The surge in hyperscaler-related borrowing to fund AI infrastructure has found its way into the municipal market. Last week, Alphabet borrowed approximately $1.2 billion through a tax-exempt prepaid energy bond, with the deal drawing more than $10 billion in orders. These structures involve a municipal issuer issuing tax-exempt debt to prepay for a long-term energy supply, with the proceeds flowing to the corporate backer, allowing them to access below-market funding compared to traditional corporate debt.

As we have written previously, prepaid energy bonds have been one of the hottest segments of the muni market over the past several years, as corporate borrowers look to capitalize on the attractive differential between taxable and tax-exempt rates. Issuance, however, has largely been concentrated among high-quality banks and insurance companies. Alphabet’s entrance into the prepaid market provides meaningful issuer and sector diversification for investors, though we believe it introduces incremental risks that are not being fully priced in.

The Prepaid Energy Sector Remains Highly Concentrated

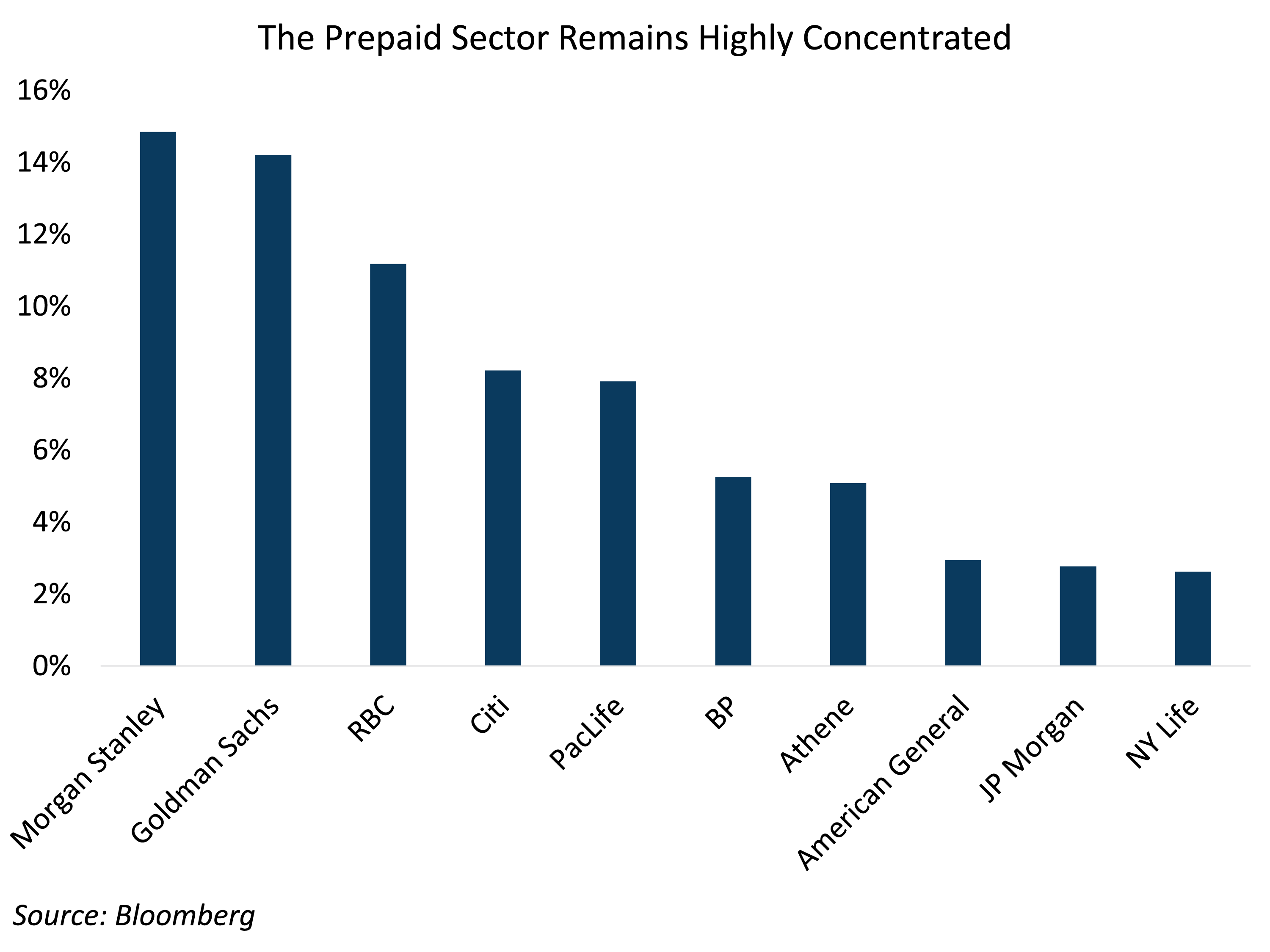

Despite strong demand, signs of fatigue are beginning to emerge in the prepaid sector. A small group of banks and insurance companies continues to dominate issuance, with the top five guarantors accounting for nearly 60% of the approximately $120 billion market. Investors have been increasingly focused on the lack of diversification in the asset class, which only amplified demand for Alphabet’s inaugural deal.

Alphabet’s Inaugural Prepaid Energy Bond Likely A ‘Proof of Concept’ Test

Alphabet’s decision to raise $1.2 billion in the municipal market is somewhat perplexing in the broader context of its capital structure. The company has already raised approximately $52 billion in corporate debt this year and is in the process of completing an $85 billion equity raise. Against that backdrop, the complexity associated with executing a prepaid energy bond likely outweighs the economic benefit.

While these structures provide access to tax-exempt funding for taxable entities, the corporate backer must importantly share the resulting interest savings with the utility counterparty, limiting the economic benefit. Based on our estimates, the roughly $1 billion raised in this structure likely generates only a few million dollars in annual savings for Alphabet, a relatively immaterial amount for them.

This leads us to believe that this issuance was simply a ‘proof of concept’ exercise to assess investor demand and execution feasibility. For the structure to become meaningful, Alphabet would need to scale issuance materially, allowing aggregate interest savings to reach a level that justifies the added complexity.

Investors Are Underpricing the Risk That Significant Additional Debt Could Be on the Horizon

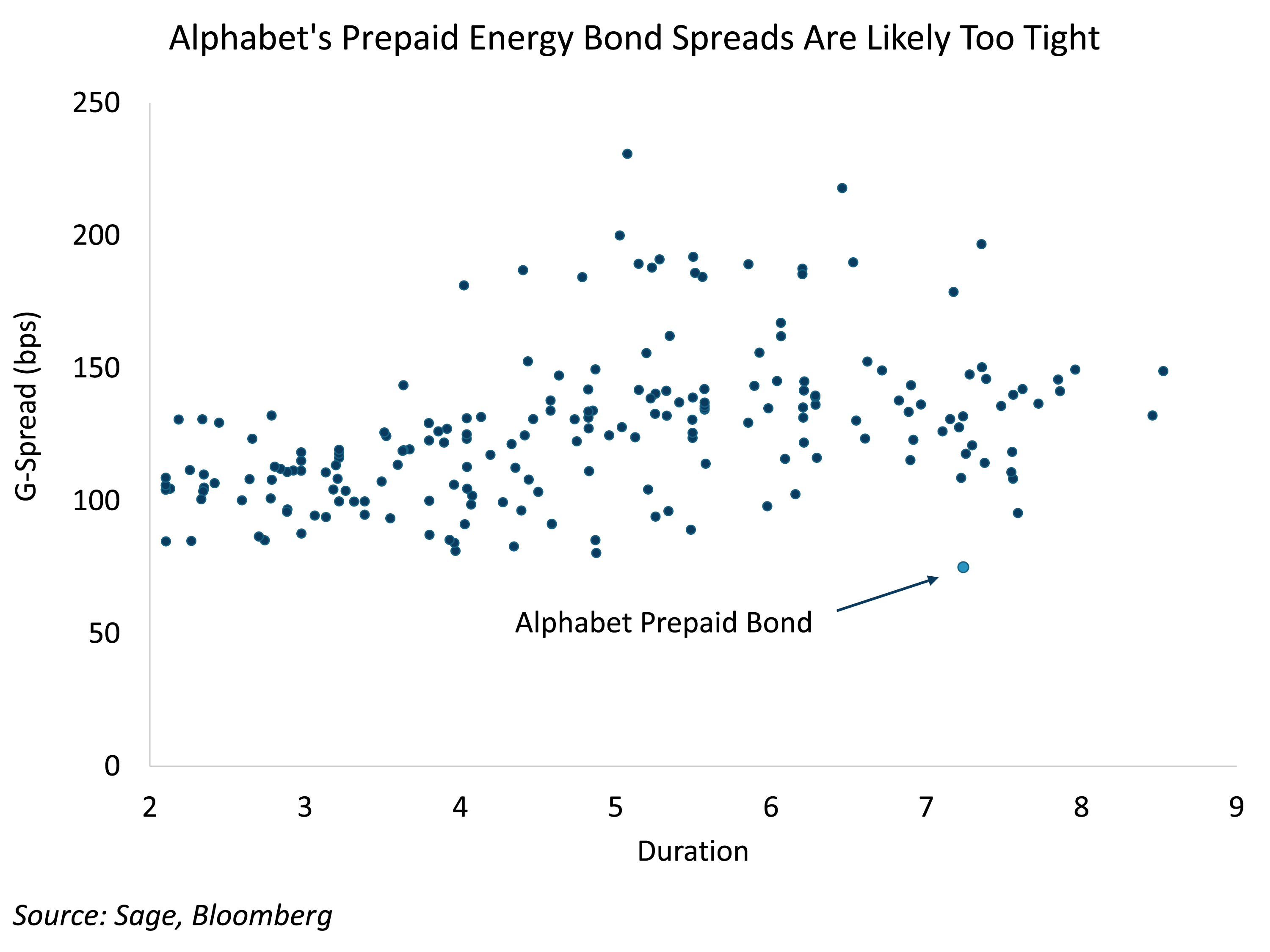

A more pressing concern is how the market is valuing this new entrant. Alphabet’s prepaid bonds are currently trading around 75 basis points above the AAA municipal curve, roughly 50 basis points tighter than comparable prepaid structures. We believe these levels overcompensate investors for diversification benefits while undercompensating them for the risk that this transaction represents the first step toward a significantly larger borrowing program. If that scenario materializes, spreads on Alphabet-backed prepaid bonds could widen by 25 to 50 basis points, creating meaningful downside for investors at current valuations. Thus, we intend to underweight our exposure to Alphabet in the prepaid sector until more clarity emerges regarding the company’s future borrowing plans.