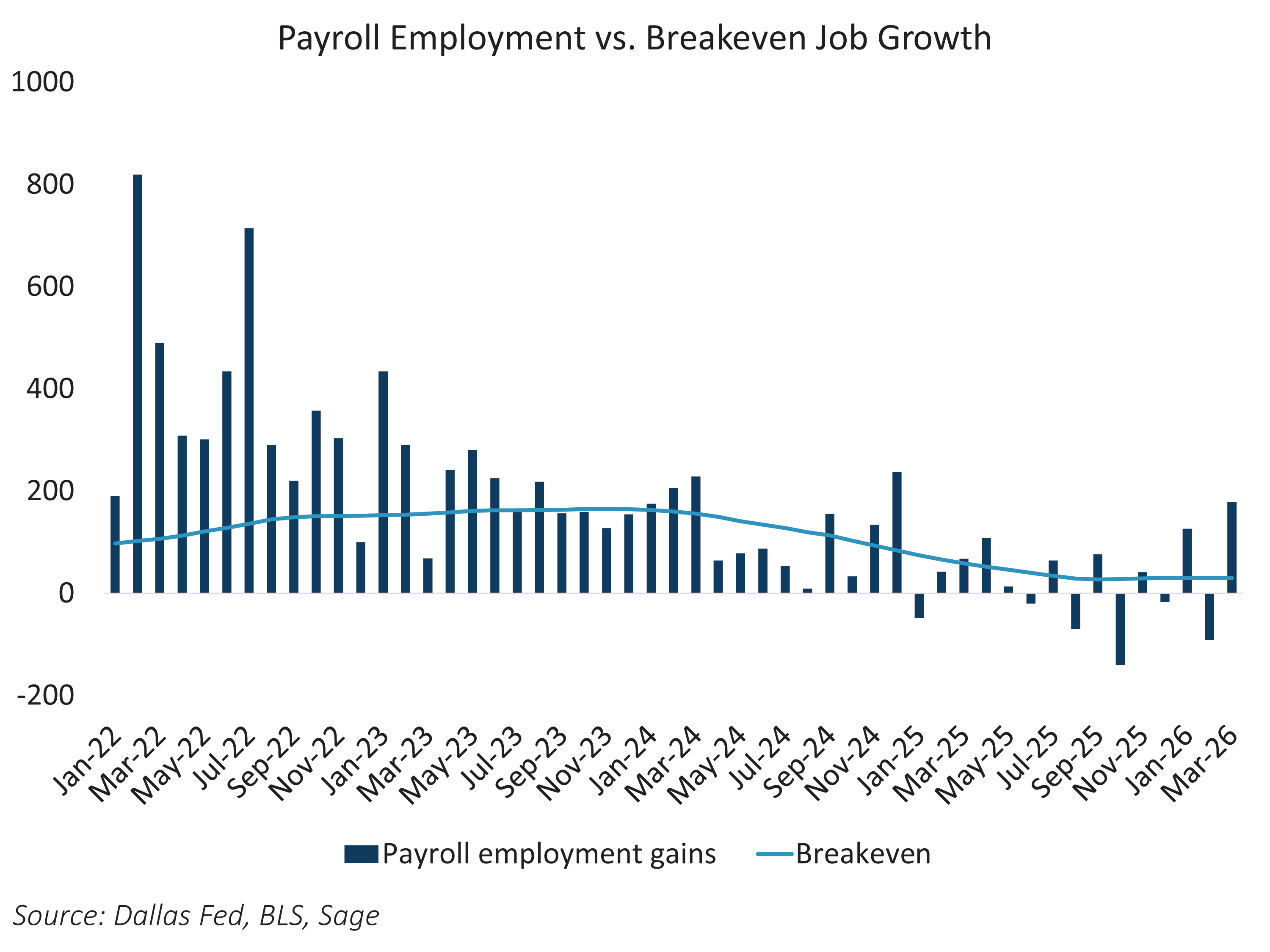

March payrolls beat expectations, rising by 178k, but the headline strength masks a labor market with limited slack and waning momentum. Downward revisions to February (-41k), only partially offset by an upward January revision (+34k), pull three‑month average job growth down to just 68k — barely above estimates of breakeven. The labor market is still expanding, but only marginally.

The unemployment rate fell to 4.26%, though the decline reflects a shrinking labor force rather than stronger hiring. Labor force participation dropped by 396k in March and is down roughly 1.4 million so far this year. When participation falls, unemployment can decline even as labor demand cools. A lower unemployment rate driven by falling participation points to stagnation, not renewed strength.

According to the Dallas Fed, breakeven job growth now sits near 30k per month. Payroll gains remain above that threshold, suggesting little outright slack. The buffer, however, is extremely thin. Unlike 2022, when breakeven growth exceeded 160k and allowed hiring to slow without lifting unemployment, today’s labor market offers little room to absorb further weakening.

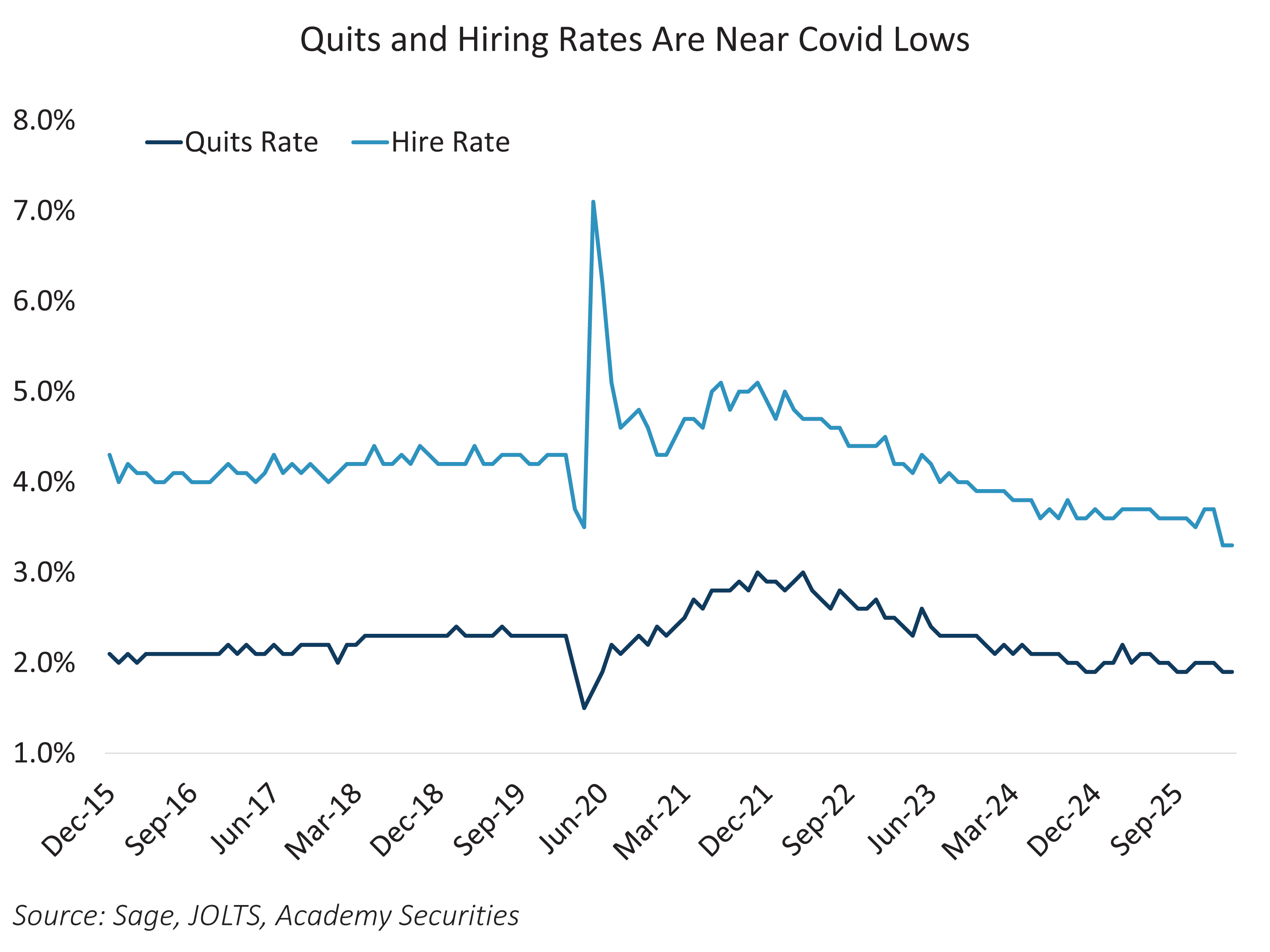

JOLTS data reinforce this picture. Hiring and quit rates continue to drift lower, signaling caution on the part of employers and reduced confidence among workers. Job mobility has slowed, churn has declined, and labor market behavior on both sides has become more defensive.

This fragility matters in the current macro environment. Rising fuel costs and concerns around supply disruption have dominated markets in recent months. With limited labor slack, slower hiring and falling participation constrain households’ ability to absorb higher costs. At the same time, subdued hiring and quits are easing wage pressure, helping to contain second‑round inflation risks.

We continue to view the economy as operating within a higher productivity growth regime, supported by AI‑related investment and expanded domestic production. Higher productivity can help sustain growth even as labor supply tightens. That support is not guaranteed. If productivity gains arrive more slowly than expected, or if energy prices outpace income growth, the labor market could contract more quickly than headline indicators suggest.