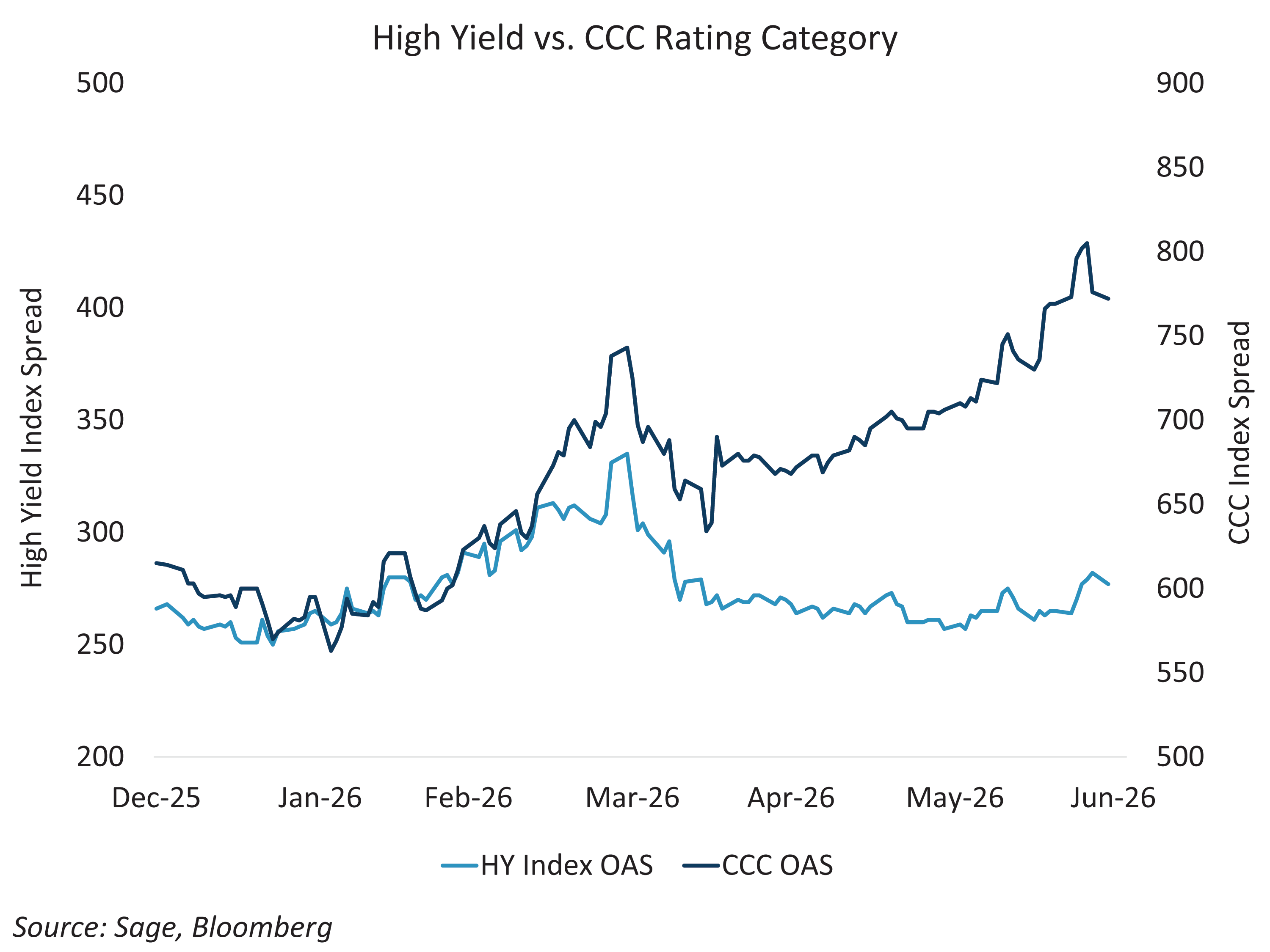

Despite an overall improvement in high yield credit quality, the lower-quality CCC-rated segment across both high yield bonds and leveraged loans is beginning to show clear signs of stress, with pronounced underperformance relative to single-B and BB-rated issuers. Year-to-date, this divergence has emerged as one of the most notable developments in leveraged credit, with weakness appearing earlier in the year and initially concentrated in technology-related issuers.

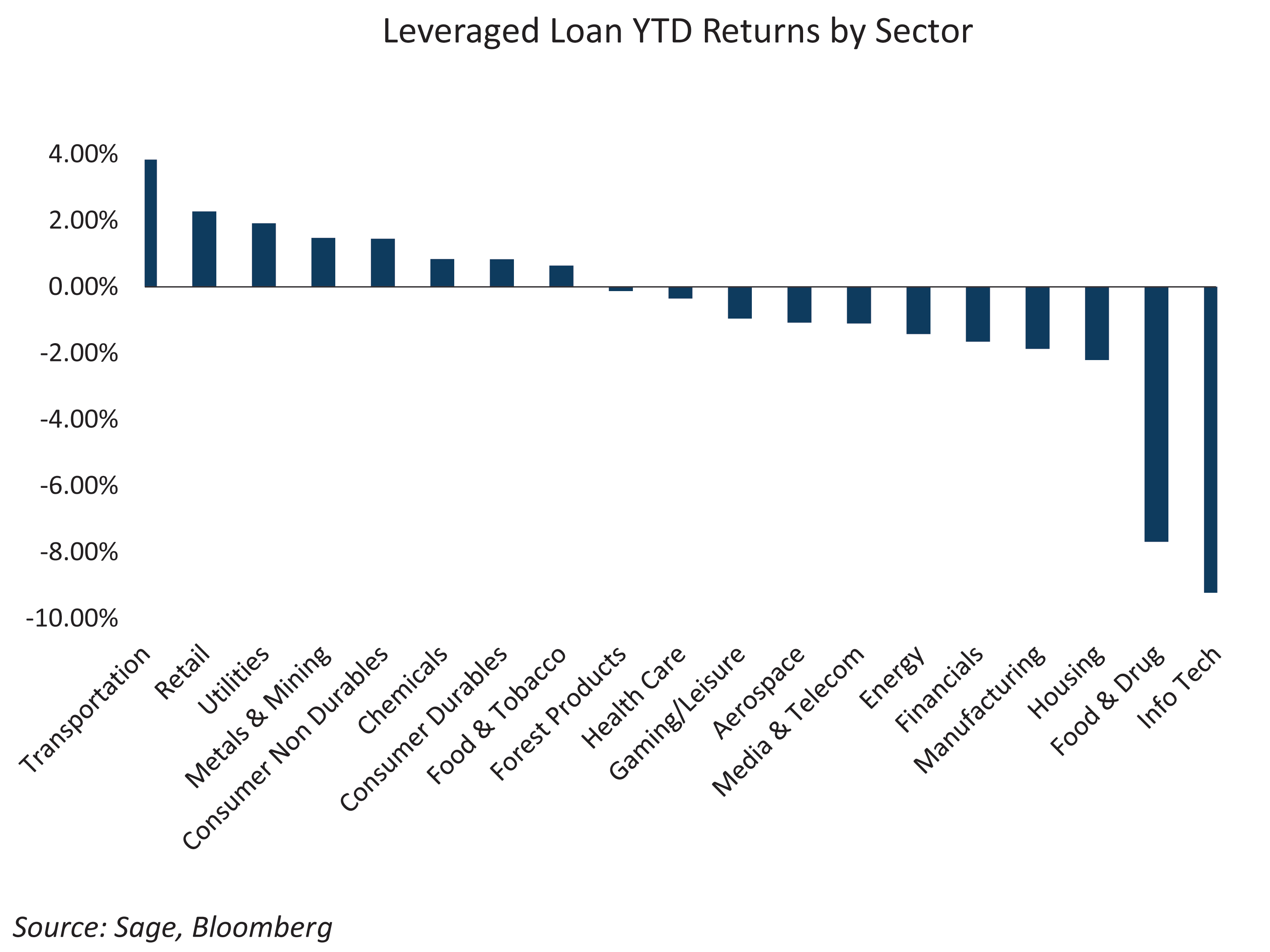

In leveraged loans, performance has largely reflected a sector-specific dynamic. Underperformance has been most evident in information technology, down 9.2% year-to-date, and in the food and drug sector, down 7.7%.

In contrast, the high yield market has experienced a more broad-based repricing. While technology weakness led initially, spread widening has expanded in recent weeks to include insurance, media, and select consumer credits.

To date, the pressure has remained largely confined to CCC-rated issuers, where high leverage and an increasingly constrained funding environment may prove unsustainable for certain companies and business models. This is particularly relevant as investors increasingly reassess earnings durability considering AI-driven efficiency gains that may structurally challenge some cost bases and end-market demand profiles.

CCC-rated credit also represents the closest public market analogue for assessing emerging risks in private credit. As business development companies continue to manage through an elevated redemption wave, CCC weakness may provide an early signal of stress among more highly levered private borrowers, where loan portfolios are only marked to market on a quarterly basis.

Importantly, spread performance has not yet translated into a materially higher default environment. Leveraged credit defaults remain below long-term averages, with high yield bond defaults running at approximately 2.0% compared to a 25-year average of 3.2%.

While the broader economy and overall health of the high yield market remain supportive, trends within CCC fundamentals and spreads warrant close monitoring as a potential leading indicator of future credit deterioration. Moving up in quality remains a prudent way to harvest excess yield.