The Iran war has become the dominant macro variable driving markets through its impact on global energy prices and the transmission to inflation and aggregate demand. While investors continue to debate growth, central bank timing, and credit fundamentals, oil has emerged as the central lens through which risk is priced. In fixed income, corporate credit spreads are moving as a function of energy prices.

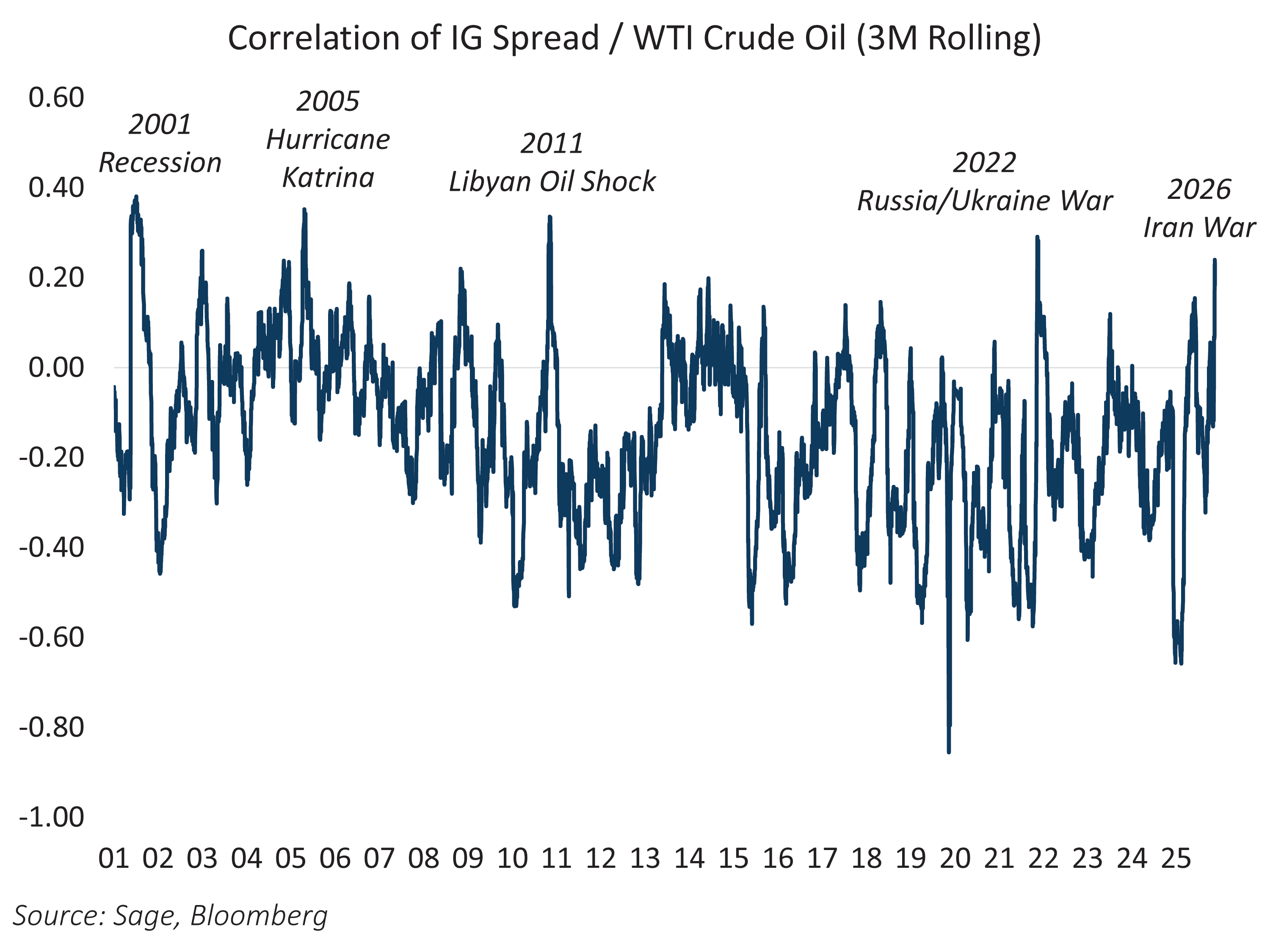

The link between oil and credit spreads is not new, but the relationship has intensified. Spikes in the correlation between corporate spreads and oil prices tend to occur during periods of energy disruption or macro stress. Similar dynamics appeared during the 2001 recession, the 2005 Katrina-driven disruption to Gulf oil infrastructure, the 2011 Libyan oil crisis, and the 2022 Russian invasion of Ukraine.

What distinguishes the current episode is not the size of the oil move, but the absence of a clear end point. While the prior episodes did not see correlations staying elevated, the Iran War presents an open-ended risk to the global energy supply, with limited visibility into de-escalation or offsetting production. For fixed income markets, credit spreads are now responding to oil’s implications for inflation persistence, central bank reaction functions, and the durability of aggregate demand. Until there is clarity on the scope and duration of the energy shock, oil is likely to remain the key macro variable linking geopolitics to credit pricing. With corporate credit spreads still at historical tights and uncertainty around systemic risk in private credit, layering an energy shock on top argues for caution in reaching for credit risk.