Oil prices have remained elevated due to the closure of the Strait of Hormuz and the risk of further damage to oil infrastructure. Inflation expectations, as reflected in TIPS breakeven inflation, have increased at the front end of the curve, while longer-term inflation expectations remain stable.

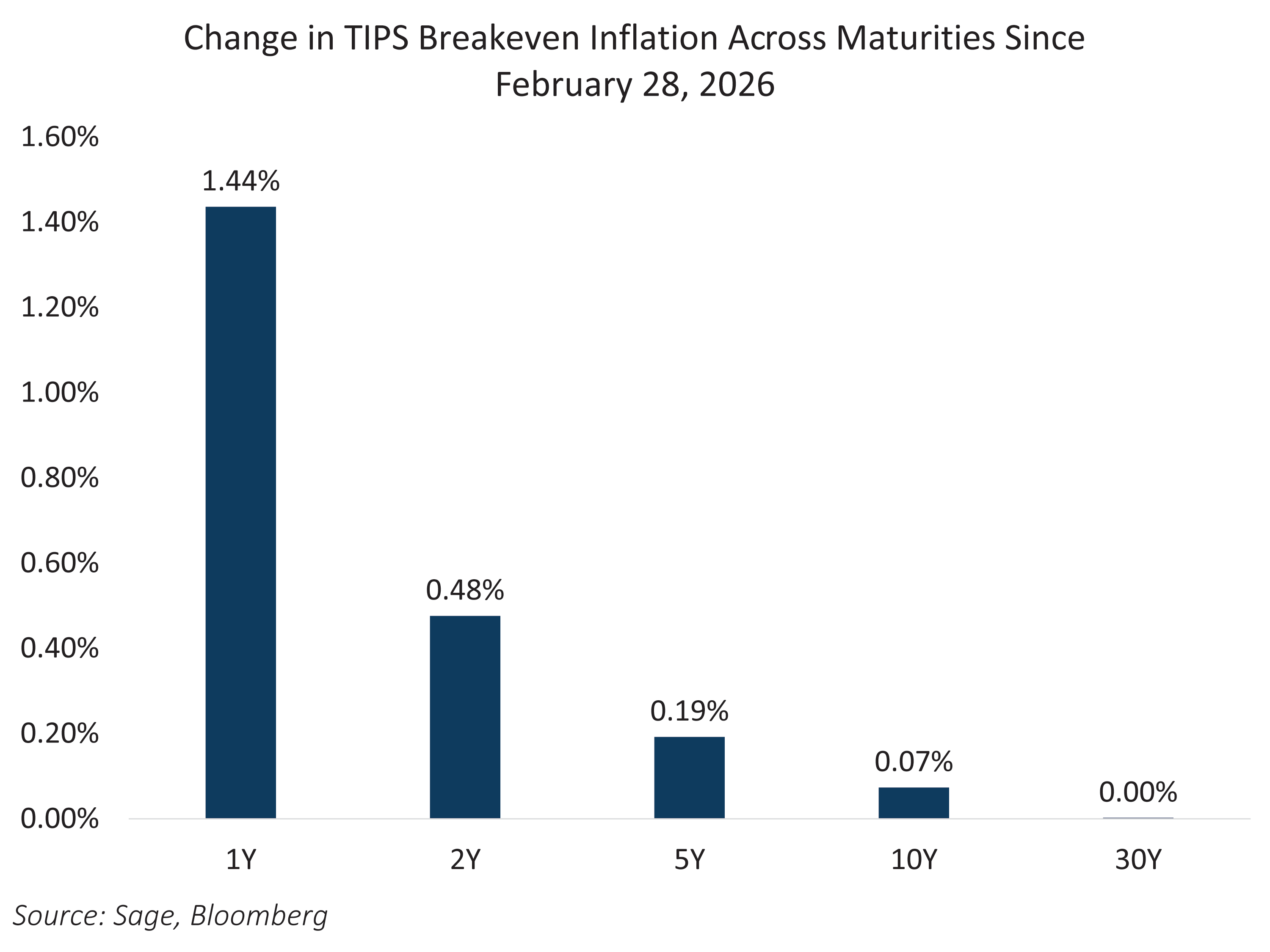

Breakeven inflation, the difference between the yield on a nominal Treasury and a TIPS of the same maturity, represents the inflation rate at which an investor would be indifferent between holding the two securities over that horizon. Rising breakevens therefore indicate higher inflation expectations. As shown in the chart below, changes in breakeven inflation since February 28 have been concentrated in the front end, with little change in longer-term expectations.

Short‑dated breakevens reflect near‑term inflation risks driven by energy prices and potential supply disruptions. Longer‑dated breakevens, by contrast, capture market views on whether those shocks persist and translate into broader, structural inflation pressures. The limited response at the long end suggests markets currently view the oil shock as a temporary inflation impulse rather than a lasting shift in long‑run inflation expectations. While market pricing presents a risk of higher oil prices and further escalation resulting in an unanchoring of longer-term inflation expectations, a mitigation in hostilities could see inflation pricing and rates fall in short order.