Geopolitical risk continues to set the tone for markets, even as price action suggests that many investors are eager to declare the worst is behind us. US equities now sit roughly 3% above levels that prevailed before the Iran war began on February 27, suggesting markets are largely looking past the conflict and expressing confidence in economic resilience and continued corporate earnings momentum. Yet beneath the surface, markets are telling a more complicated story. The energy risk premium has not fully dissipated, with WTI crude still about 30% higher than at the outset of the conflict after peaking nearly 70% above pre-war levels.

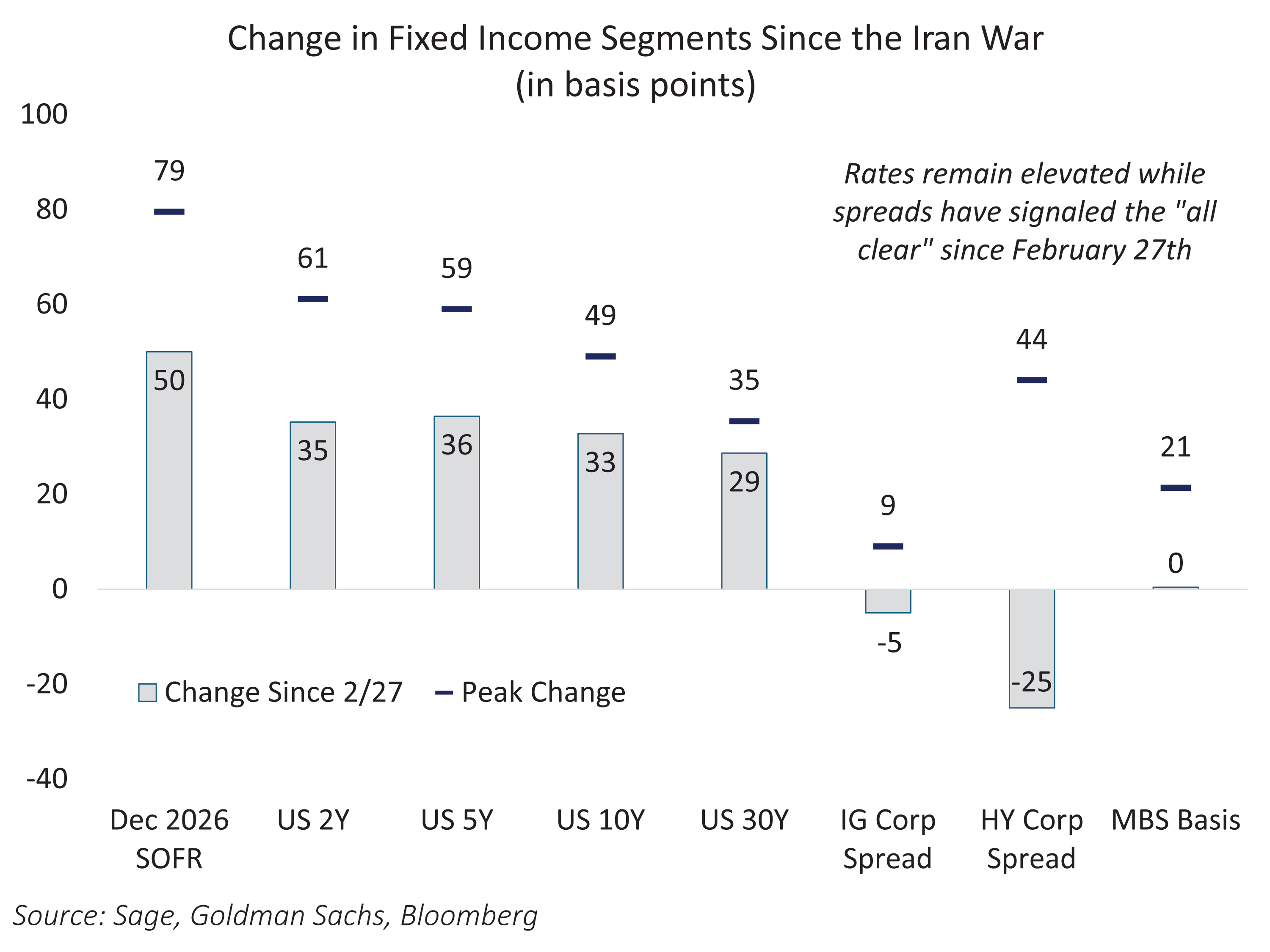

Rates markets remain above pre-Iran war levels. December 2026 SOFR stands at 3.56%, implying that the Federal Reserve remains on hold throughout the balance of this year. That rate is roughly 50 basis points higher than when the conflict began, moving from two rate cuts in 2026 to zero. At the height of the turmoil, December 2026 SOFR traded nearly 30 basis points above current levels, briefly implying that a 2026 hike was at least a non-trivial risk. While that tail risk has faded, it has not disappeared entirely.

Across the Treasury curve, yields remain elevated relative to pre-war levels. Two-, five-, ten- and thirty-year yields are all roughly 30 to 40 basis points higher than they were in late February. This repricing suggests that term premium remains, driven by a combination of energy-related inflation uncertainty, heavy Treasury supply, and a more cautious view of Fed policy.

Credit markets appear far more sanguine in contrast. Investment grade corporate spreads have been remarkably stable throughout the year, widening modestly before tightening back to levels that are now slightly inside where they stood before the conflict. High yield followed a similar, albeit more volatile, path, widening sharply at the peak of geopolitical stress before retracing and now trading meaningfully tighter. Even agency MBS, often sensitive to rate volatility, has fully round-tripped its move, sitting flat versus pre-war levels after briefly tightening by more than 20 basis points.

April has seen a significant reallocation into financial assets, whether driven by the roughly $8 trillion parked in money markets or broader portfolio rebalancing. This flow has provided a powerful tailwind for risk assets, but it does not eliminate uncertainty. The situation in Iran remains fluid, and markets may yet be forced to revisit assumptions that, for now, appear comfortably priced in. Risk assets are increasingly looking through the geopolitical shock and focusing on a still-constructive economic backdrop. If the region settles into some form of steady-state peace and oil prices continue to retrace from their highs, there is room for yields to move lower from here, particularly at the short end of the curve.