On Friday, the labor market surprised to the upside for a second consecutive month, with nonfarm payrolls rising by 115k in April, alongside an upward revision of 7k to March’s initial estimate, bringing the total to 185k. The three month average pace of payroll gains now stands at 48k, even after incorporating the soft February print, and it remains above the breakeven rate of job creation needed to keep the unemployment rate stable. The unemployment rate was largely unchanged in April and currently sits at 4.3%.

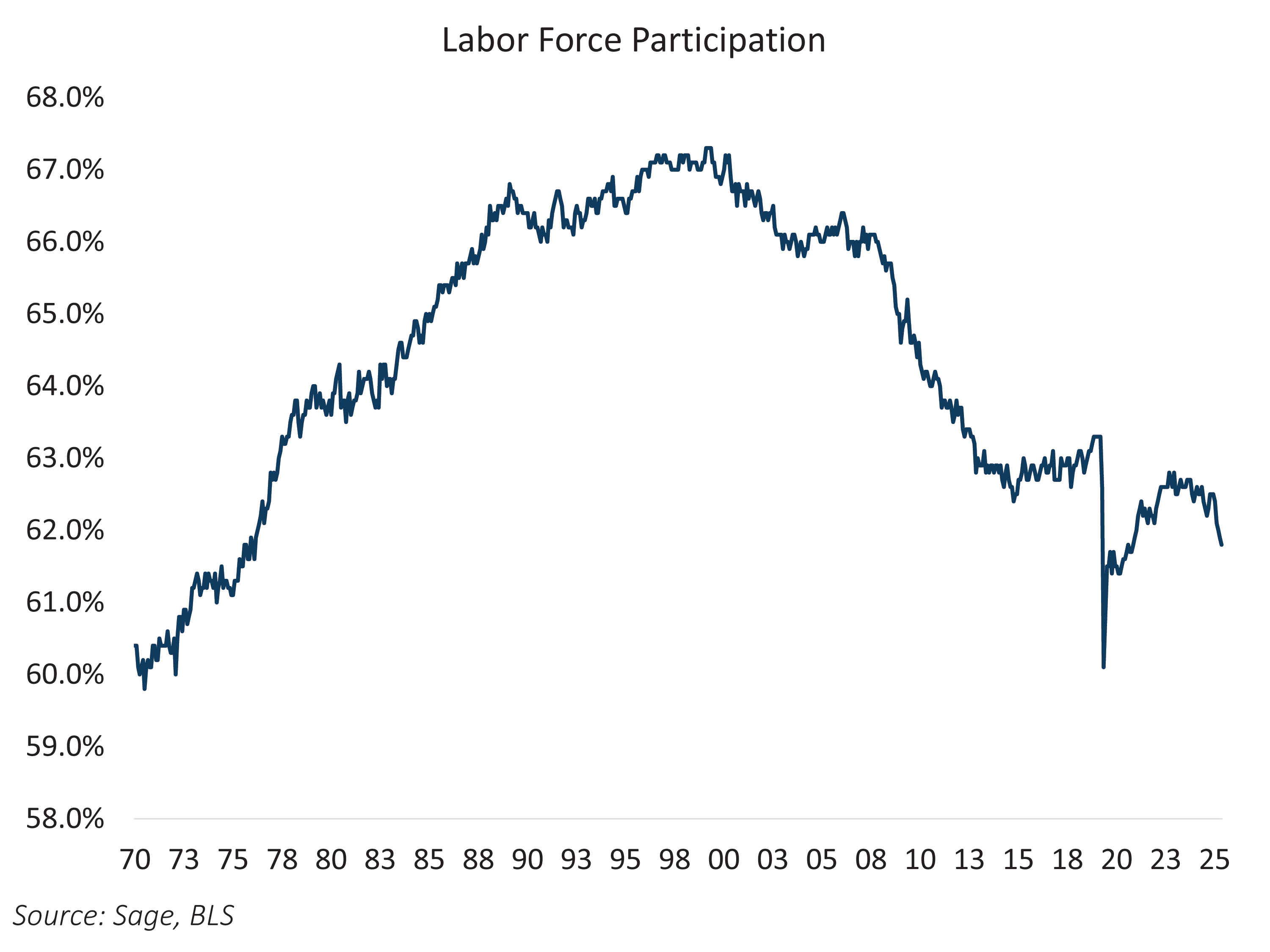

Beneath the headline strength in payroll growth, however, the underlying labor supply picture is weakening. The labor force participation rate continues to fall and sits at the lowest level since the Covid nadir. While the labor market is performing better than expected in 2026, the broader picture suggests ongoing stagnation.

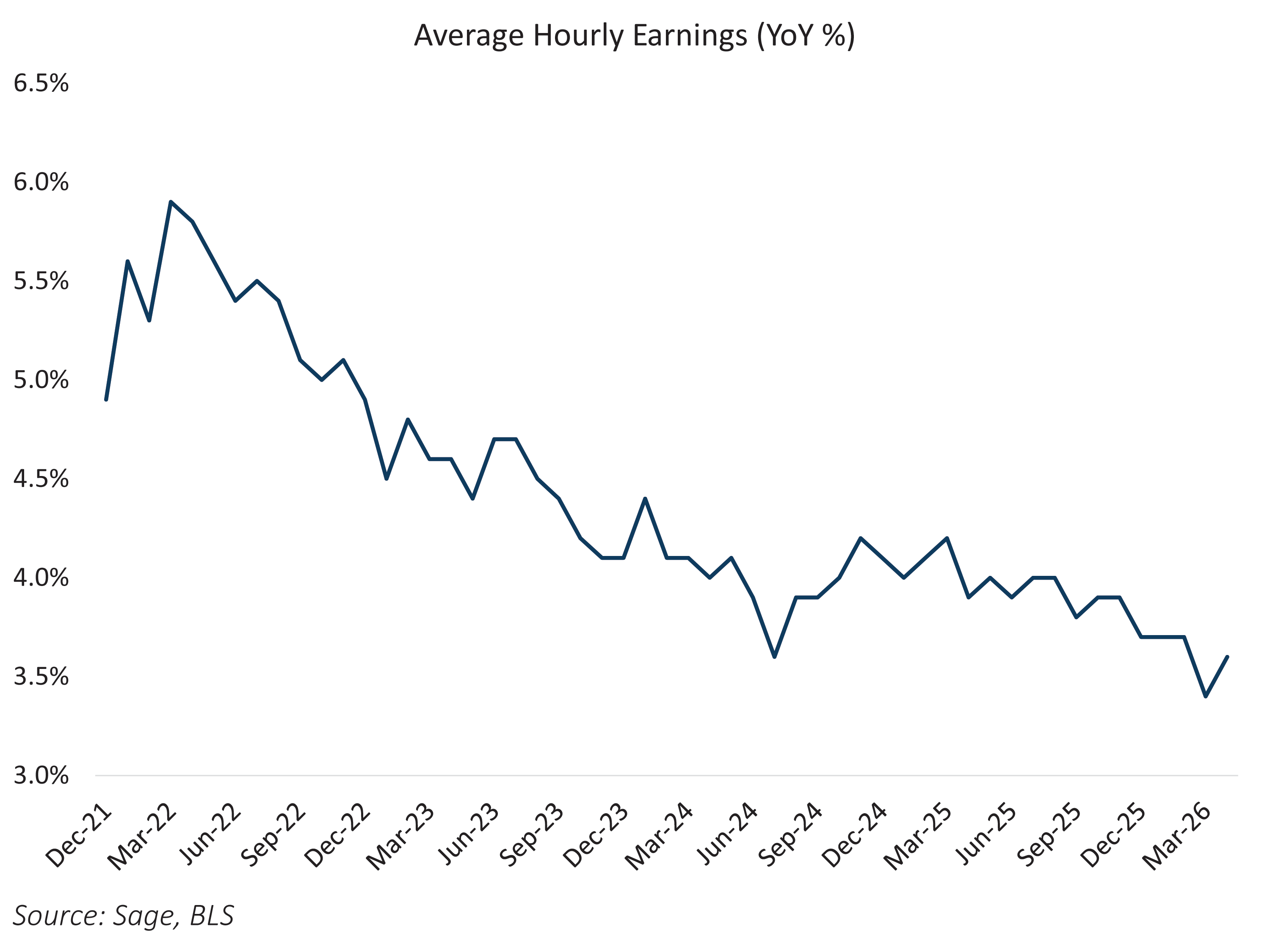

Despite this tighter labor supply backdrop, wage growth remains subdued as inflationary pressures are not yet broad-based enough to affect the downward trajectory of wages.

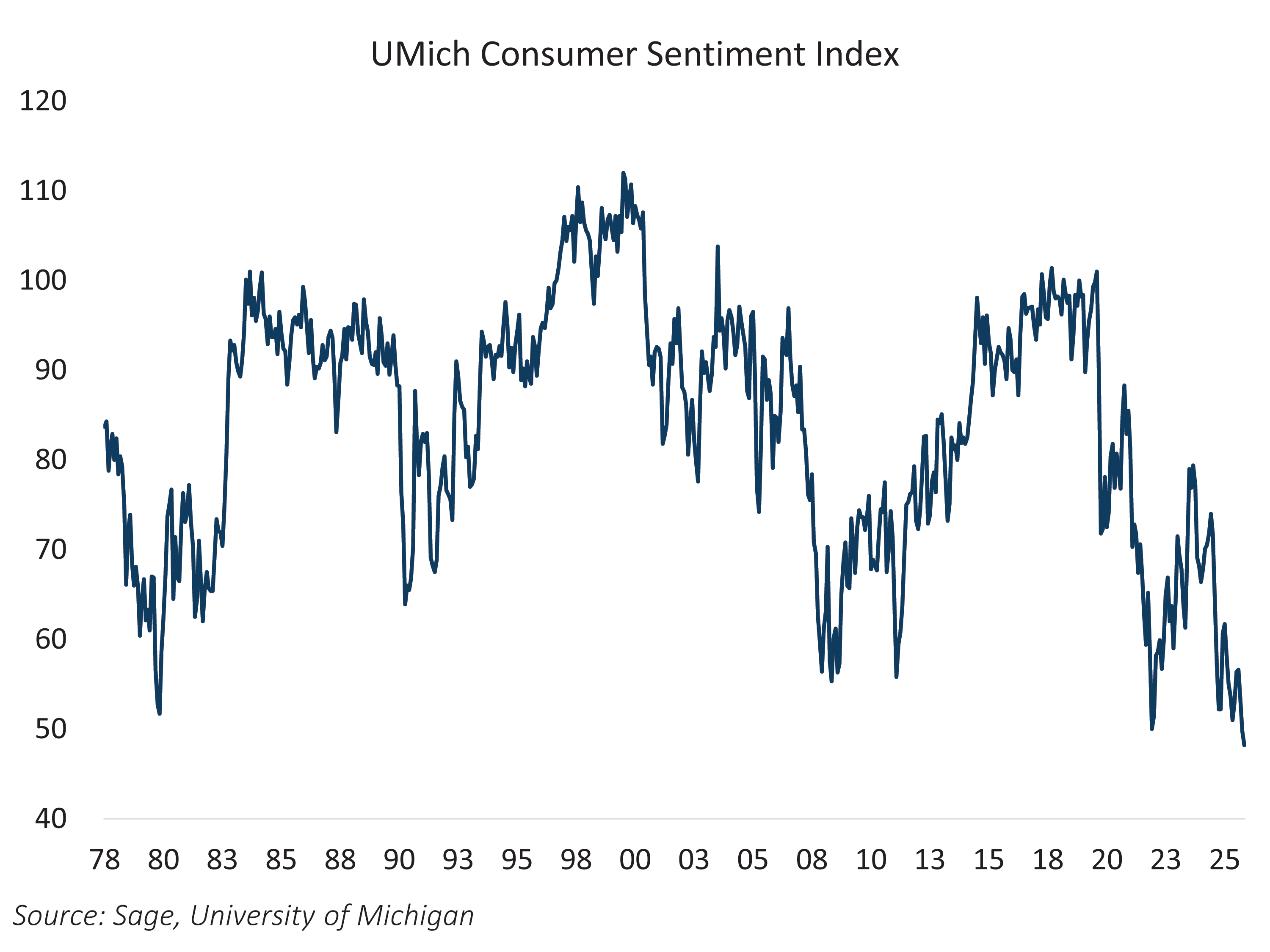

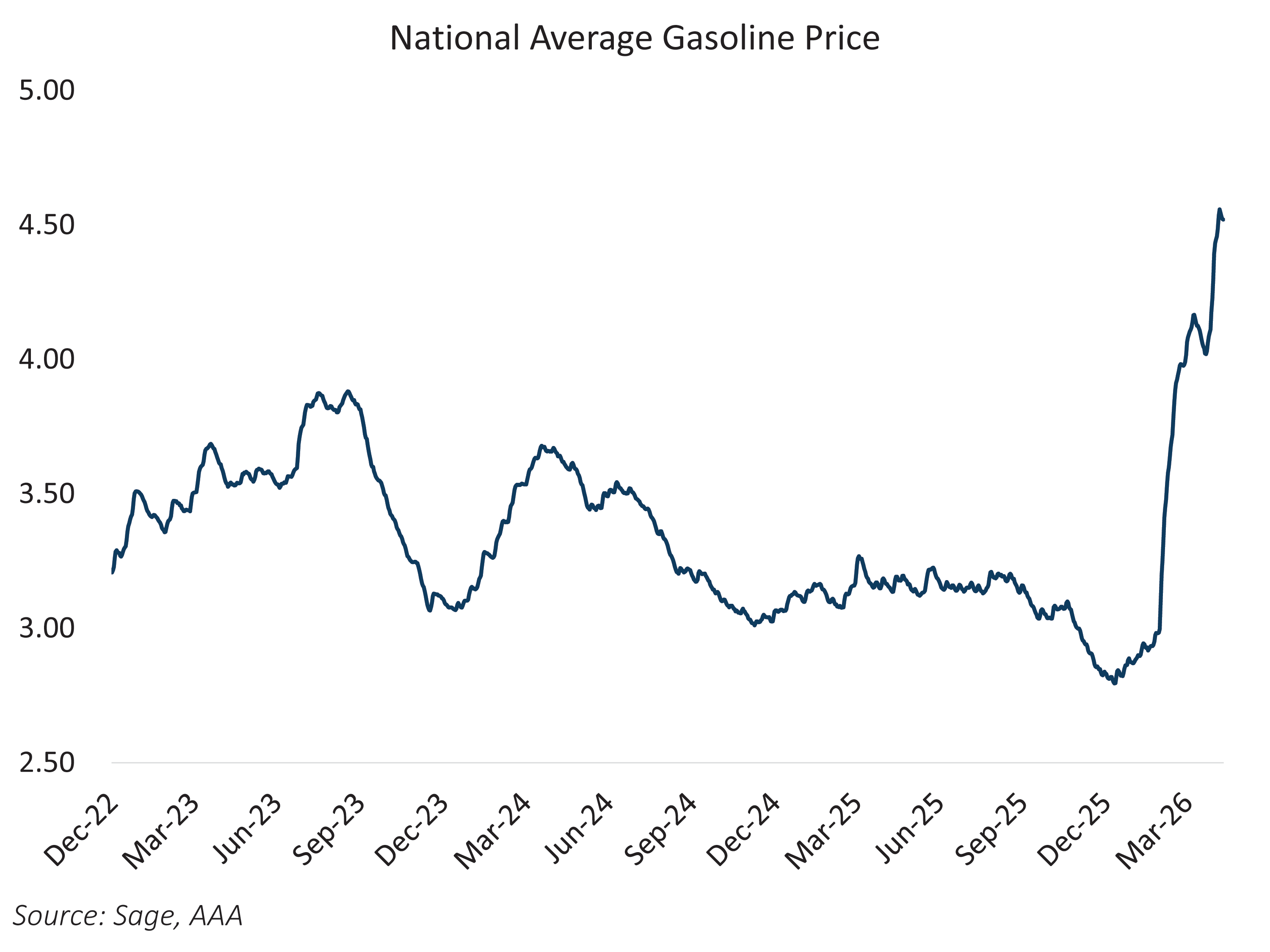

Against this backdrop of muted wage growth, consumer sentiment has deteriorated meaningfully, with the University of Michigan consumer sentiment index now at an all-time low, reflecting growing concerns about the economic outlook as nationwide gasoline prices move above $4.50 per gallon on average.

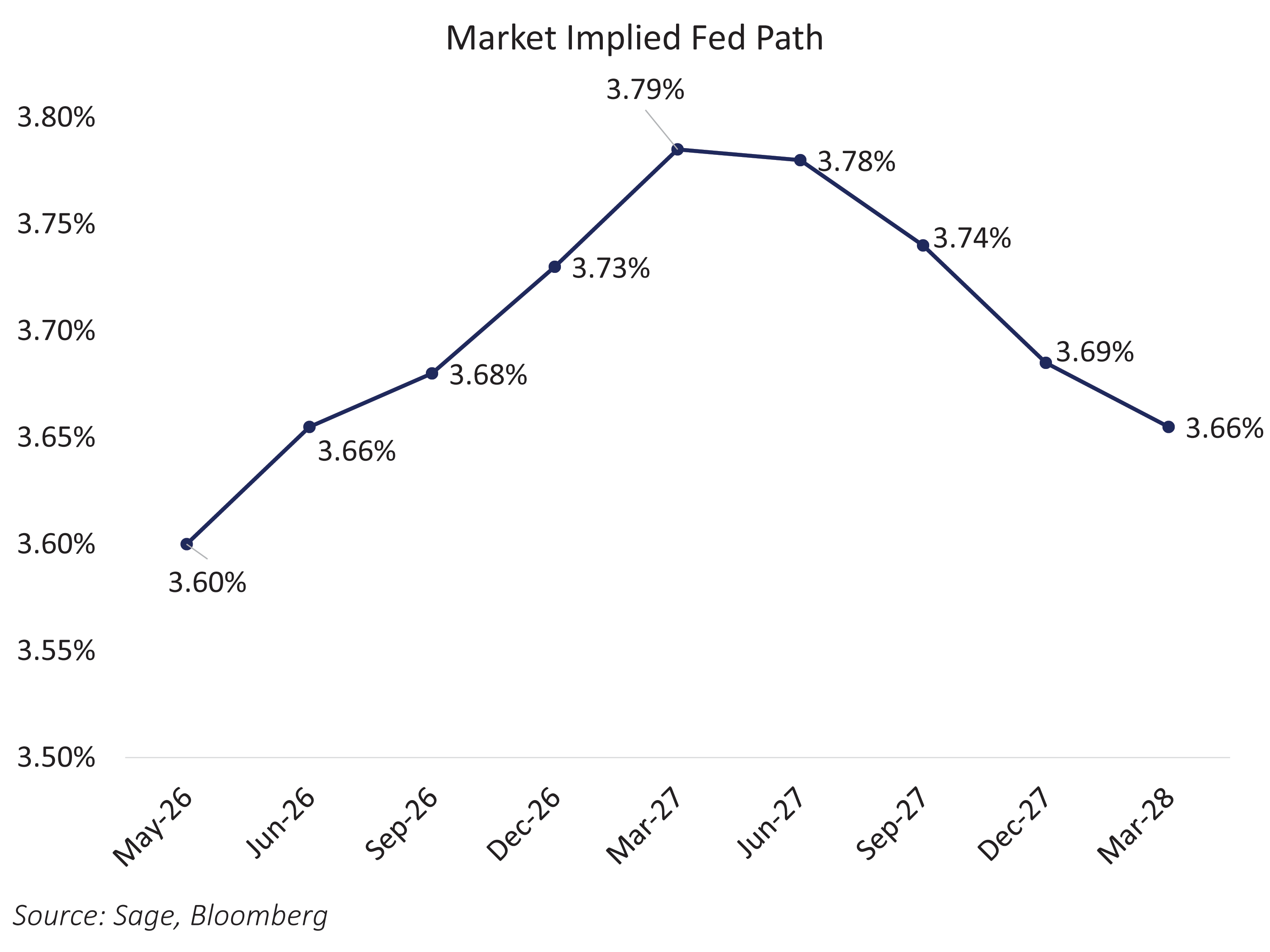

These crosscurrents carry important implications for interest rates. The key question as we transition to a new Fed chair is, what side of the mandate is in the driver’s seat: inflation or full employment? While there are fears around an inflation shock, resulting in a potential rate hike this year, we think that the bar is high for a rate hike and the base case is that the Fed remains on hold through the balance of the year.

Rate cuts continue to face a high bar, as labor markets remain firm enough and the economy still appears to be in a modest expansion. The notion of the Fed losing its independence has faded, as the three dissents, along with Powell’s intention to remain on the Board of Governors, should mitigate any political influence on monetary policy. We believe current conditions warrant neither a rate hike nor a rate cut, but the risk of slowing demand from persistently higher gas prices, coupled with limited near-term economic visibility, should cap further upside in bond yields.