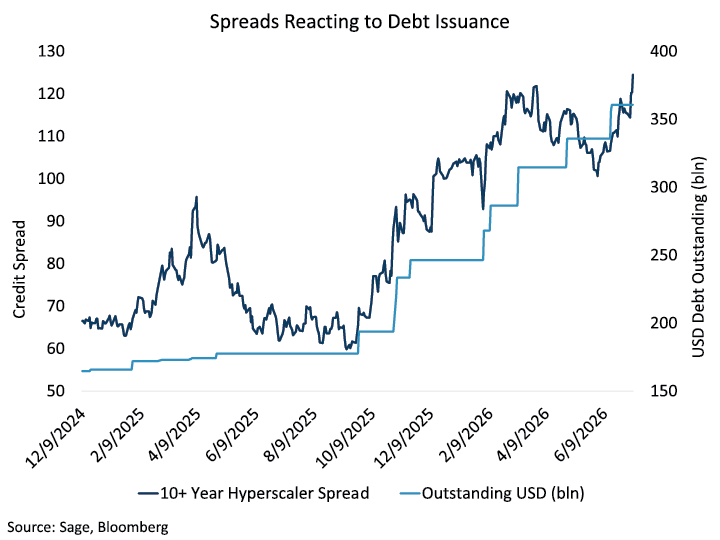

Hyperscaler issuance tied to the AI buildout remains the dominant theme in the investment grade market. Last week, Amazon issued $25 billion, marking the ninth deal this year larger than $20 billion, with seven of those transactions linked to hyperscalers. The Amazon offering came as a surprise to the market, pushing its existing 30-year bond, which was issued earlier this year, 20 basis points wider as investors demanded additional concession to absorb the latest wave of supply.

This supply dynamic has been the primary driver of hyperscaler underperformance in 2026. Each successive jumbo deal has pressured spreads wider before they eventually stabilize and experience modest rallies. Since September, the hyperscalers, which include Microsoft, Meta, Google, Oracle, Amazon, and Nvidia, have more than doubled their collective U.S. dollar debt footprint to over $360 billion. As the AI buildout has accelerated, these companies have increasingly turned to the capital markets for funding amid declining organic free cash flow generation. This debt deluge does not include the money hyperscalers have raised in other currencies and in other structures, such as off-balance-sheet leases.

Importantly, this has occurred against a generally favorable fundamental credit backdrop. Ratings pressure has remained limited, particularly among the highest quality issuers, which continue to maintain AA ratings. While leverage has begun to trend higher across the group, net leverage remains at extremely healthy levels, and hyperscalers have begun to supplement debt financing with equity issuance to reduce the ultimate impact on their balance sheets.

As earnings season approaches and management teams provide updated guidance, investors broadly expect capex growth to remain elevated but begin to moderate heading into 2027. As a result, future spread performance is likely to be driven by the pace and magnitude of issuance needed to fund the next phase of AI investment.