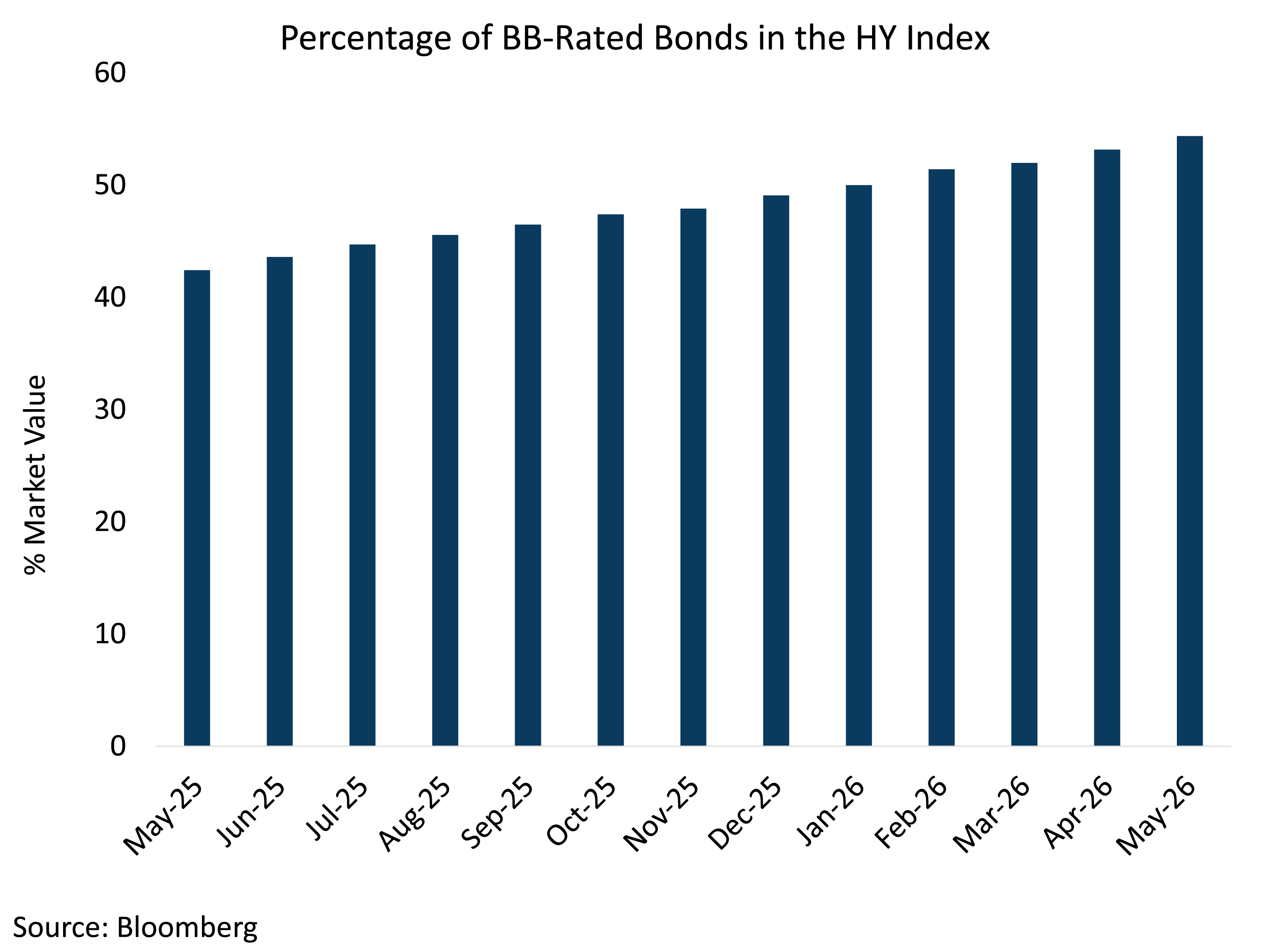

Despite high yield spreads trading near the tighter end of historical ranges, improving structural ratings quality and a healthy earnings backdrop support a compelling case for remaining invested in the asset class. The high yield market has undergone a meaningful structural shift in recent years, with BB-rated issuers now representing the majority. Lower-quality companies have largely migrated out of the market, increasingly appearing in adjacent asset classes, such as leveraged loans and private credit. This shift is closely tied to changes in where lower-quality borrowers are accessing capital.

Despite high yield spreads trading near the tighter end of historical ranges, improving structural ratings quality and a healthy earnings backdrop support a compelling case for remaining invested in the asset class. The high yield market has undergone a meaningful structural shift in recent years, with BB-rated issuers now representing the majority. Lower-quality companies have largely migrated out of the market, increasingly appearing in adjacent asset classes, such as leveraged loans and private credit. This shift is closely tied to changes in where lower-quality borrowers are accessing capital.

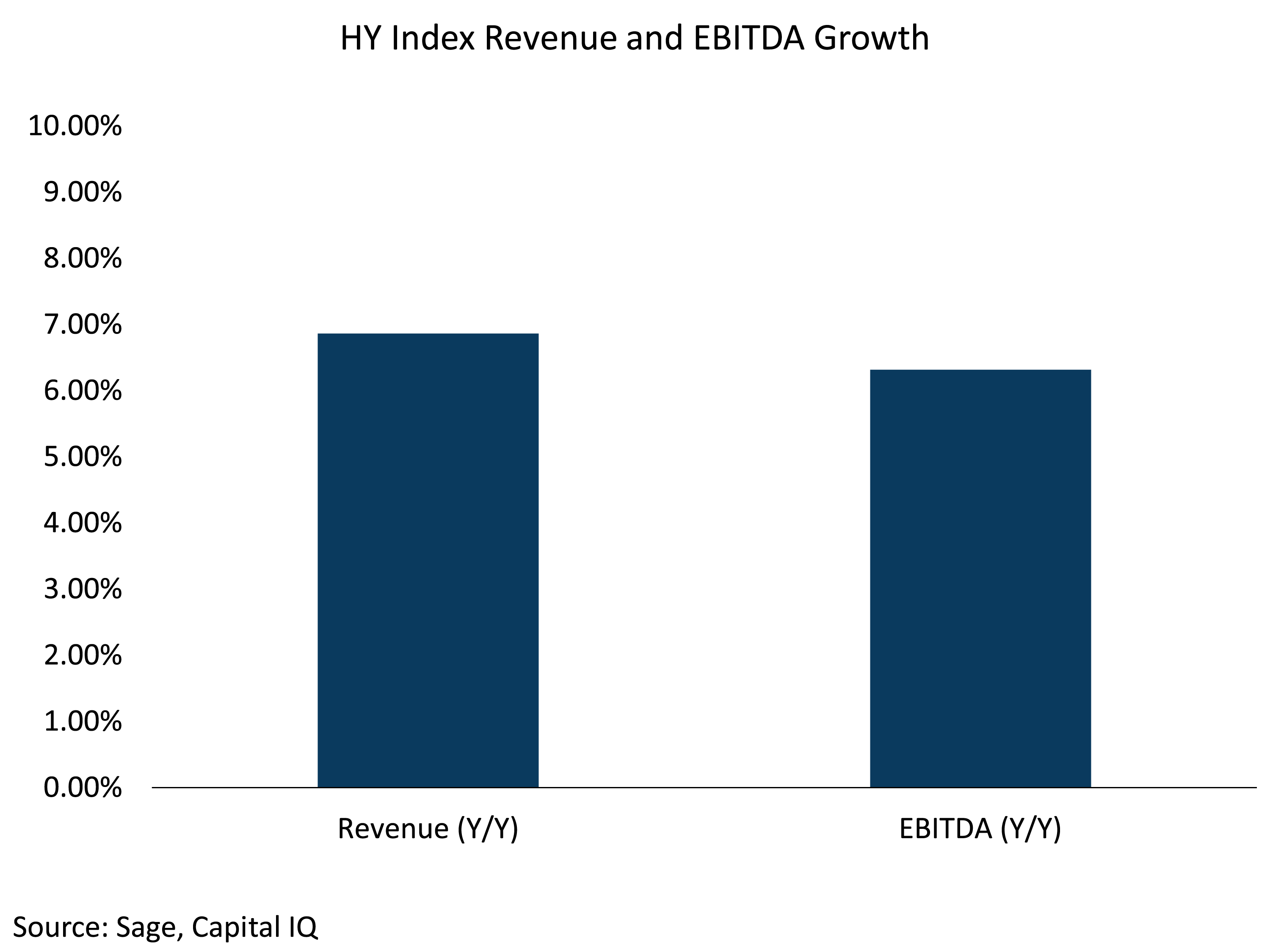

Fundamentally, 1Q earnings reflected the fastest revenue growth since 2022, led by strength in technology, metals, and energy. These sectors have been key beneficiaries of the ongoing buildout of artificial intelligence infrastructure. Importantly, performance has not been concentrated in a few sectors. 1Q26 total revenue growth for members of the HY index hit 7% YoY, while EBITDA grew 6%. The market continues to exhibit broad-based resilience, with most industries delivering year-over-year growth, supportive of overall credit quality.

While high yield spreads remain tight and fundamentals are stable, divergence has begun to emerge across leveraged credit markets. Private credit is showing early signs of deterioration, while leveraged loan spreads have started to widen. Loan spreads are now closer to their median levels, reflecting heavier exposure to lower-quality single B and CCC issuers.

These segments have underperformed and face a shortening maturity profile. The volume of loans approaching refinancing over the next several years is at a multiyear high, suggesting a potential increase in credit stress ahead. In contrast, the high yield market appears more insulated from these dynamics. Against a backdrop of a still-constructive macroeconomic environment, total return potential for high yield remains attractive.