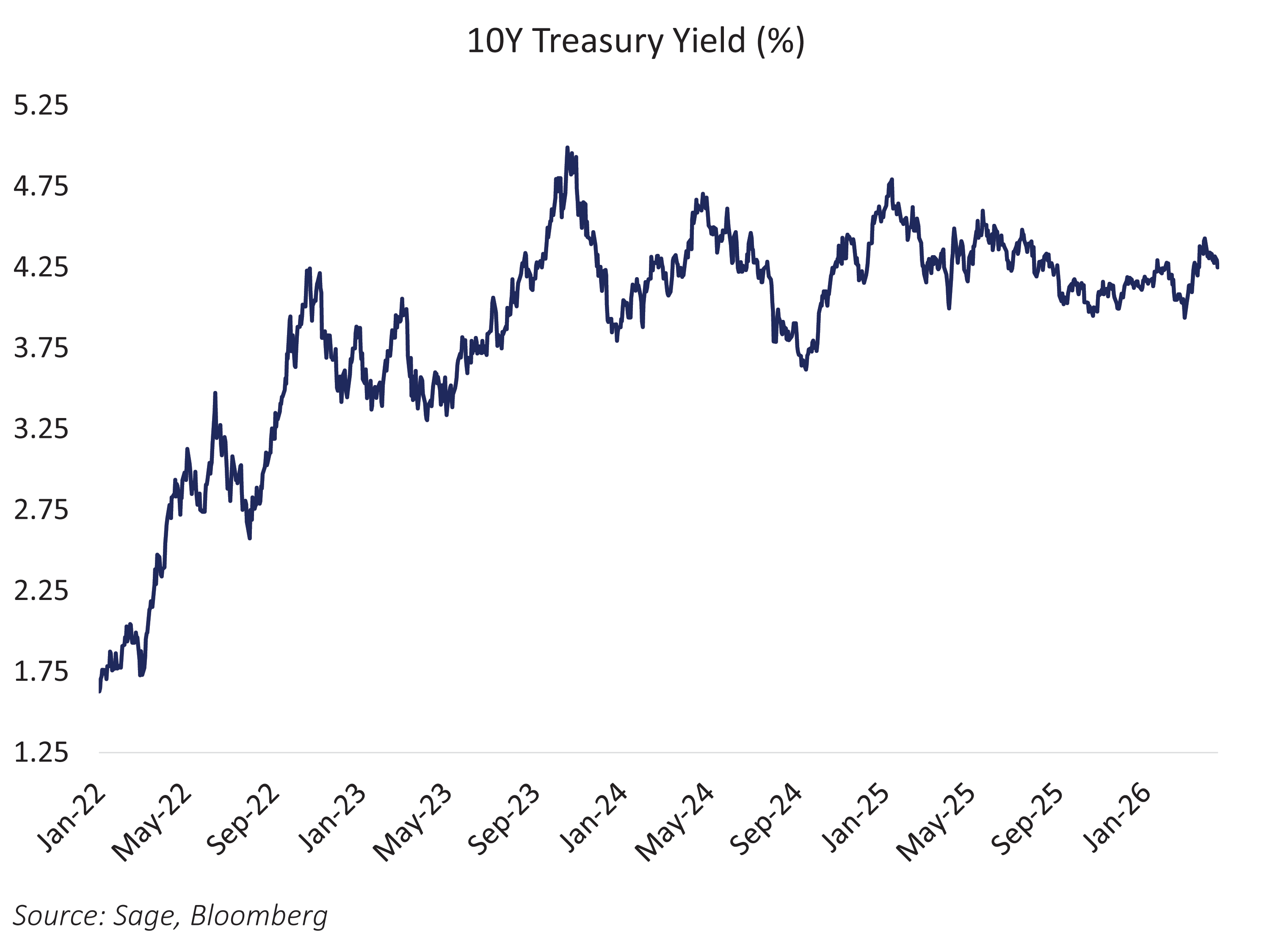

The 10‑year Treasury has been far more stable than recent headlines imply. Since peaking near 5.0% in late 2023, around the time the Fed ended its hiking cycle, the 10-year yield has largely settled into a narrowing range centered near 4.25%. Day‑to‑day moves still attract attention, but these moves have been mostly mean‑reverting. Stepping back, the broader signal has been a rangebound yield, with a modest pull lower as the Fed shifted from hikes to cuts.

Why Investors “Feel” Instability Even in a Rangebound Market

The 10-year is a growth-and-inflation instrument first, and a Fed instrument second. It reacts quickly to incremental data surprises and risk events, even when the underlying regime has not changed. Short‑term swings of 15 to 25 basis points can feel directional when viewed in isolation. They often create a recency bias, tempting investors to extrapolate the last move forward. Yet over the last 2 years, those moves have repeatedly faded. The market has tested both sides of the range and then reverted, reinforcing that the 10‑year has been anchored to an equilibrium level rather than repricing to a new regime.

In this cycle, that anchor has been a mix of:

- a still‑positive real yield (the market demanding compensation for duration and pricing in further economic expansion),

- inflation that is lower than the peaks but not “solved,”

- growth that has repeatedly cooled without breaking,

- and a Fed that has shifted policy direction without committing to a single straight-line path.

The result has been a 10-year yield that trades actively but has not established a durable break higher or lower.

What Yield Stability Implies for Portfolio Construction

Rangebound markets can still feel uncomfortable. Liquidity ebbs and flows. Positioning crowds quickly. Data surprises matter more when conviction is low. That means duration risk often shows up in short bursts. For investors, the discipline is knowing whether a move reflects noise or a shift in fundamentals and sizing exposure accordingly.

In this environment, income has done more of the work. Coupon matters when rates are not trending. Duration is best treated as a risk factor rather than a bet on macroeconomic changes. Credit selection remains critical, particularly when stable rates encourage incremental yield-seeking that can weaken portfolio liquidity.

What Would Change the Regime?

A sustained break in the 10‑year would likely require a regime change. On the upside, that could come from a durable reacceleration in nominal growth, a renewed inflation impulse that proves persistent, or a rise in term premium driven by supply, volatility, or reduced demand for long-duration assets. On the downside, it would likely take a clearer slowdown in labor markets and earnings, stronger evidence that inflation is structurally easing, or a cutting cycle aligned with weakening growth rather than simple policy normalization. Until then, the market appears comfortable trading within familiar boundaries.

Why This Matters Now

The last couple of years have been a good reminder that big daily moves can coexist with a stable multi-year range. The 10-year has been noisy, not directionally decisive. For investors, the discipline is to treat the 10-year as stable until proven otherwise, while respecting that stability can break quickly when a regime shifts. That argues for balanced exposure:

- enough duration to participate if growth slows and yields fall,

- not so much that a term premium shock dominates outcomes,

- and enough liquidity and credit quality to stay in control when volatility spikes.

The discipline is staying flexible enough to respond when the macro environment truly changes rather than reacting to every short‑term fluctuation along the way.