After an eventful few months, the summer begins with a few important waypoints for economic data. Economic readings, particularly labor market data and inflation, have outperformed expectations. In the context of rising energy prices and their effect on inflation, FOMC Chair Warsh’s June 16-17 meeting will see him walk a tightrope around acknowledging inflation pressures while not committing to a rate action one way or the other.

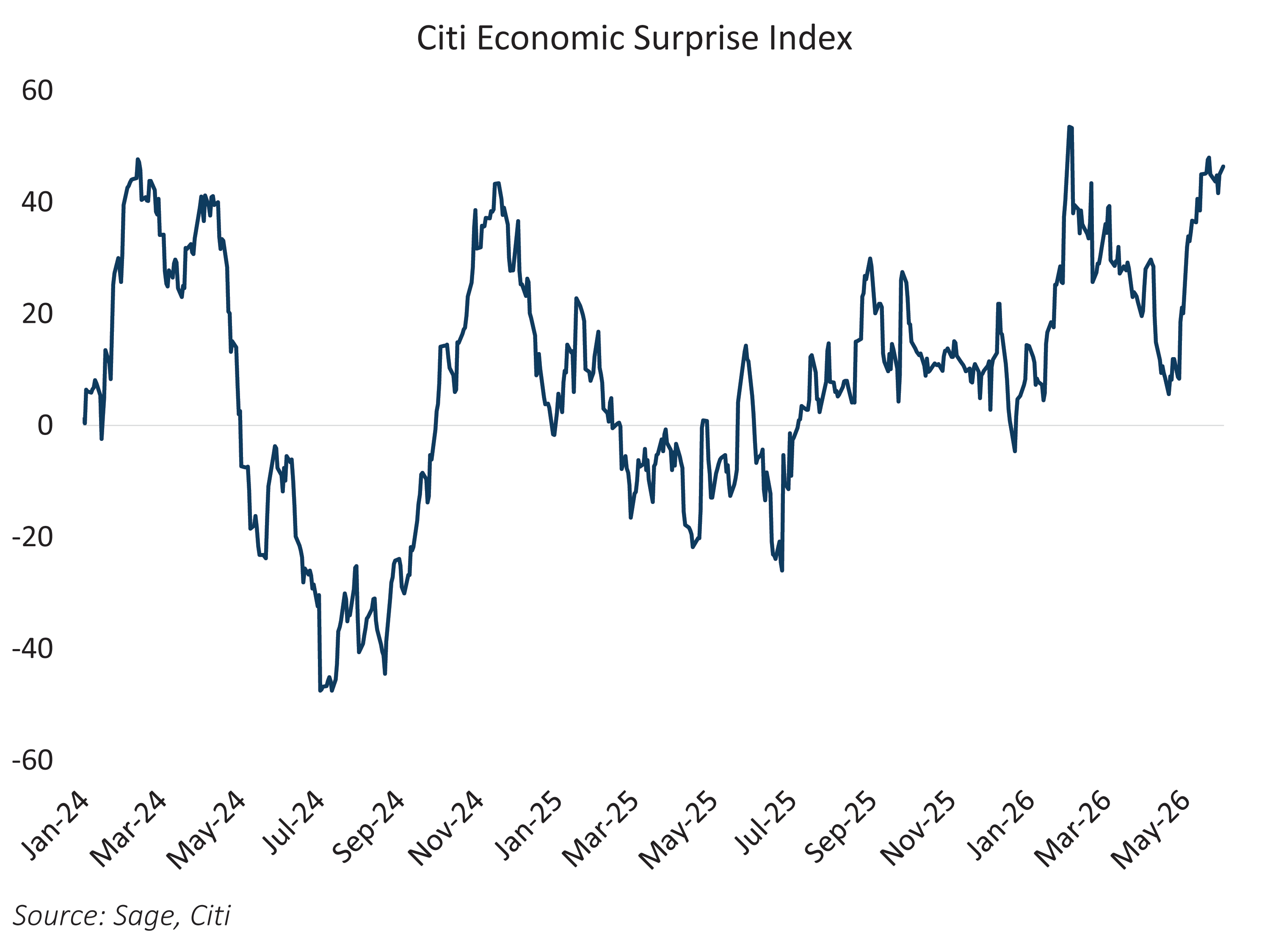

In the US, the economic picture continues to improve. The Citi Economic Surprise Index sits at 41.6 as of late May, near YTD highs and part of what has been a positive streak stretching back over a year — the longest run of upside surprises since the 2008-09 financial crisis.

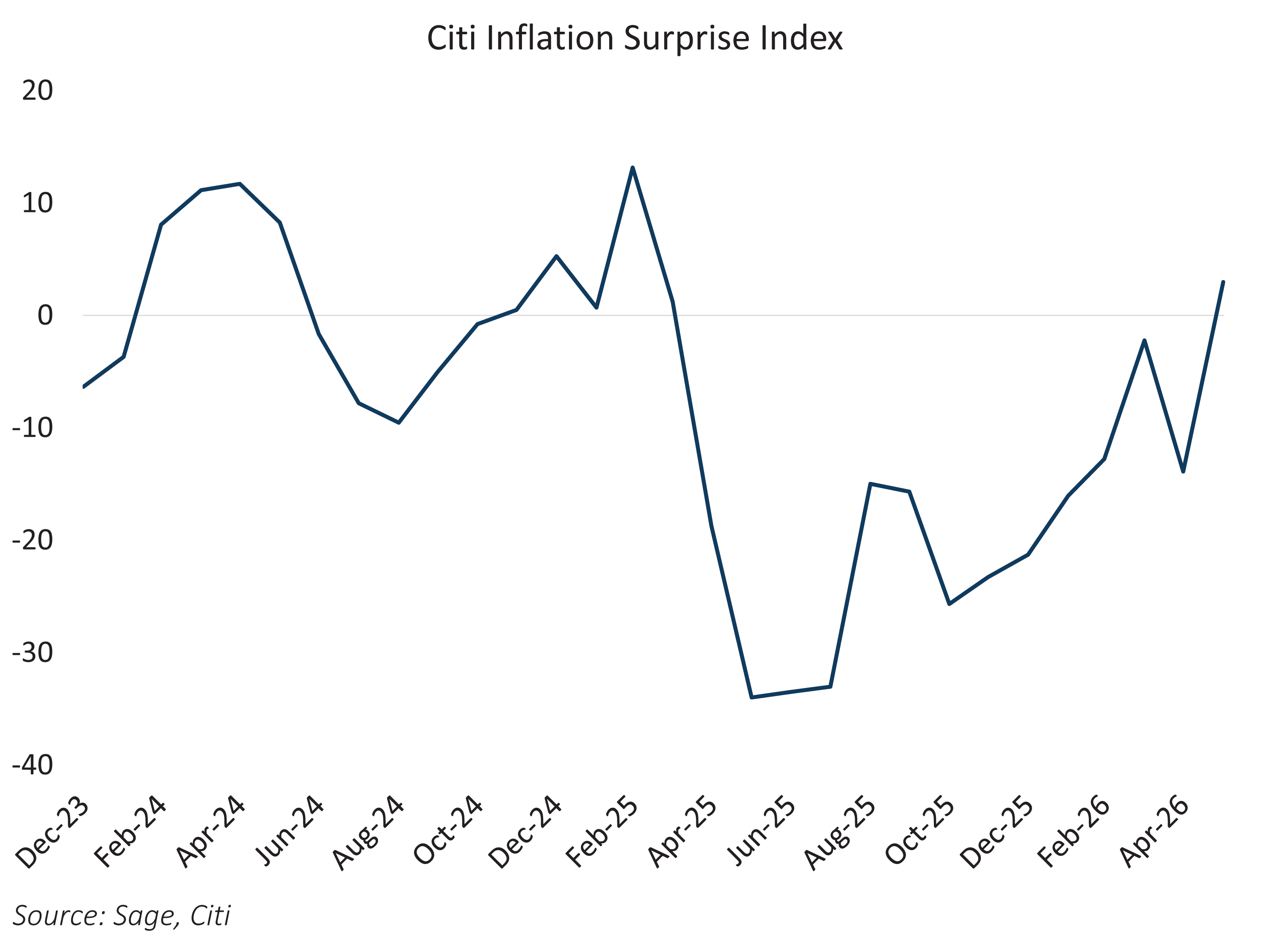

Inflation surprises are also at a local high relative to expectations. April CPI came in at 3.8% year-over-year, up sharply from 3.3% the prior month, driven largely by a 17.9% annual surge in energy costs and a 28.4% jump in gasoline prices.

This week brings labor data via Nonfarm Payrolls on Friday. The last two months have seen outsized prints — March at 178K versus a consensus of negative 6K, and April at 115K against expectations of roughly 62K to 90K. The pace is running at a level that will keep the unemployment rate from rising. This week’s number, if the trend continues, will point to a strong labor market that complicates the case for easing.

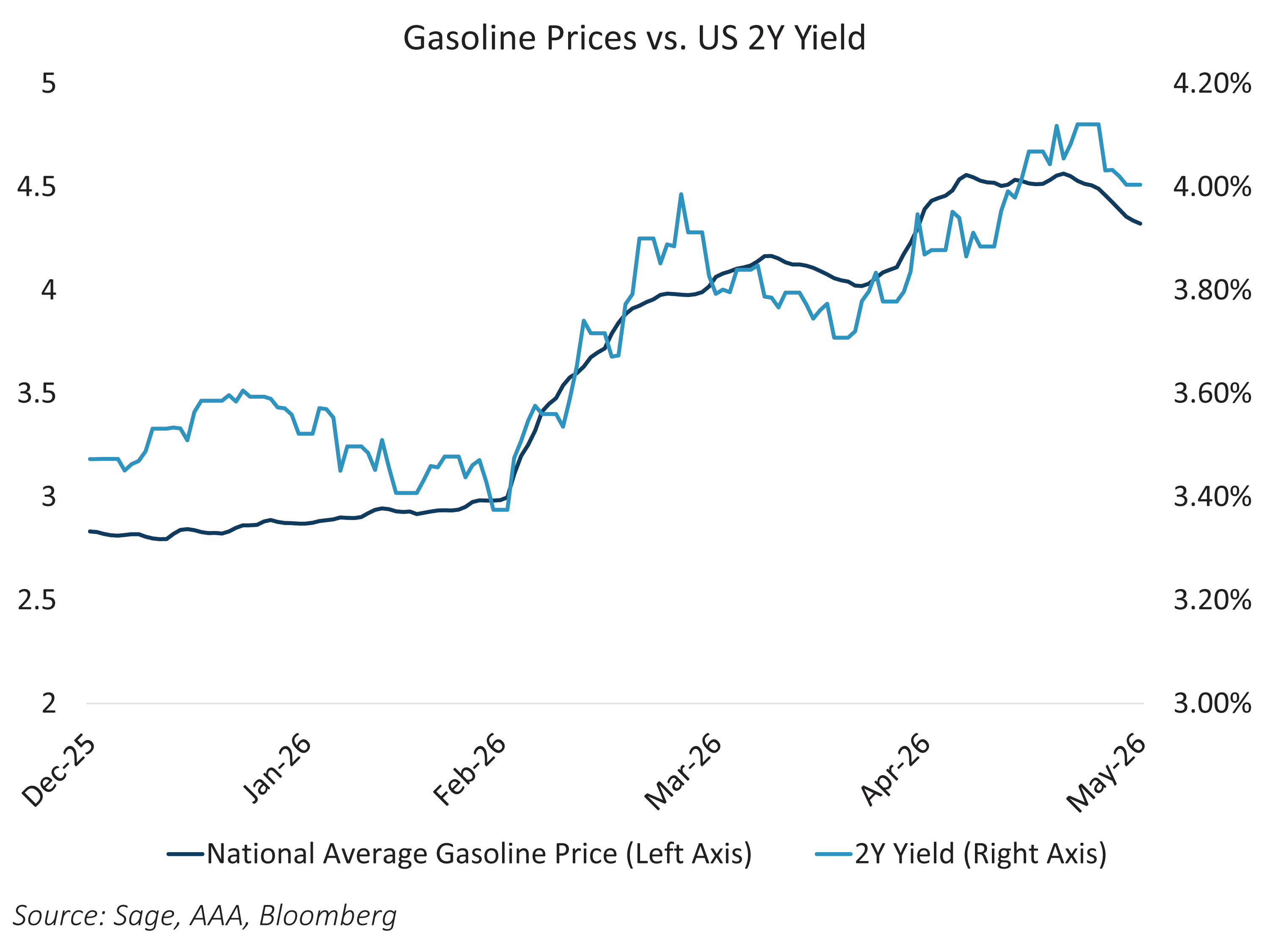

However, gasoline prices remain elevated due to the Strait of Hormuz shutdown. The national average sits near $4.32 per gallon, up roughly 54% from pre-conflict levels at the end of February. The chart below shows the national gasoline average price versus the US 2-year Treasury yield, which tracks closely. Until the Strait of Hormuz situation is fully resolved, rates — particularly on the short end — will have to price in an inflation risk premium and remain elevated.

Chairman Warsh will have a tough line to toe during his first FOMC meeting. He has been vocal about eliminating forward guidance, framing it as a constraint on the Fed’s ability to respond dynamically to changing economic conditions. During his April confirmation hearing, he stated plainly that he does not believe in it and proposed ending or modifying the Fed’s quarterly dot plot projections, arguing they pre-commit the committee to a course of action and reduce policy flexibility. He favors a rules-based framework that is transparent in its logic but deliberately opaque about its next move. Meanwhile, the April FOMC minutes revealed a majority of participants acknowledged that rate hikes will likely become appropriate if inflation continues to run above 2%, underscored by four dissents at the April meeting. Market pricing now reflects roughly a 30% probability of a hike in 2026, leaving risks more evenly balanced ahead of this meeting. Upcoming labor market and inflation data, along with a potential resolution of the Strait of Hormuz shutdown, could provide greater clarity, though uncertainty will likely persist.