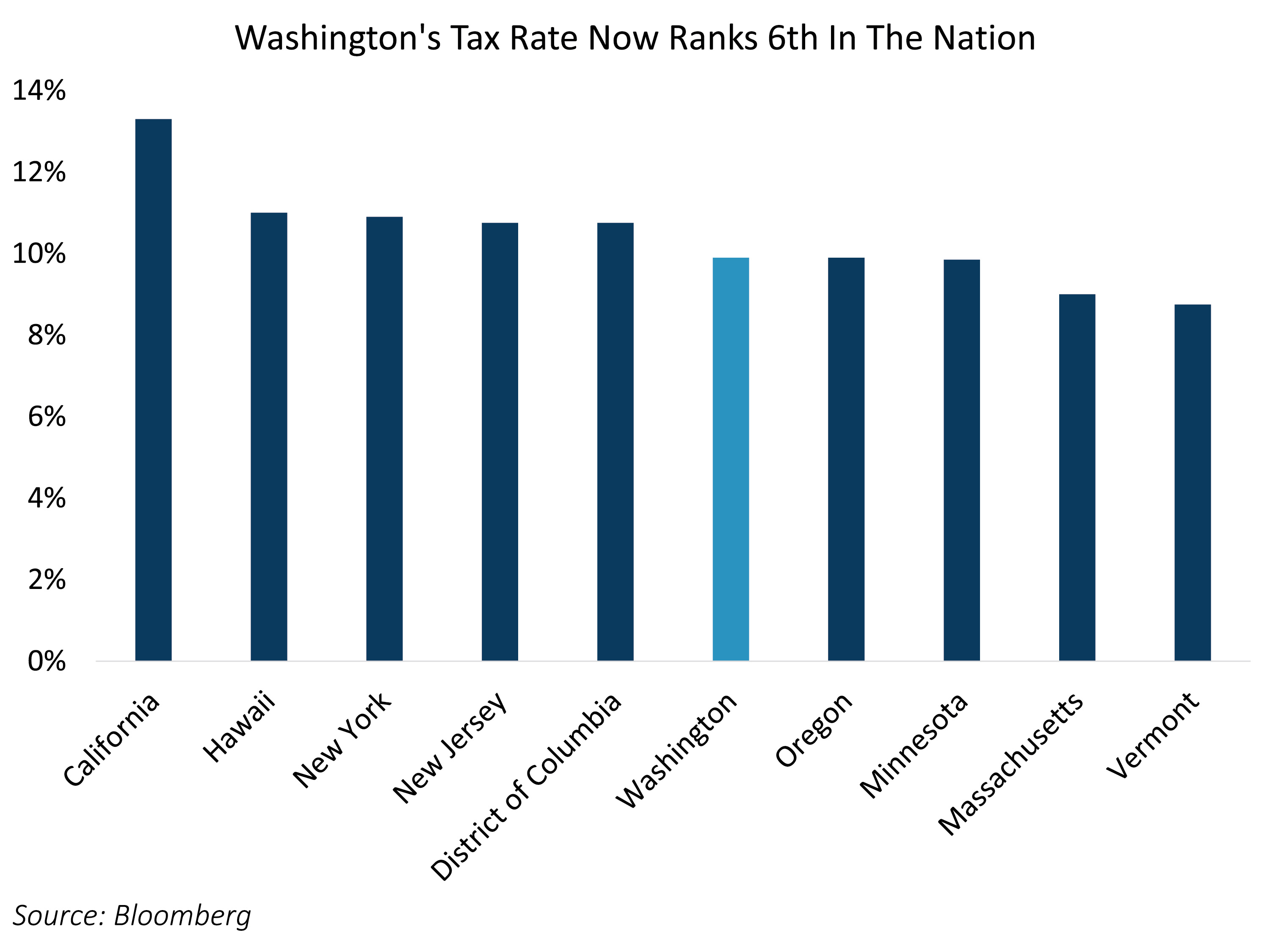

On March 30, Washington Governor Bob Ferguson signed Senate Bill 6346 into law, establishing a 9.9% state income tax on annual earnings above $1 million. Long known as one of the few states without an income tax, Washington will now rank among the highest marginal tax jurisdictions in the country for high earners. While the legislation raises concerns about potential business dislocation and population outflows, it also meaningfully increases the relative attractiveness of Washington‑issued municipal bonds for individuals now subject to the “millionaires’ tax.”

In‑State Bond Ownership Can Now Deliver Meaningful Value

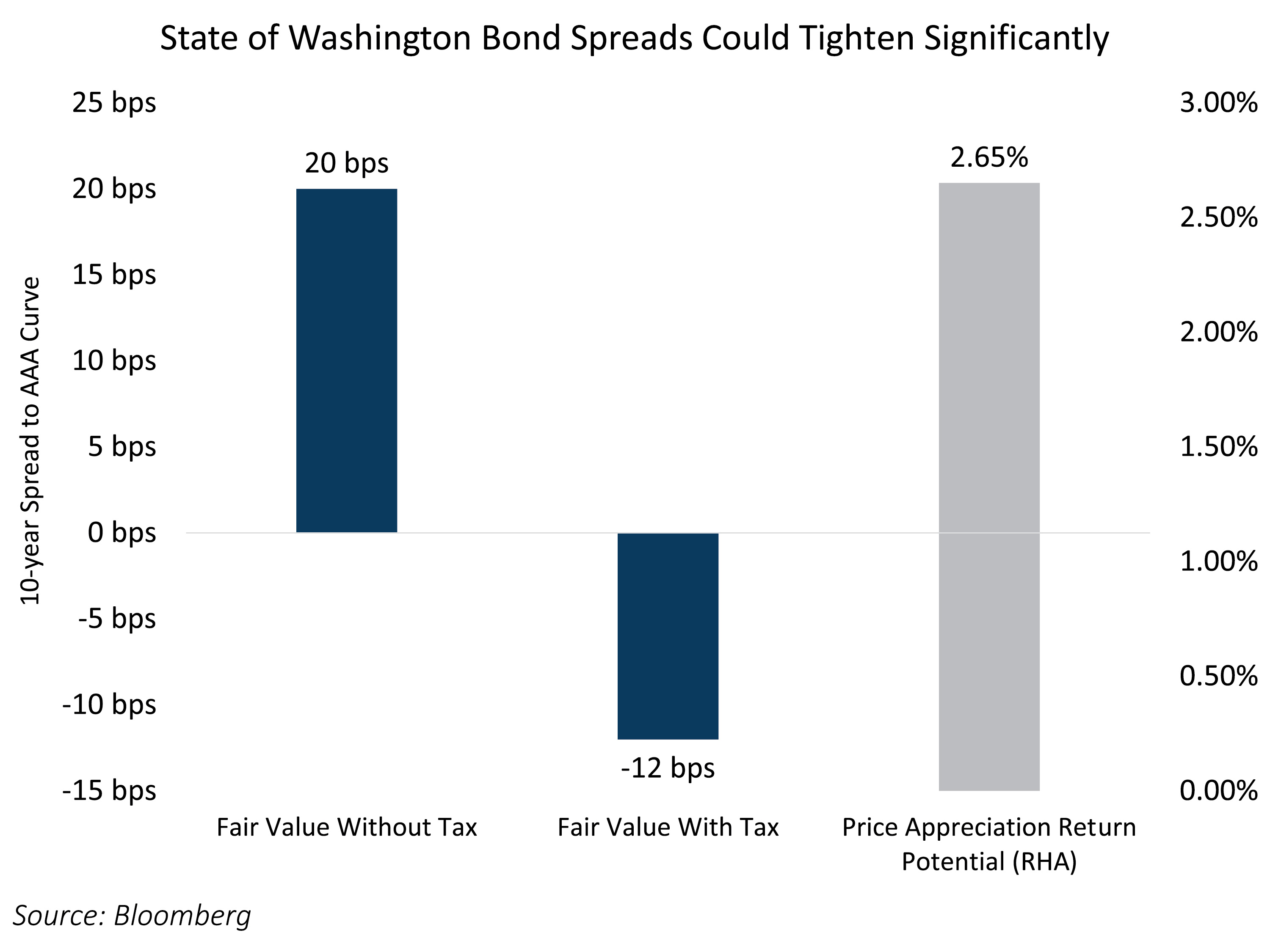

Historically, Washington municipal bonds lacked a natural in‑state buyer base due to the absence of state income taxes, leading investors to demand marginally higher yields to hold the state’s bonds. By contrast, in higher‑tax states, in‑state municipals typically trade at tighter spreads to reflect the value of the state tax exemption—one reason bonds issued in New York and California frequently trade at negative spreads to the AAA municipal benchmark.

With the introduction of a new tax on high earners, we expect demand for Washington municipal bonds to increase over the next 12–18 months as residents seek to improve the tax efficiency of their fixed income portfolios. Importantly, Washington municipals have not yet priced in the impact of the new tax regime. Currently, Washington State general obligation bonds trade at spreads of approximately 20 basis points, in line with historical norms. However, those spreads could compress materially—potentially to as tight as negative 12 basis points. This dynamic creates an opportunity for Washington residents to benefit from tax‑free income, while both in‑state and out‑of‑state buyers may also realize meaningful price appreciation if spreads begin to fully reflect the value of the new in‑state tax exemption.

Tax Policies Are Becoming More Polarized

State income tax policy has diverged sharply across the country. Over the past five years, 23 states have reduced income tax rates, while a smaller group has moved in the opposite direction—largely along partisan lines. To navigate this increasingly polarized tax landscape, Sage offers both state‑preferred and state‑specific municipal strategies, allowing investors to allocate between 40% and 100% to in‑state bonds. With valuation dynamics now shifting in Washington, a higher in‑state allocation may be increasingly attractive for affected residents.