Last year, following the election of New York City Mayor Zohran Mamdani, we noted that many key elements of his agenda would be extremely difficult to implement given the mayor’s limited ability to enact major unilateral policy changes. Most notably, the administration has been unable to deliver on its pledge to eliminate bus fares citywide, an objective we do not expect to be realized absent major structural funding reforms.

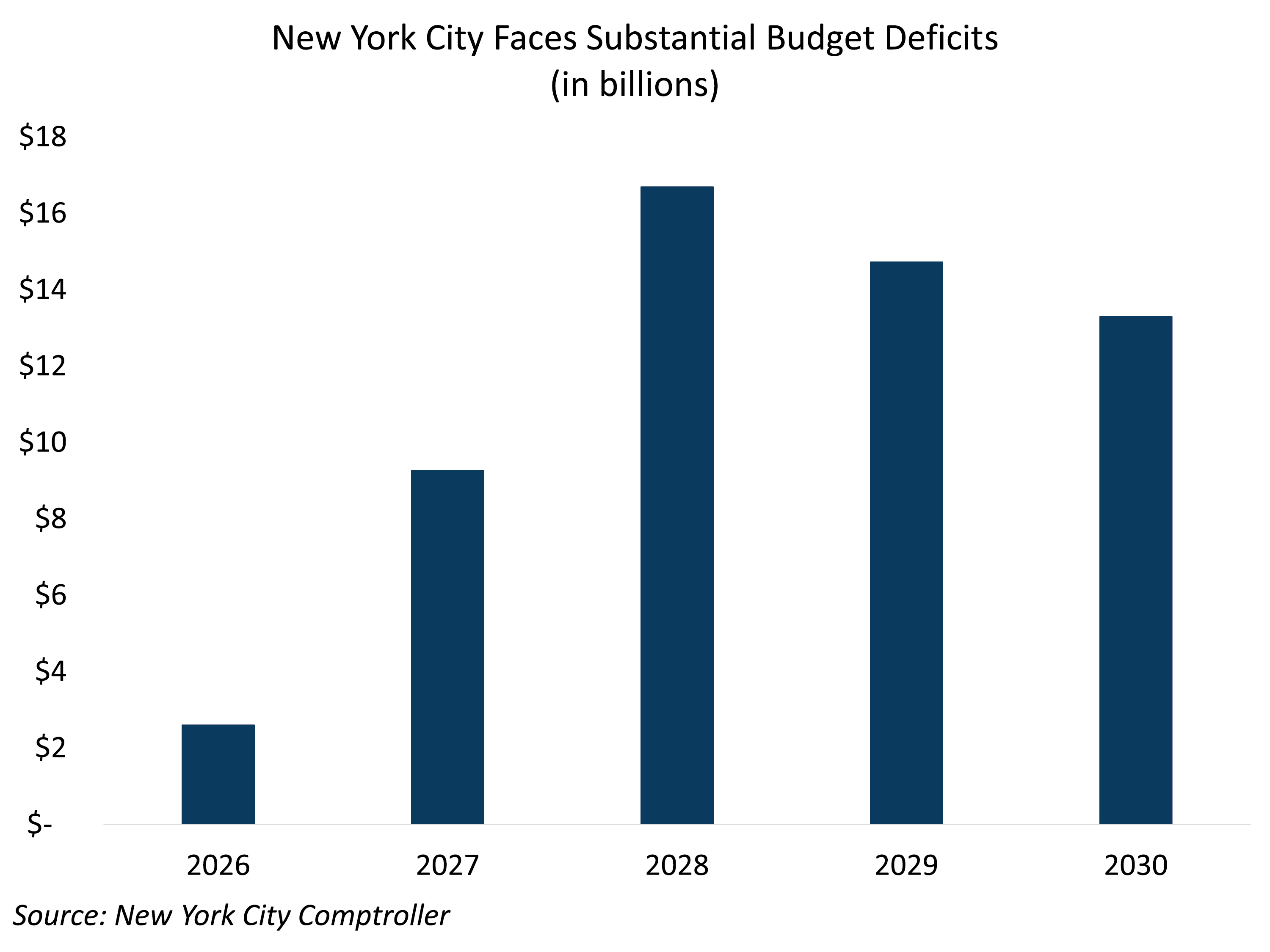

At the same time, the city is grappling with a budget deficit exceeding $2 billion in fiscal year 2026, alongside a projected $10.4 billion gap in fiscal year 2027. While these shortfalls reflect years of fiscal mismanagement under the prior administration, Mayor Mamdani now bears responsibility for stabilizing the city’s finances while advancing a policy agenda that, in many cases, would further strain the budget.

Rather than pursuing meaningful expenditure reductions, the mayor has proposed a series of revenue‑raising measures through tax increases, most of which have gained little traction. This is unsurprising given that, when state and city taxes are considered together, New York City residents face the highest marginal income tax burden in the nation. Despite this heavy burden on taxpayers, the city’s more than $120 billion operating budget continues to balloon, consistently outpacing the rate of inflation. Rather than focusing on ways to rein in recurring expenditures, the mayor has instead shifted his attention to the city’s pension system as a potential source of near‑term budgetary relief.

Proposed Pension Contribution Holiday Would Materially Weaken the City’s Credit Profile

To address the budget gap, Mayor Mamdani has floated a proposal to reduce annual pension contributions by approximately $1 billion through actuarial changes that would extend the timeline for fully funding pension obligations. We view this proposal as a significant credit negative, as it would defer costs to future budgets and heighten the long-term fiscal impact of weaker-than-expected investment returns.

In many respects, pension obligations function similarly to debt: they are long-term liabilities that require consistent funding to ensure timely payments to beneficiaries. A willingness to reduce annual pension contributions therefore raises broader concerns about the city’s commitment and capacity to meet its fixed obligations, particularly in the absence of a credible plan to address large, structural budget deficits. This approach is likely to draw heightened scrutiny from both rating agencies and investors, as a reduction in pension contributions of this magnitude would materially increase downside credit risk and could lead to ratings pressure and wider borrowing spreads.

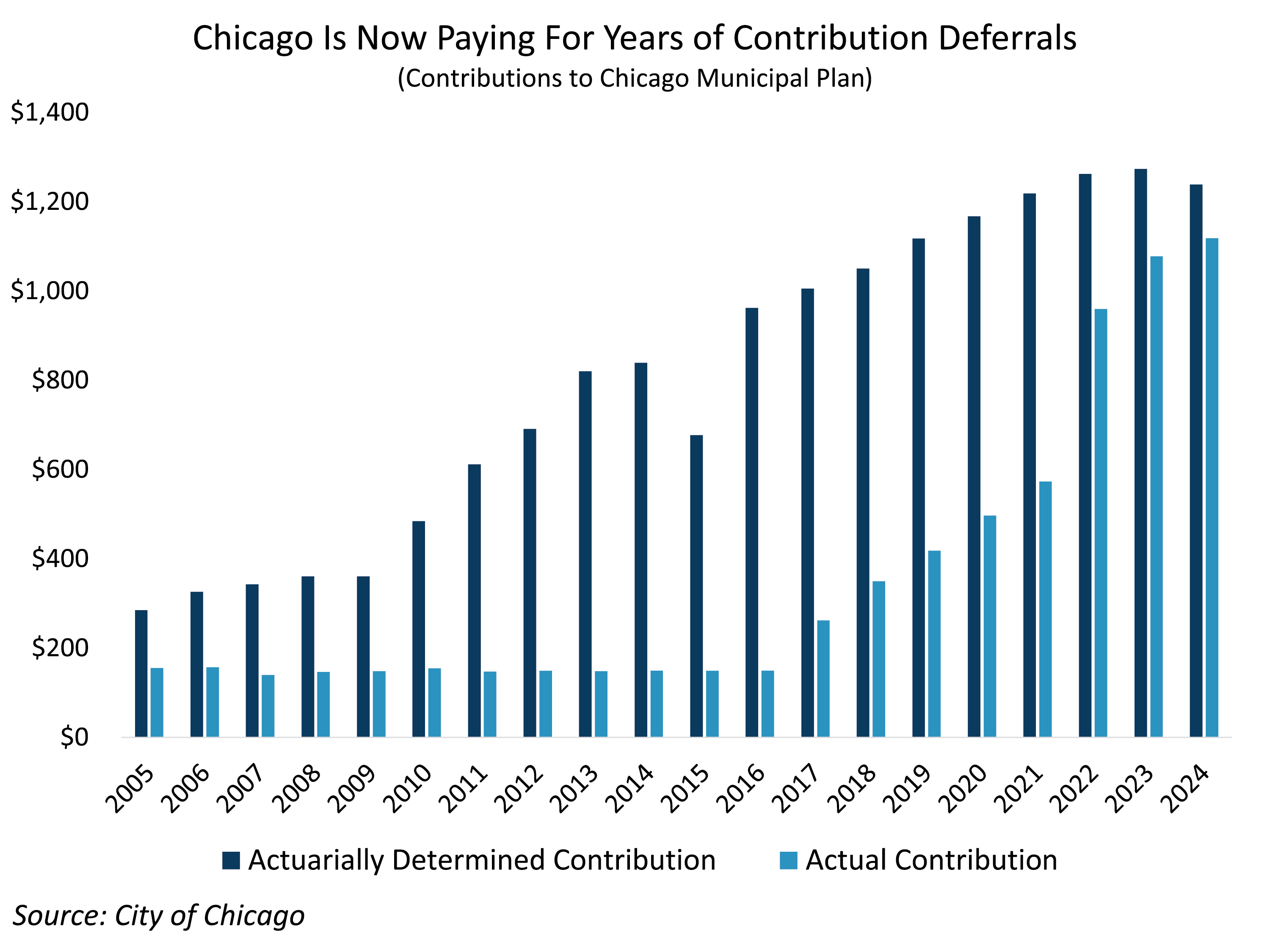

Pension Contribution Reductions Have Been Tried Before With Costly Results

New York City would not be the first municipality to seek budgetary relief by underfunding its pension systems. Most notably, the City of Chicago deferred pension contributions for years, only to see required payments surge following poor investment performance during the Global Financial Crisis. As a result, Chicago now spends roughly $1 billion more annually on pension contributions than it likely would have had it consistently made full payments in prior decades.

While Mayor Mamdani’s proposal relies on actuarial adjustments rather than outright contribution deferrals, the underlying premise remains the same: contributing less today increases the likelihood of substantially higher costs in the future. Although the mayor has consistently framed his agenda as serving the interests of everyday New Yorkers, this approach appears at odds with that objective by shifting fiscal risk onto future taxpayers.