US interest rates continued to break higher, moving beyond the tight range that held in place following the onset of the war. Economic data remain resilient, with growth readings holding firm despite the energy shock, while last week’s inflation prints showed incremental acceleration. With little progress on negotiations to reopen the Strait of Hormuz, markets are increasingly pricing in a more persistent inflation path. At the same time, newly confirmed Fed Chair Kevin Warsh heads into his first FOMC meeting facing a more complicated backdrop, balancing firming inflation data against his previously more accommodative tone.

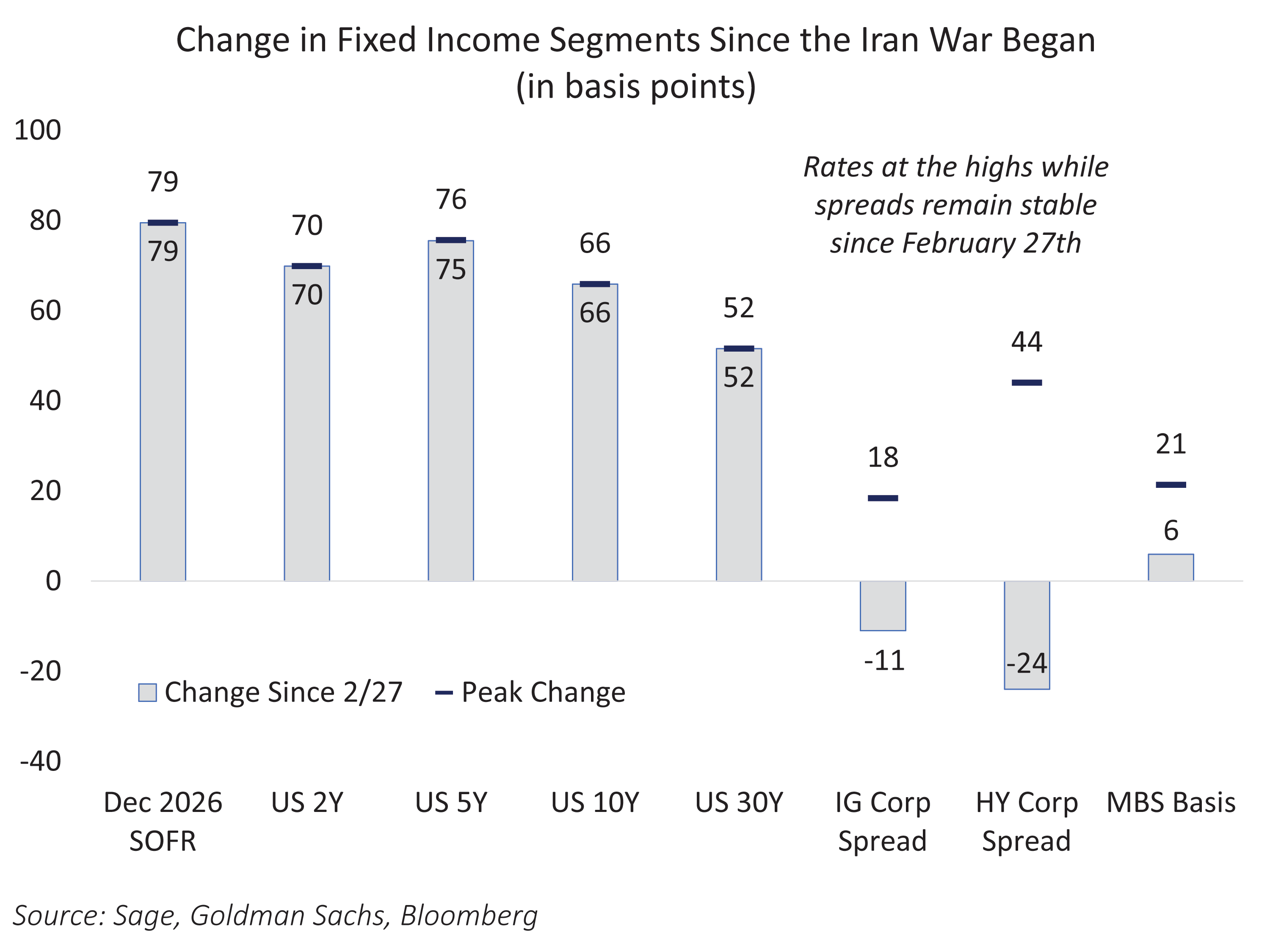

This dynamic marks a notable shift from earlier expectations. In an earlier note “There and Back Again,” we highlighted the sharp moves in global fixed income and the reversal that followed the Iran ceasefire announcement. One month later, progress on reopening the Strait remains limited. As a result, that reversal has largely unwound: rates have retraced higher and now sit at their highest levels since the war began. Meanwhile, credit spreads continue to reflect resilient economic and corporate fundamentals, remaining near the tightest levels seen this year.

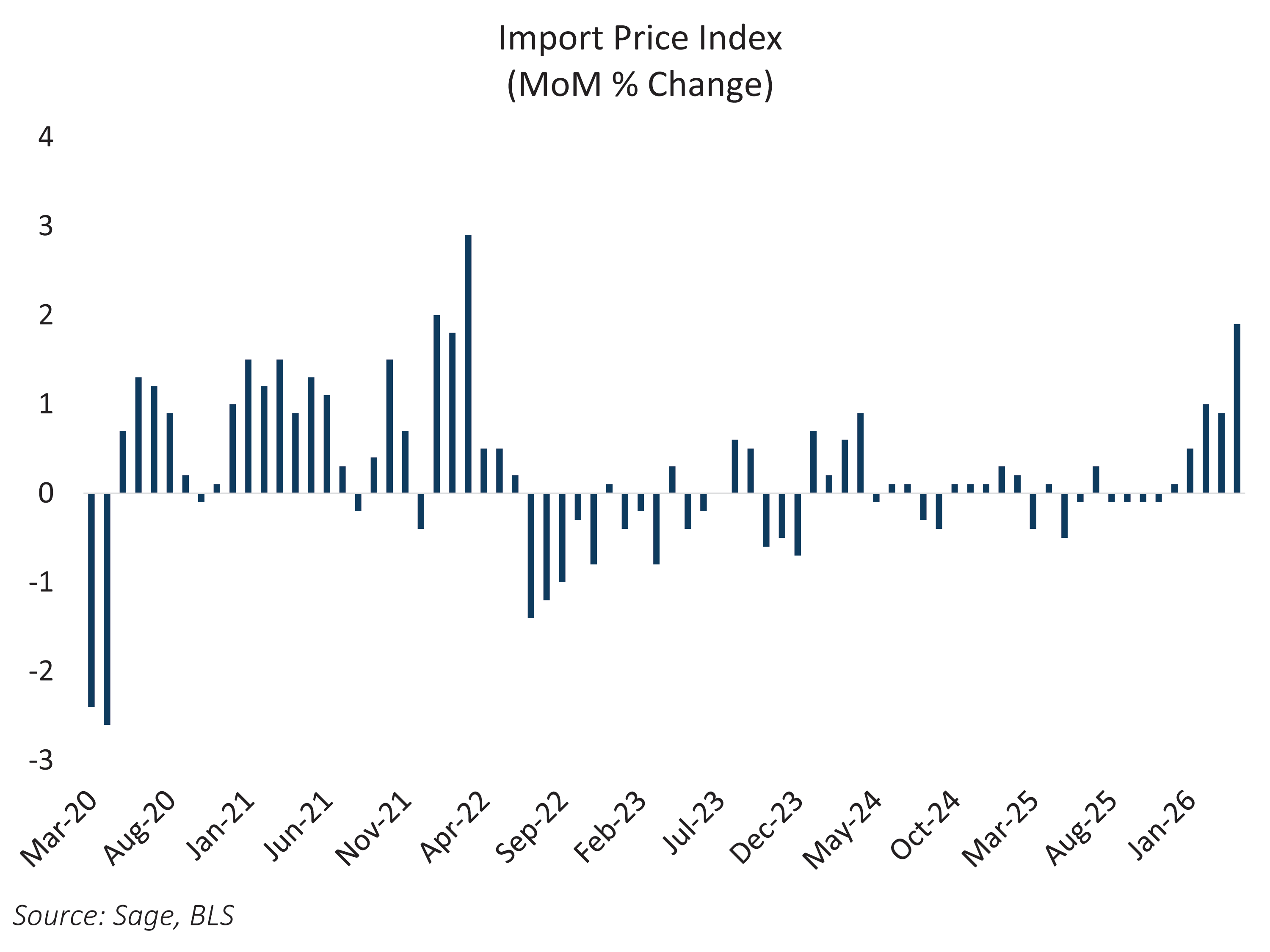

Recent data have only reinforced these trends. Last week’s releases, particularly on inflation, highlight the growing risks associated with a prolonged stalemate that keeps the Strait closed. Import prices, for example, rose at their fastest monthly pace in four years, underscoring the renewed upward pressure on costs.

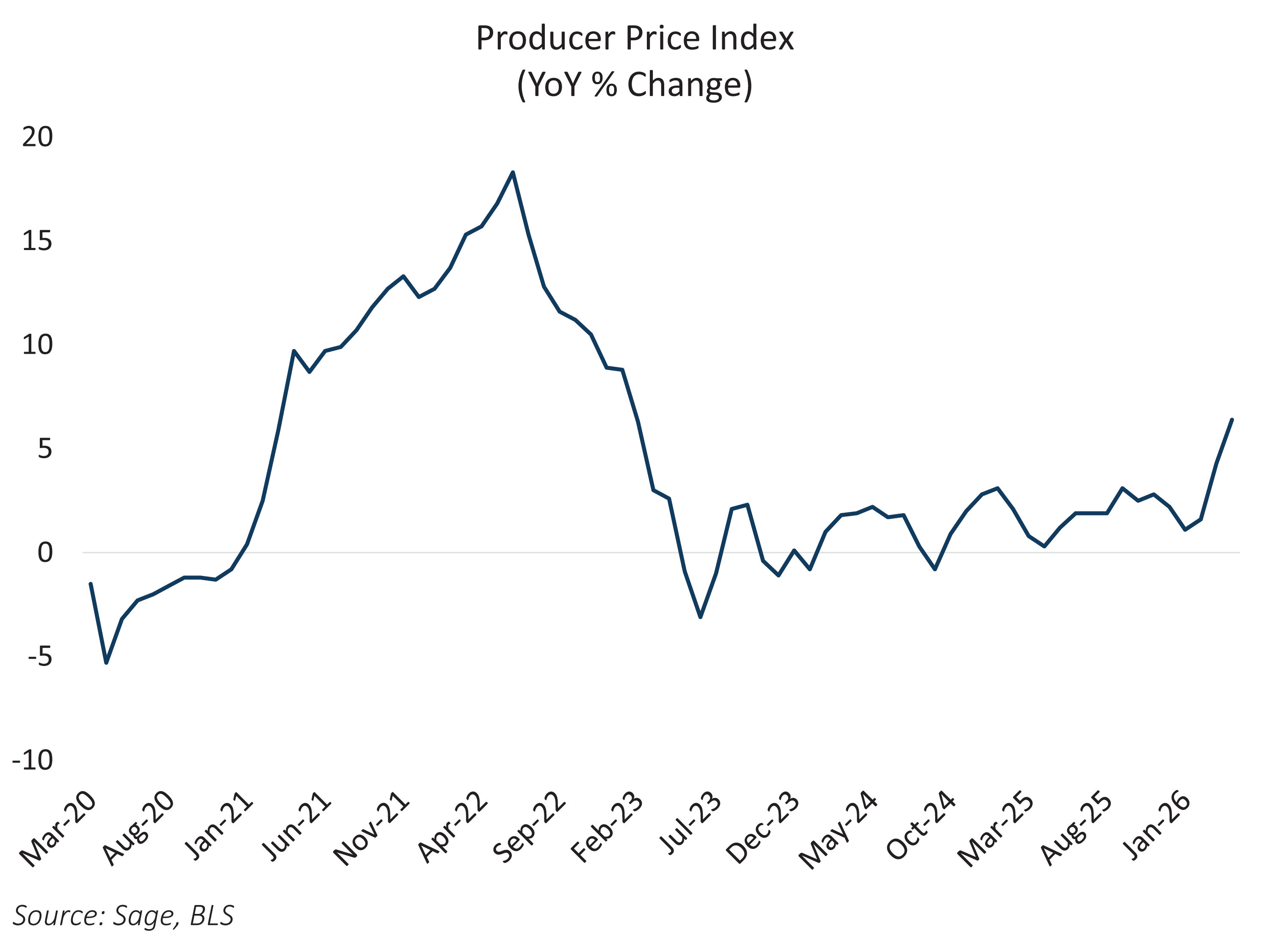

Similarly, producer prices continue to trend higher. The Producer Price Index (PPI) also ticked higher as expected, and is now running at 6.4% year-over-year, well above the range that persisted through much of 2023.

Taken together, these developments set the stage for a challenging start to Chair Warsh’s tenure. He inherits a divided committee and must navigate clear inflation pressures and the need to maintain credibility on both sides of the Fed’s mandate. Markets are now pricing roughly one rate hike by March 2027, and we expect the Fed’s median dot plot to align closely with that path, placing added focus on how Warsh communicates this shift. First FOMC meetings often test a new chair and can drive elevated volatility, and June is unlikely to be an exception.