With the Justice Department dropping its investigation into the Fed’s building renovation, political uncertainty around the succession has faded, paving the way for Kevin Warsh’s nomination as the next Fed chair. Warsh’s recent remarks lay out how he views monetary policy and the implications for the bond market during his tenure.

While Warsh has been known as an inflation hawk, his stance on inflation and how he defines inflation is nuanced. On the one hand, Warsh has criticized the Fed’s post‑pandemic record, arguing that policymakers misjudged inflation in 2021 and 2022 and allowed price pressures to take hold. That experience has shaped his emphasis on institutional credibility and the need to keep inflation expectations anchored. A Fed chair with this outlook would be reluctant to declare “inflation under control” based on short stretches of favorable data, even as growth slows or political pressure mounts.

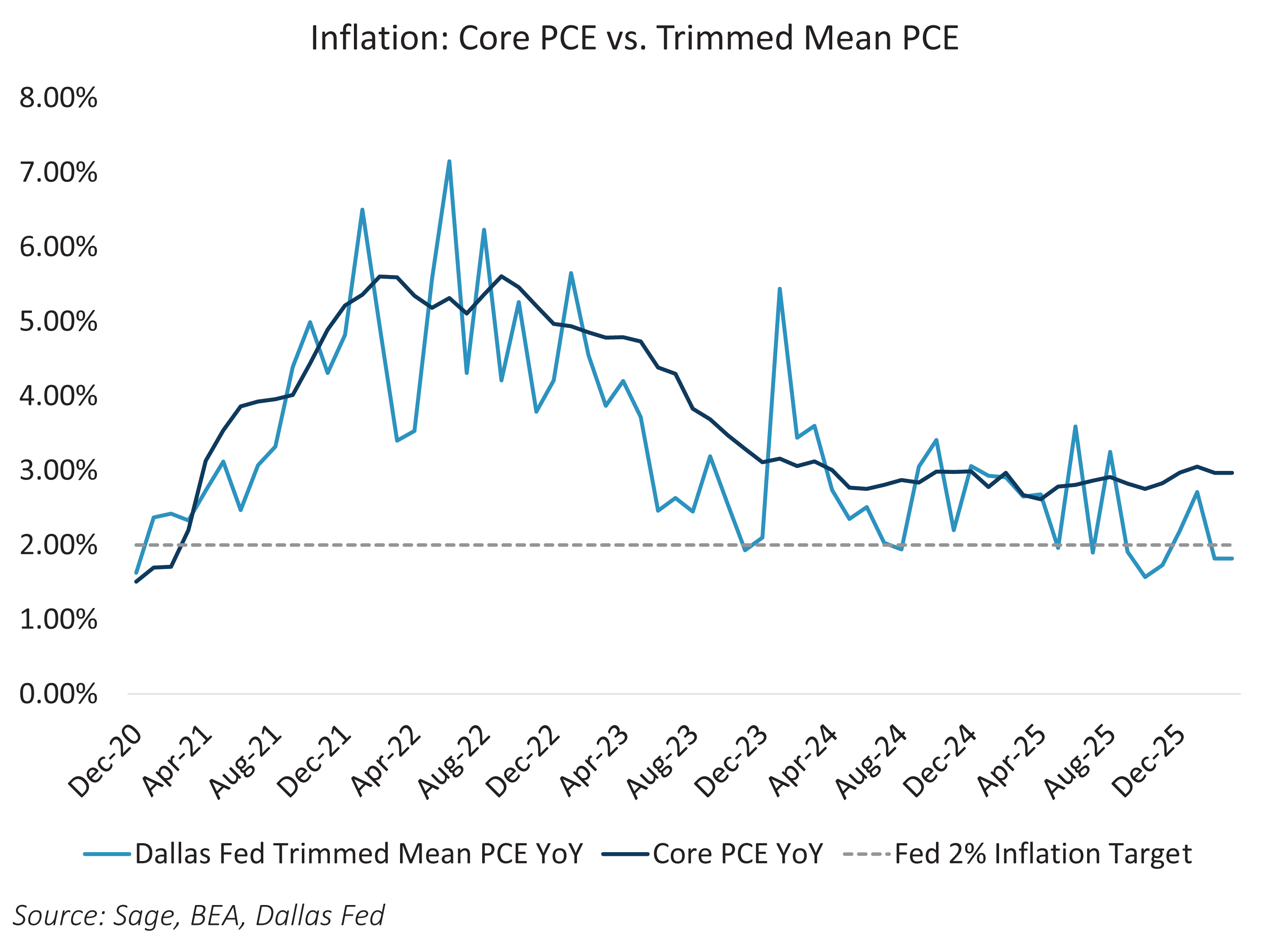

On the other hand, Warsh challenges how the Fed measures inflation. He is critical of relying on core PCE and instead points to trimmed mean and median measures that strip out extreme price moves. By those measures, inflation is currently lower than the headlines indicate and sits closer to target than headlines or core statistics suggest. Warsh has acknowledged this progress in his public remarks. Under his framework, the Fed can justify rate cuts while preserving its inflation mandate, grounding that case in the underlying trend rather than in volatile components.

Another important consideration for fixed income likely comes from balance sheet policy rather than from changes to the policy rate. Warsh opposes quantitative easing as a standing tool and argues that the Fed allowed crisis measures to become permanent. He links the expanded balance sheet to asset price distortion and to a weakened boundary between fiscal and monetary policy. His views point toward a central bank that reduces its footprint over time and reserves asset purchases for moments of systemic stress rather than routine cycle management. In this framework, Warsh could approach asset purchases with greater restraint, though how firmly he holds that line will become clear when the FOMC is tested by sustained market volatility.

Warsh may support lower short‑term rates if disinflation continues, but he shows little appetite for suppressing long‑term yields through asset purchases or heavy communication. He questions forward guidance and argues that policymakers should make decisions at meetings instead of pre‑committing to forecast paths. That stance places more of the burden of duration pricing back on markets and could create more frequent and meaningful dislocations in fixed income, offering opportunities for active bond managers.