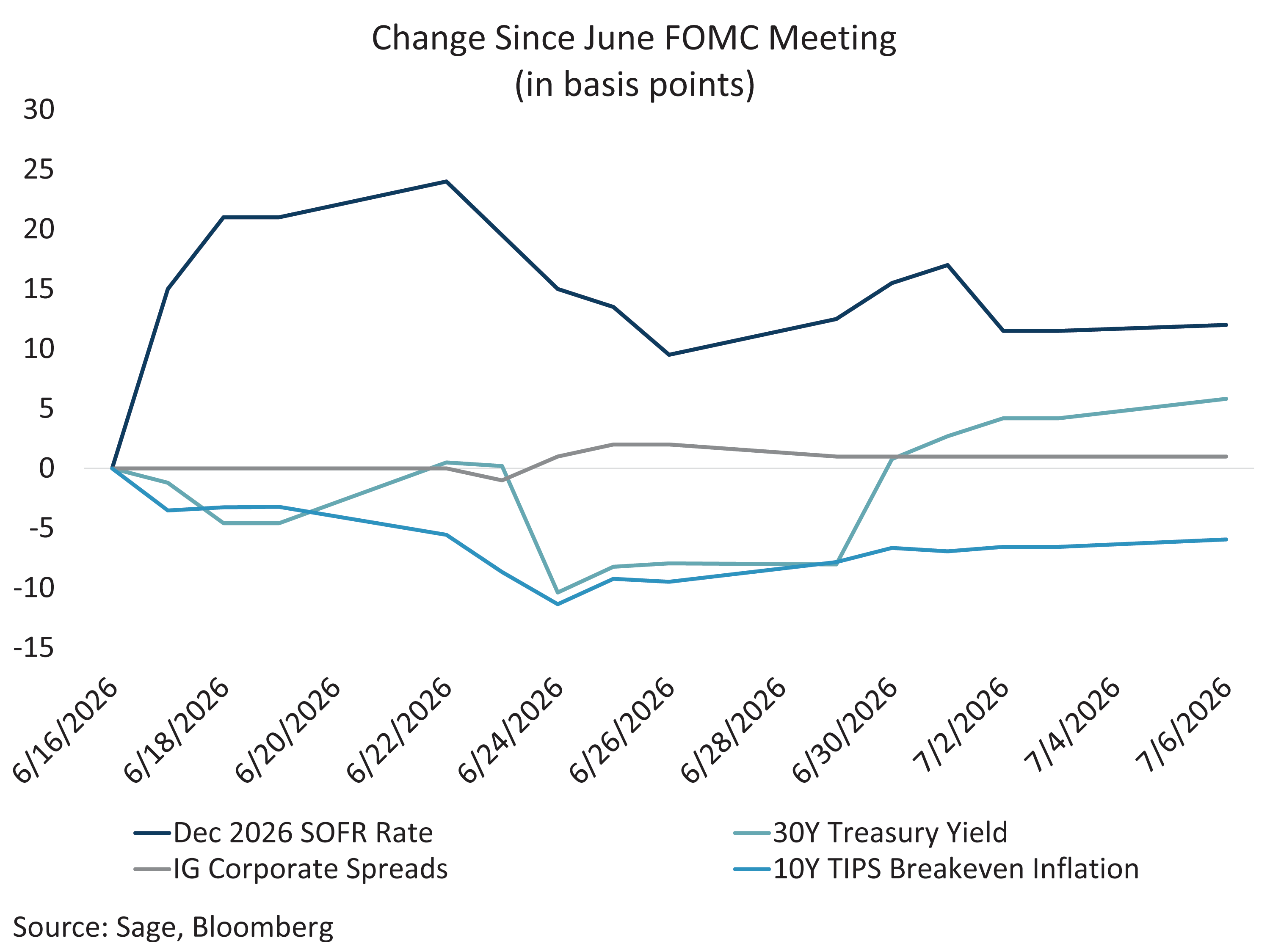

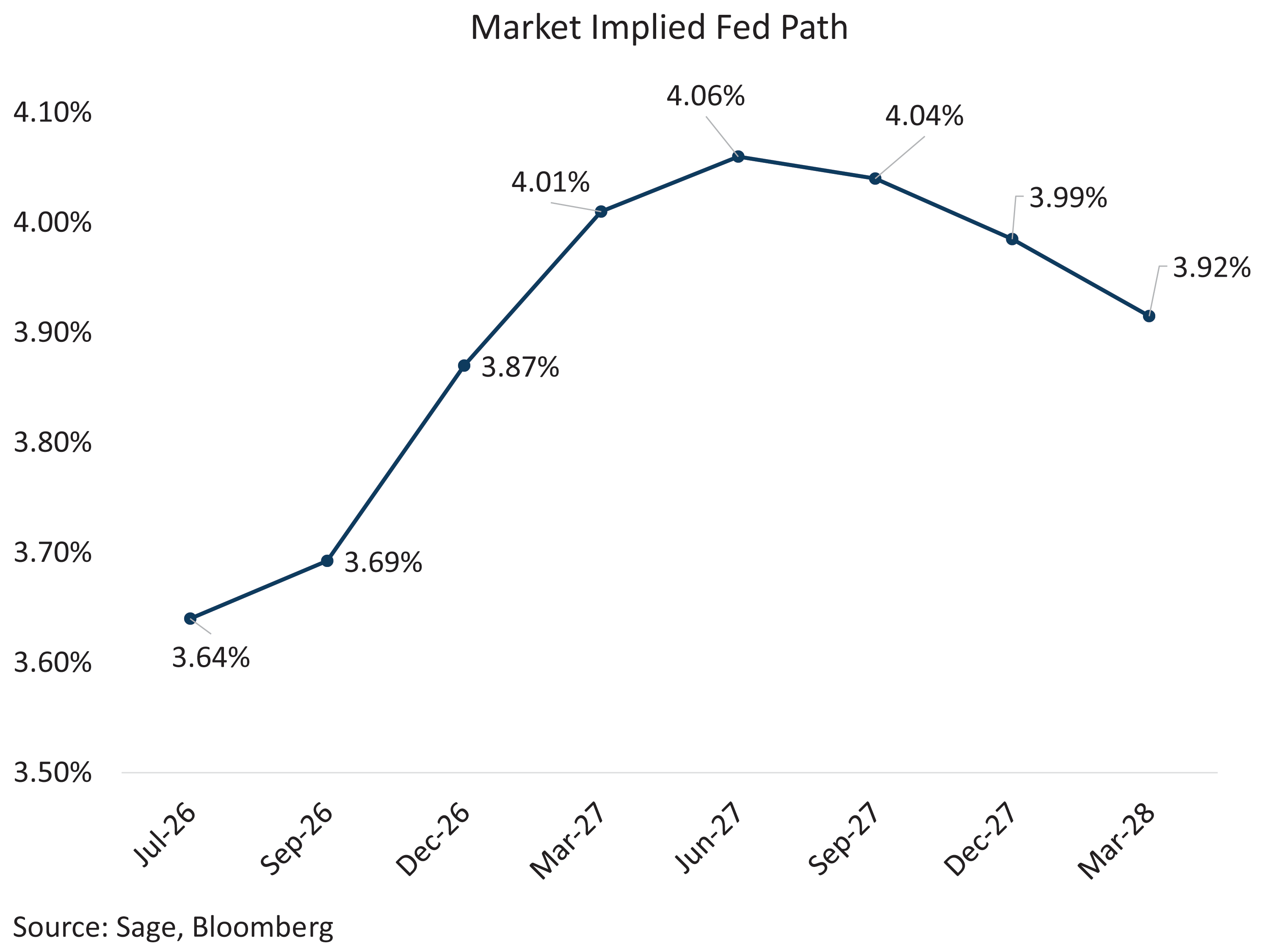

The June jobs report took the pressure off an immediate July rate hike. Payrolls came in soft at +57,000, while the unemployment rate ticked down to 4.2% on a lower participation rate, which fell to 61.5%. Market-implied odds of a July hike faded, and the front end of the yield curve rallied in kind. The opening days of Fed Chair Kevin Warsh’s tenure have been successful if judged by market reaction — his credibility pledge on inflation has priced in rate hikes while anchoring long-term interest rates, lowering breakeven inflation, and keeping risk assets and credit intact.

Despite softening labor growth, the Fed’s path from here does not run through the labor market. It runs through inflation, which remains elevated relative to FOMC targets — something Warsh emphasized in his remarks at and since the FOMC meeting. Shelter disinflation has flattened out, the goods deflation that did so much heavy lifting last year is fading as tariff effects filter through, and services ex-housing has stalled at a pace inconsistent with 2%. If inflation holds at current levels, we expect the Fed to hike rates by year-end.

The Fed regime shift has ushered in a truly data-dependent environment, where each print carries more weight than in prior cycles. Warsh’s more balanced tone at Sintra landed without a meaningful pickup in volatility — a sign the market is respecting his credibility for now. That credibility buys the Fed room, not a free pass; it holds only as long as inflation continues to grind toward target. The next several CPI prints will do more to set the path for rates and risk assets than labor reports through the balance of the year.