Recent inflation data is sending two distinct signals. Headline CPI has moved higher as energy prices surged following the escalation of the Iran conflict, pulling inflation measures upward in a visible way. At the same time, core inflation, which strips out volatile food and energy components, has remained comparatively steady. That divergence is central to understanding both market pricing and the Federal Reserve’s policy path.

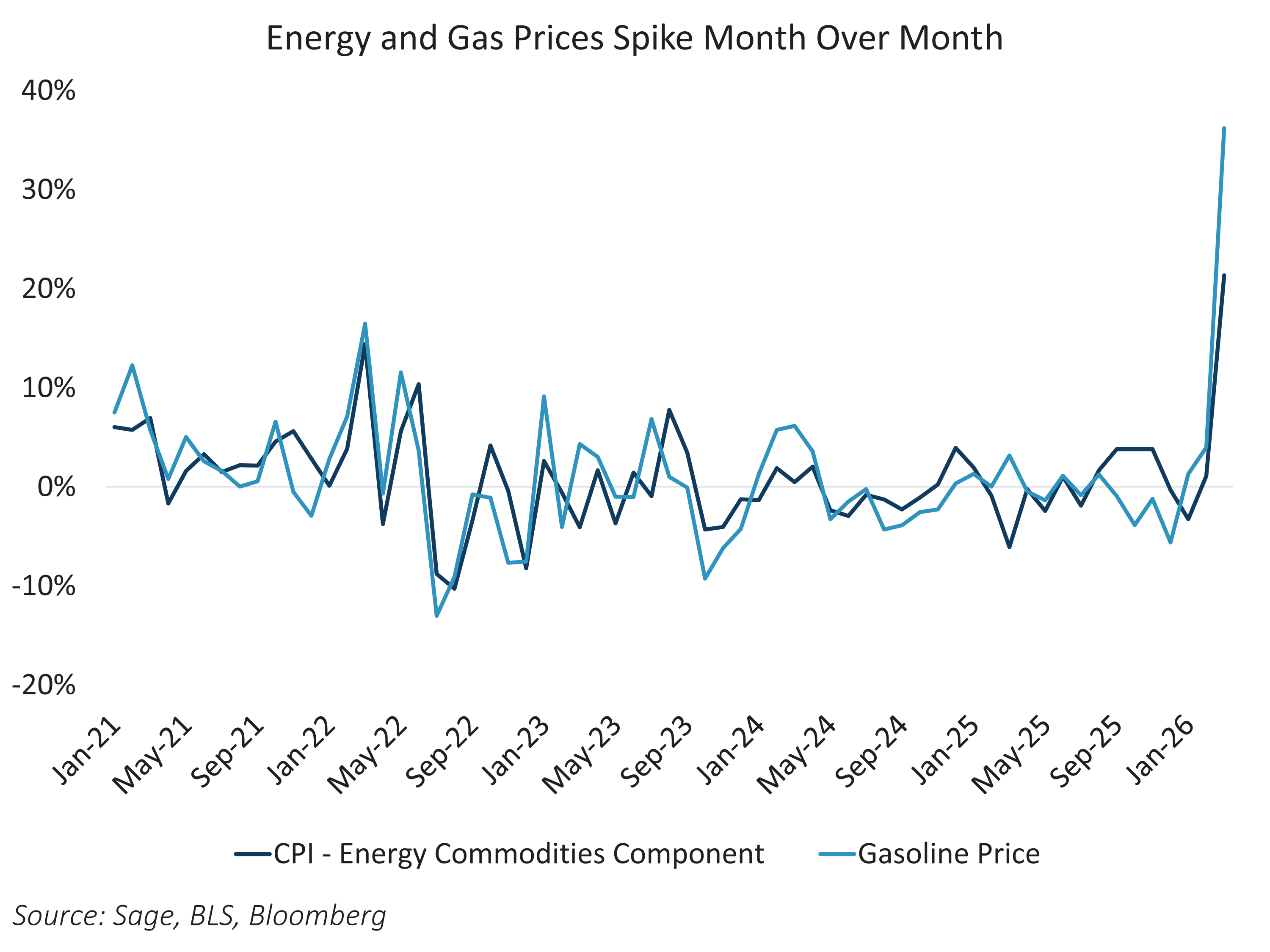

The March CPI print reflected the oil shock tied to the Iran war and showed a sharp move in commodity goods prices, up 21% on the month. That increase tracks the jump in national average gasoline prices, which rose 36% over the same period. The Iran war is having a clear impact, concentrated in commodity-linked areas of inflation.

The current energy shock is larger than the one that followed the Russia-Ukraine invasion in March 2022. At that time, the CPI energy component rose 14% and gasoline prices increased 16%. Today’s increases exceed those levels by a wide margin.

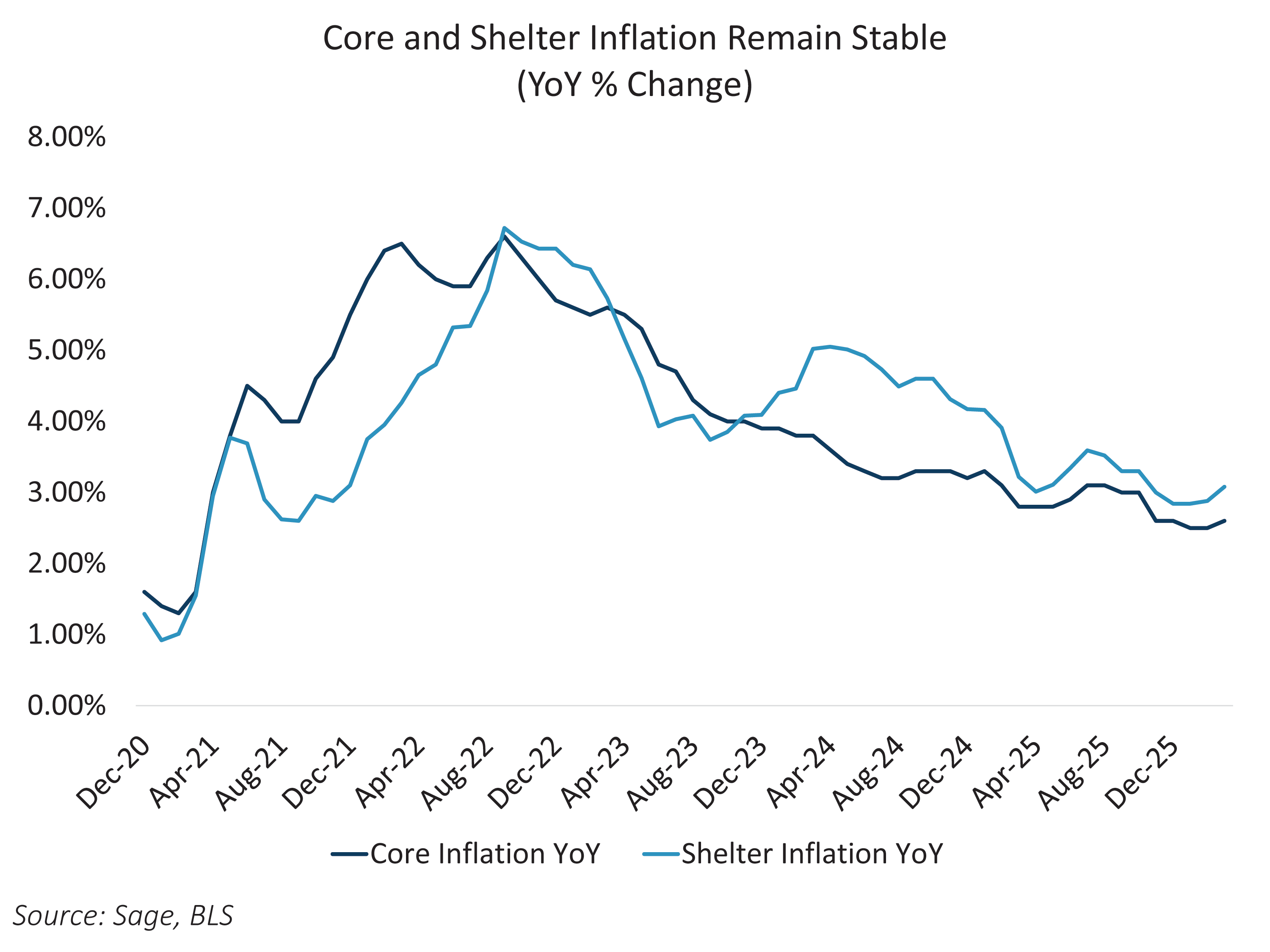

Broader inflation measures remain more stable. Core CPI, which the Fed emphasizes, came in at 2.6% year over year in March 2026. Shelter inflation, the largest component, came in at 3.08%. During the 2022 spike due to the Russia/Ukraine war, shelter inflation ran at 4.26% and core CPI stood at 6.5%, reflecting a far more inflationary backdrop than what we see today.

The current energy shock is pushing headline inflation higher, but underlying conditions remain healthier than they were in early 2022. That episode followed a supply shock tied to Covid-era disruptions, while this time, inflation had been moderating before the energy spike began. A sustained and broad rise in core prices beyond energy would be required to put rate hikes back on the table. Markets are now pricing in a prolonged policy pause over the next two years, a notable shift from earlier expectations for rate cuts. While the bar for rate cuts remains high, the policy path remains fluid and dependent on how conditions in the Strait of Hormuz evolve.