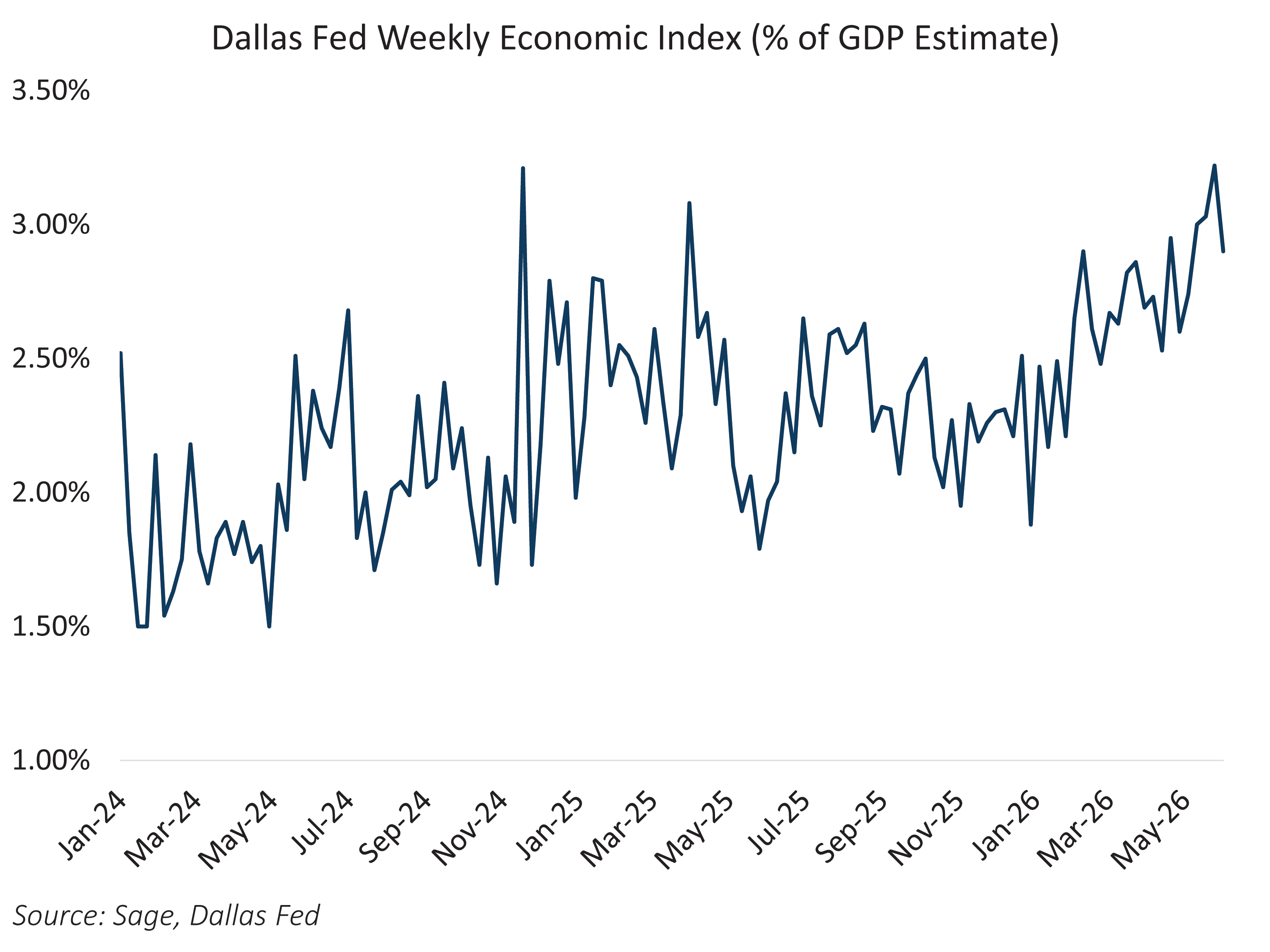

The US/Iran agreement to reopen the Strait of Hormuz clears the geopolitical overhang that drove markets for the past several months, and attention shifts squarely to the most consequential event of the summer: the first FOMC meeting of the Warsh era. It will be no easy task to calibrate monetary conditions to the mix of forces shaping the economy. The committee faces strong underlying growth alongside inflation that was elevated by higher oil prices, though those pressures are now easing as the Hormuz developments filter through energy markets. The Dallas Fed Weekly Economic Index, which forecasts 1-year ahead growth, currently sits at 2.9%.

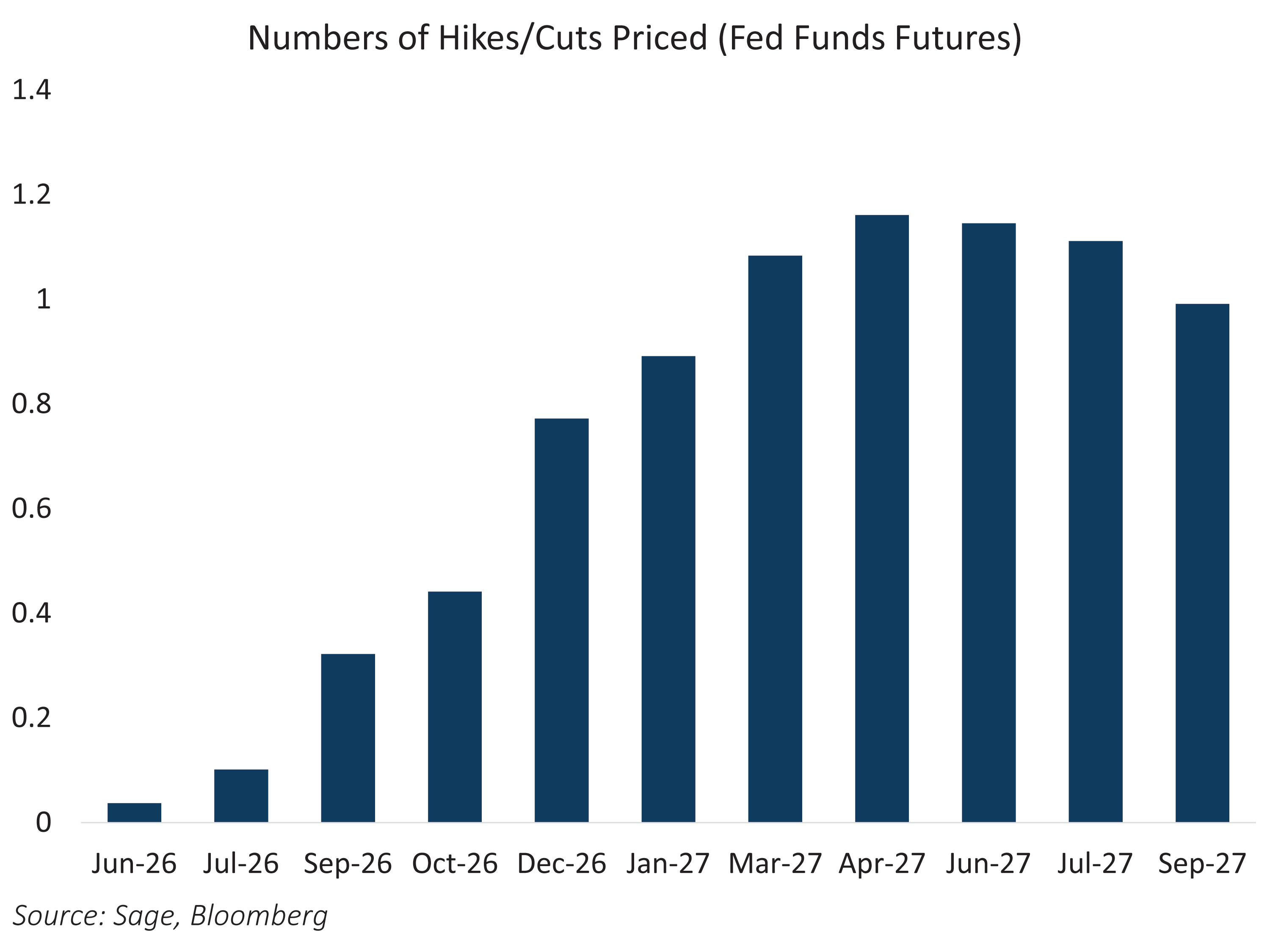

Interest rate markets had priced in one full rate hike by year-end, but expectations have pulled back in the wake of the deal. Markets now point to one 25-basis-point hike by March 2027, reflecting the view that easing energy prices take some near-term urgency off the table. Growth has not slowed, the labor market continues to run above breakeven, and even with oil retreating, the cumulative pass-through from months of elevated energy costs has not fully unwound. It could be too early to call victory on inflation, especially given the recency of the US/Iran deal.

Given the strength of the data and the prevalence of inflation risks, we expect the Warsh committee to emphasize the “price stability” side of its dual mandate. We expect the FOMC to leave the fed funds rate unchanged, with the dot plot signaling a hike by the end of 2026 and the Summary of Economic Projections pointing to higher inflation expectations relative to the March meeting. While hawkish relative to the prior meetings, this outcome is largely priced into interest rate markets.

The wildcard will be the press conference. Warsh has made no secret of his opposition to forward guidance, viewing it as a constraint on policy flexibility. Still, reporters are likely to press him on the timing and conditions for a hike, as well as whether the Hormuz agreement changes the inflation calculus. Warsh will have to thread the needle – acknowledging incoming data and reinforcing the FOMC’s decision without committing to a path for upcoming meetings, which could induce some near-term volatility in rates.