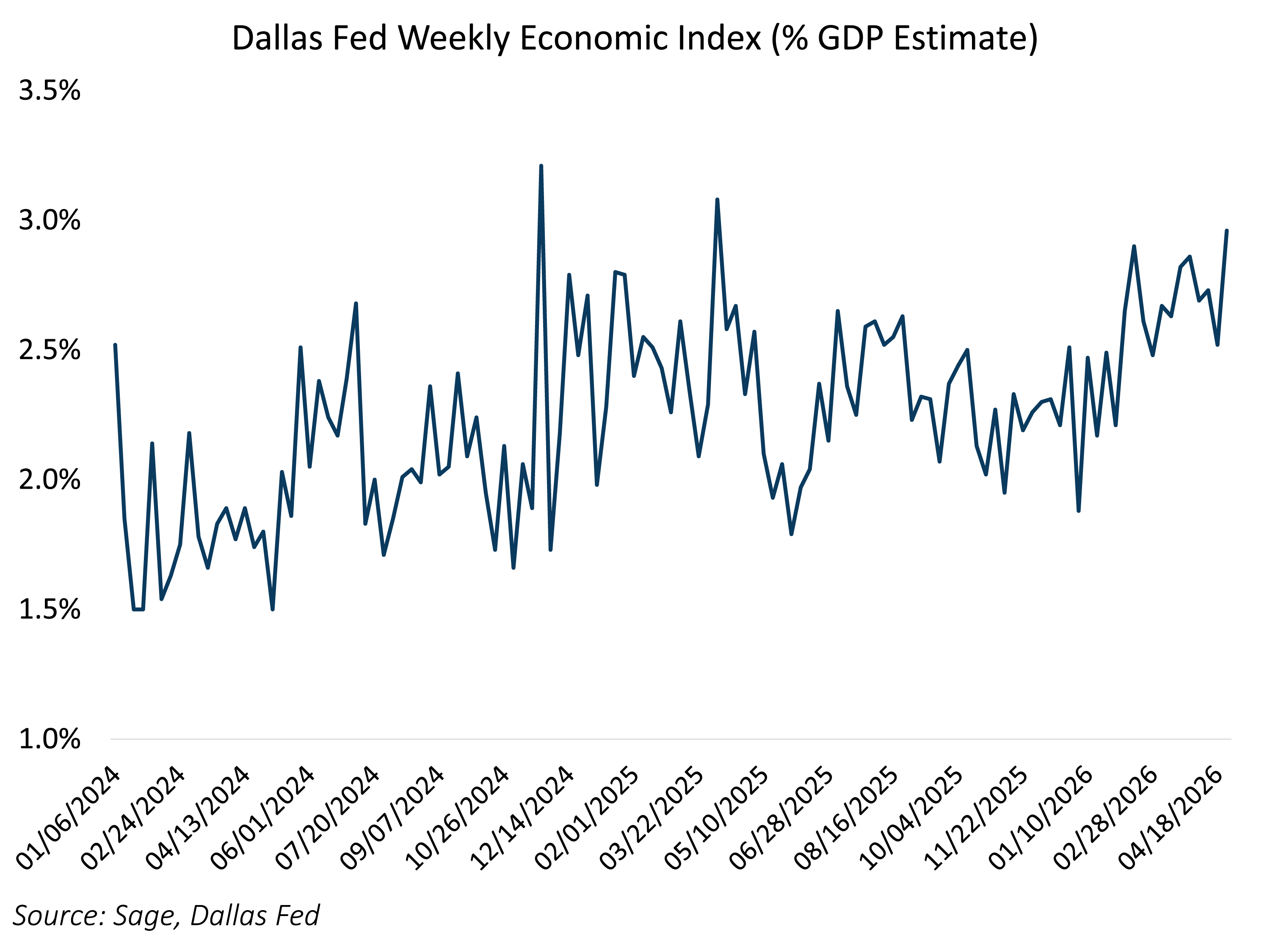

Market narratives remain split between two forces: tail risk to oil flows through the Strait of Hormuz and constructive US economic data supported by AI infrastructure capex. The Dallas Fed Weekly Economic Index (WEI), a real-time, GDP-equivalent signal of economic momentum, rose to 3.0% from 2.5% last week.

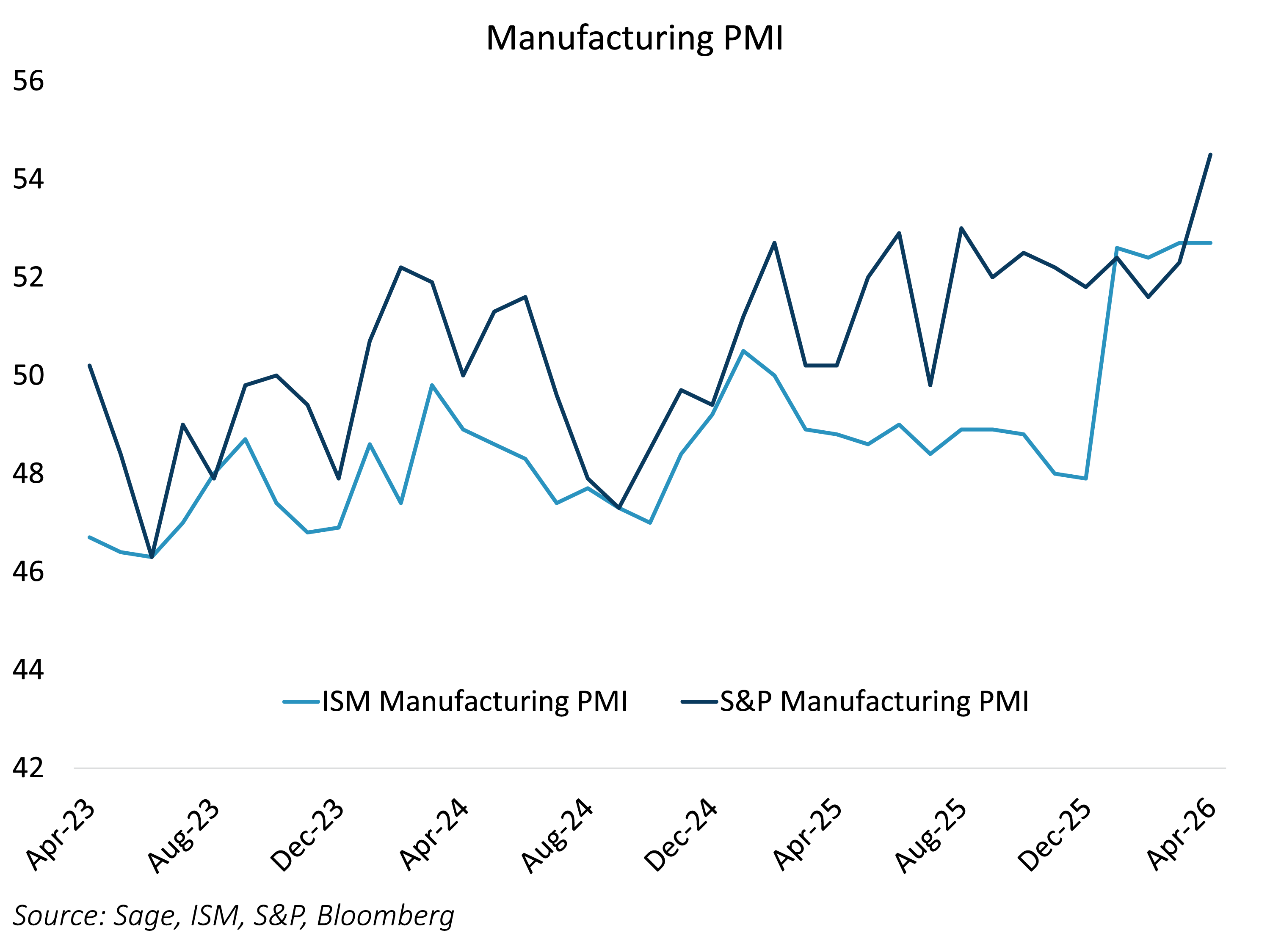

Manufacturing PMI surveys also signaled a continued manufacturing renaissance from AI infrastructure spending and reshoring, which could continue to boost both economic growth and productivity.

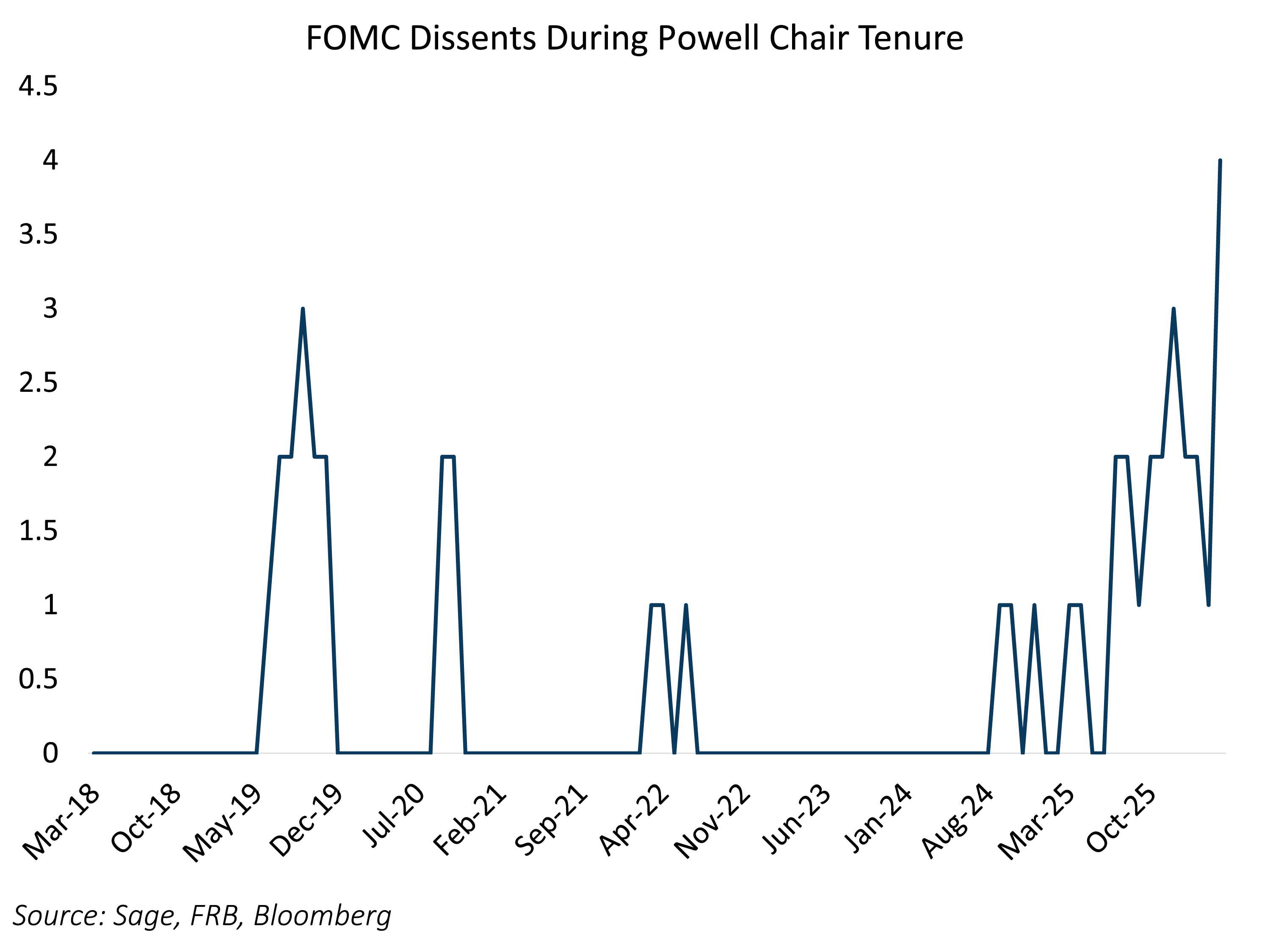

Stronger data, however, can bring its own risk. With energy-driven inflation pressure still a meaningful wildcard amid the Iran conflict, global central banks face a familiar dilemma. For the FOMC, that tension is heightened as the Fed navigates a leadership transition alongside a still-solid expansion.

When Powell took the helm as chair in early 2018, the Fed was in the midst of rate hikes after years of extraordinary accommodation, with inflation subdued and consensus-driven decision-making the norm. Today, inflation risks are more prominent and fiscal policy plays a larger role, with no end in sight to the fiscal deficit. Now, the Fed must contend with maintaining a solid economic expansion while mitigating inflation pressures. Interest rates should continue to remain rangebound at these levels as the Fed navigates competing objectives with less consensus than in past cycles.