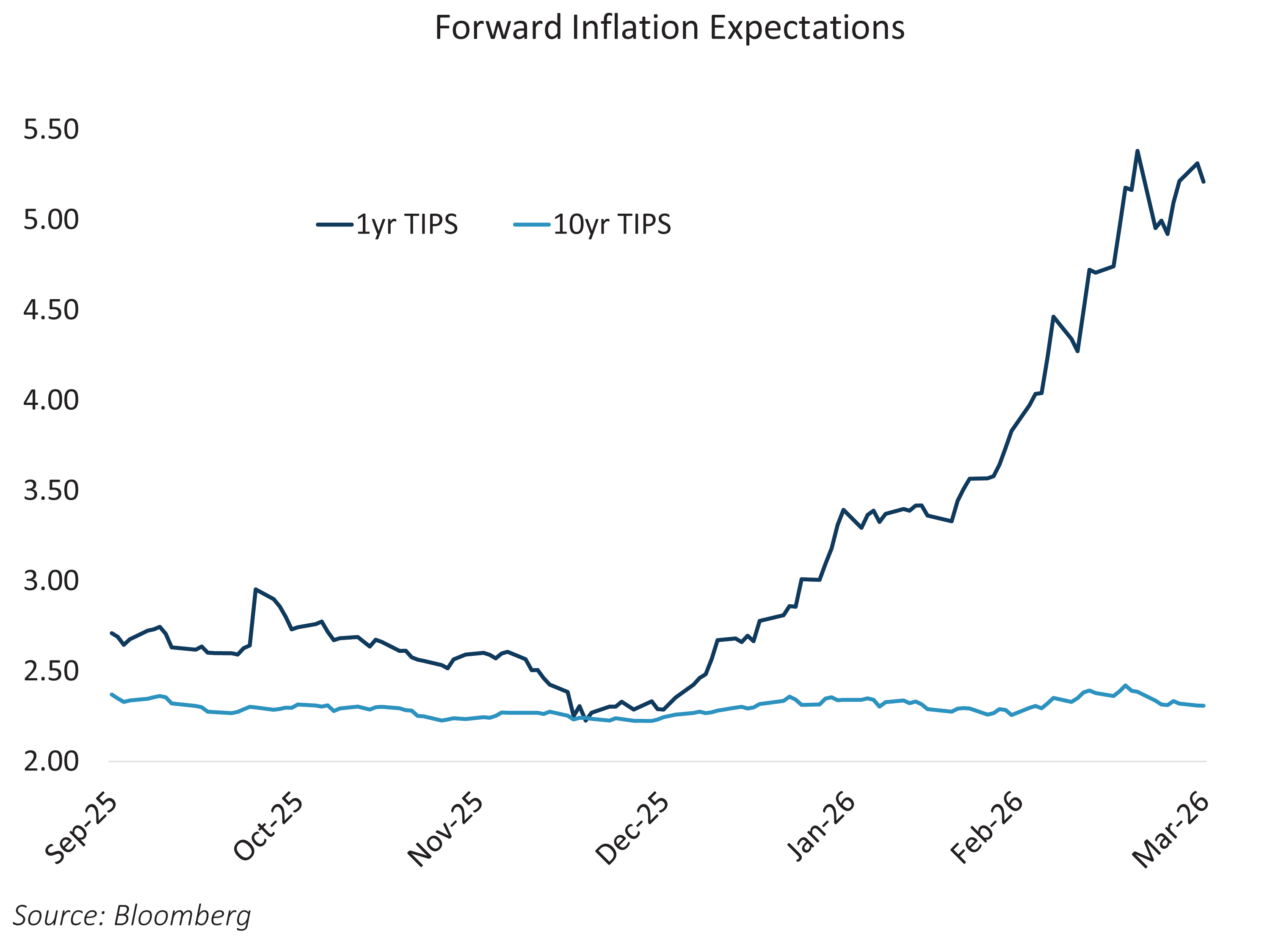

A Panic-Driven Repricing, Not a Fundamentals Shift

Recent moves in the bond market reflect panic selling of duration, not a meaningful re‑anchoring of long‑term inflation expectations. Investors have reacted aggressively to the spike in oil prices and fears of renewed inflation pressure, even though market-based measures of long‑term inflation have remained relatively stable. Fed Chair Powell reinforced this point yesterday, emphasizing that short‑term energy shocks do not automatically translate into a persistent inflation problem. TIPS markets reinforce this view, pointing to stability in long‑term inflation expectations.

What has changed sharply is market psychology and positioning, not the underlying long-term inflation outlook. That distinction matters, because it has created meaningful dislocations across the yield curve.

Sell First Ask Questions Later

The move has been abrupt and defensive, rather than strategic. Investors have rushed to reduce interest‑rate sensitivity amid fears that inflation could re‑accelerate and keep policy tighter for longer. The concern is less about today’s data and more about avoiding exposure if the narrative shifts further toward “rate hikes.” As a result, Treasury yields have repriced aggressively.

This behavior suggests risk aversion, not conviction. The market is prioritizing capital preservation over forward‑looking valuation, even as longer‑term inflation expectations have yet to meaningfully deteriorate.

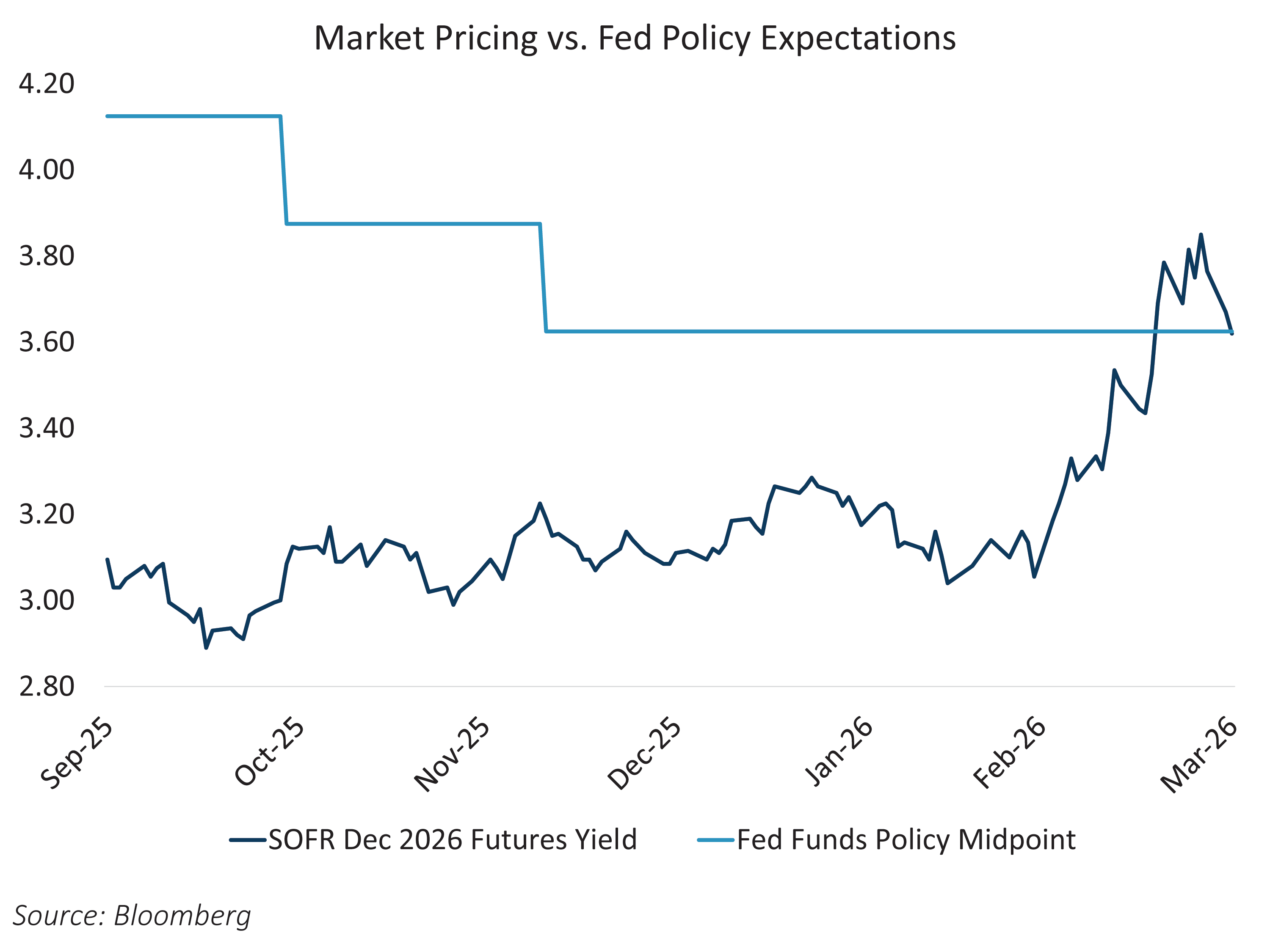

The Speed of This Shift is Notable

Just a month ago, the market was pricing a clear easing path. As of late February, December 2026 SOFR futures implied a policy rate closer to 3.10%, consistent with roughly two Fed cuts by year‑end. Today, that same contract trades around 3.63%, effectively aligning with spot rates and implying no easing at all. That swing represents one of the most dramatic reversals in rate expectations in recent years. Importantly, it occurred without a corresponding surge in long‑term inflation expectations, reinforcing the view that this has been a positioning reset rather than a structural reassessment of inflation risk.

Where We See the Best Value

In our view, the 1‑to‑10‑year maturity range offers the best risk‑reward profile in fixed income today. This part of the curve has fully priced out future Fed cuts while assuming a high level of short‑term inflation pressure. Yields across this segment reflect a pessimistic policy outlook that leaves little margin for further disappointment, while offering materially higher income than was available just a few months ago.

Watch For Asymmetric Upside If Tensions Ease

Looking ahead, current pricing leaves room for asymmetric upside. Any easing of hostilities in the Middle East would likely bring oil prices lower, relieve near‑term inflation pressure, and reopen the discussion around rate cuts. Under incoming Fed Chair Kevin Warsh, that would put policy flexibility back on the table.

In that environment, intermediate‑maturity bonds are well positioned to benefit, offering both durable income today and potential capital appreciation if rate expectations normalize.