Halfway through 2026, the fixed income story hinges on one word: inflation. Gasoline prices and wages are cooling, but the broader inflation picture remains stubbornly above the Fed’s 2% target — and new FOMC Chair Kevin Warsh has been explicit that price stability is his north star. That backdrop has driven long-term yields higher this year, but the move is a Fed story, not a fiscal one. Meanwhile, AI-driven capex is powering the real economy and fueling record corporate bond issuance, all of which is being readily absorbed by yield-hungry buyers. Our positioning reflects a rangebound-rates environment where all-in yields are high enough to work for investors — even as spreads sit near the tights. We remain constructive on carry, comfortable owning duration at these levels, and selective in credit, favoring high-quality spread sectors like MBS that offer income without stretching for risk.

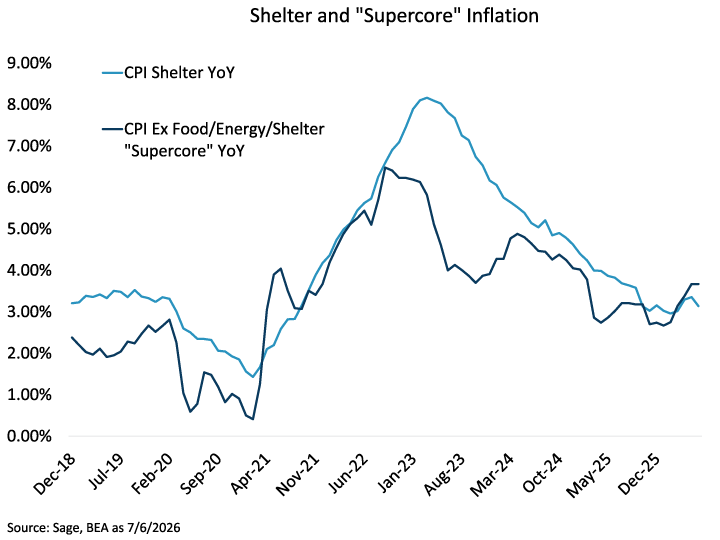

Broader Inflation Has Ticked Higher in Recent Months

Two of the less-volatile components of the inflation basket — CPI Shelter and “Supercore” (CPI ex Food, Energy, and Shelter) — have stopped declining and have started to drift higher in recent months, which warrants caution. Headline relief from lower gasoline prices is welcome, but the slow-moving pieces of inflation are what drive Fed policy and remain above target. Until we see prices roll over convincingly, we expect the Fed to lean hawkish, keeping rate volatility elevated. Advisors should anchor portfolios in the belly of the curve, where carry is attractive without taking maximum rate risk.

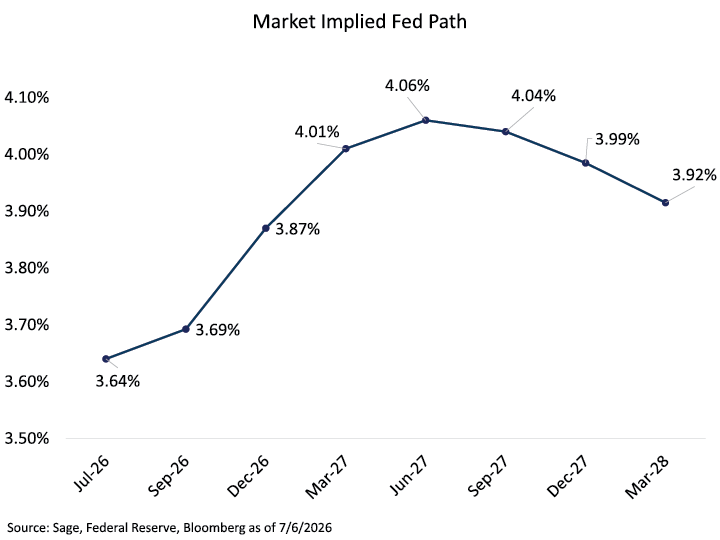

Markets Take Warsh’s Focus on Price Stability at Face Value — With 2 Hikes Priced

The market-implied Fed path now peaks at roughly 4.06% by mid-2027, up from 3.64% today — pricing in approximately two rate hikes through 2027. Chair Warsh’s first FOMC meeting reset expectations. Markets are taking his price-stability pledge seriously, as reflected in market pricing. This regime shift establishes a higher-for-longer floor under front-end yields, which advantages income-oriented clients. Short and intermediate fixed income should benefit as the reinvestment risk that dominated 2024–2025 has largely faded.

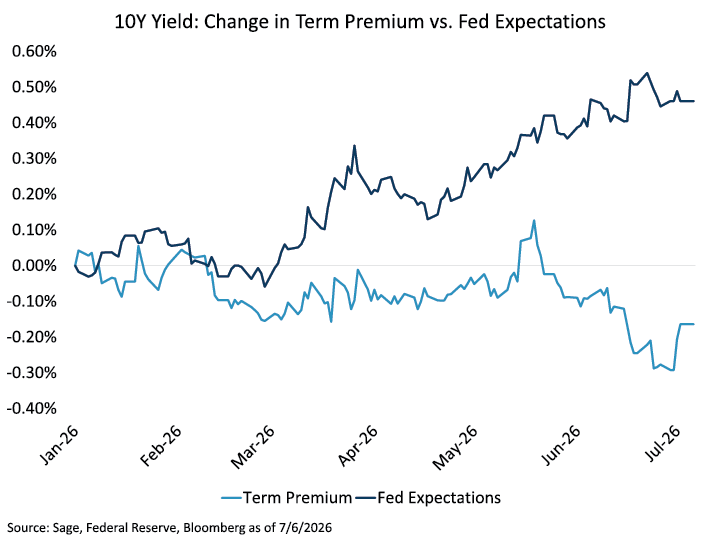

Higher Long-Term Rates Reflect a Fed Shift — Not Fiscal Concerns

Decomposing the rise in the 10-year Treasury yield in 2026 into its two drivers — Fed expectations vs. term premium — reveals that essentially all of the move higher this year is attributable to shifting Fed expectations. Term premium (the piece that would reflect supply/deficit concerns) has actually declined. The major factor affecting the shape of the yield curve this year has been the repricing of Fed policy rather than concerns around fiscal sustainability and bond issuance. As long as inflation remains the dominant concern, this dynamic should hold, and rates should stay rangebound at slightly elevated levels rather than spiraling higher on supply fears. It’s the foundation of our “don’t fear duration” stance for the back half of the year.

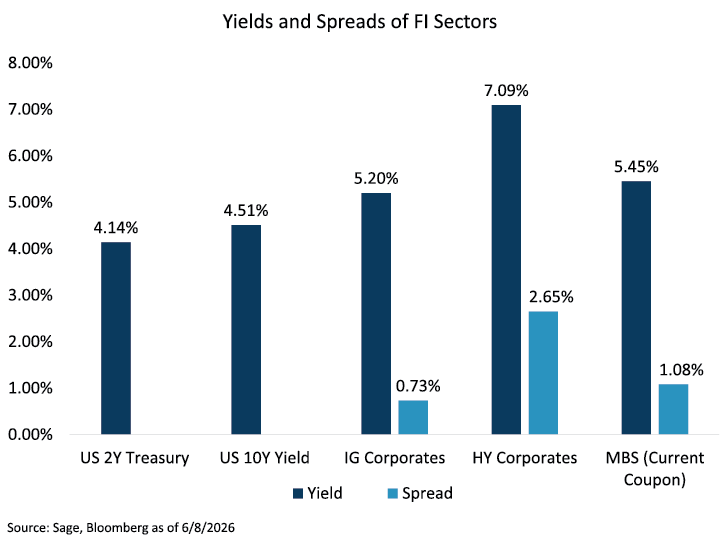

High All-In Yields Are Attracting Investors Despite Tight Spreads

Across the fixed income complex, yields are compelling — IG Corporates at 5.20%, HY at 7.09%, MBS current coupon at 5.45% — even though spreads on IG (73 bps) and HY (265 bps) sit well inside long-term averages. This chart captures the paradox of today’s market. Spreads look tight in isolation, but all-in yields are the highest they’ve been in nearly two decades, which attracts continued inflows into the asset class. While spread compression may be limited from here, absent a systemic event, the high level of yields should continue to drive bond returns. Within credit, we favor higher-quality names where the yield give-up is minimal, and we see MBS as particularly attractive — investors are getting a spread near its 10-year average (109 bps vs. 110 bps) at a time when nearly every other sector is trading rich.

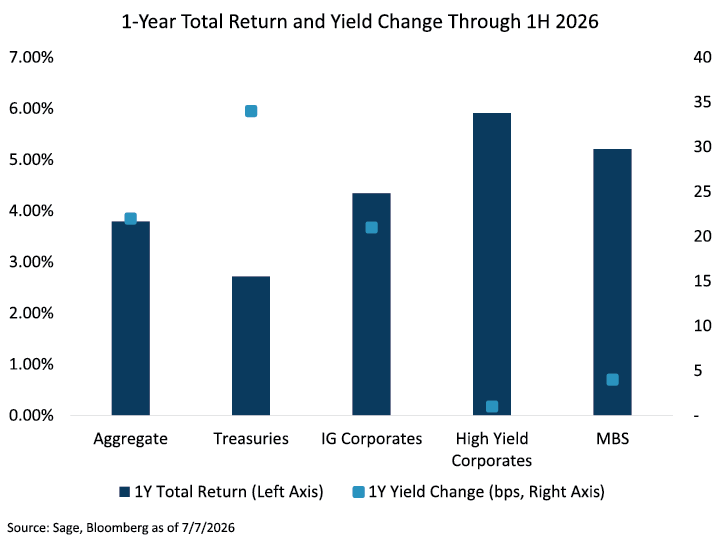

Despite Flat-to-Rising Yields, Fixed Income Returns Remain Solid

Over the past 12 months, even as yields have been flat-to-modestly higher across the curve, every major fixed income sector has posted positive total returns — with High Yield leading (~5.9%), MBS close behind (~5.2%), and IG Corporates (~4.3%) and the Aggregate (~3.8%) all delivering solid outcomes. In a world where yields have remained stable and spreads are tight, starting yields were high enough to absorb modest price volatility and still leave investors with meaningful total return. Notably, MBS has performed nearly as well as High Yield with a fraction of the credit risk, which is exactly why we’ve been leaning into the sector. For advisors, the message to clients is simple: you don’t need a rate rally to make money in bonds right now — you just need to stay invested and let the coupon compound.