Weekly Market Recap

The municipal market experienced limited yield movement around the FOMC meeting, with year-end supply influenced by historical Federal Reserve actions. December supply has varied in past years, affected by rate hikes, cuts, and tax legislation, such as the 2018 tax package that accelerated nearly $70 billion in issuance in December 2017. Recent years showed muted year-end activity, with 2022’s tightening cycle resulting in only $20 billion of volume and 2024 ending with $31 billion amid cumulative rate cuts.

This year’s late-year supply is more active, supported by favorable curve slopes and issuer-friendly yields, with premarketing indicating steady spreads and some alternate couponing structures tailored to investor demand. Notable issues include a $2 billion University of California bond with 5¼–5½% coupons and Texas A&M University bonds using discount structures for 30-year maturities. The Education, Healthcare, and Electric Power sectors saw the largest year-over-year supply increases.

Market Activity

BWIC volumes rose 18% above the five-week average last week, with a hit ratio slightly above average. Bid-wanted volumes increased across most duration and ratings categories, with mixed sector volume changes, including significant rises in Electric Power and State GO. Coupon volumes mostly increased in higher coupons while zero-coupon volumes declined. Traded yields on purchases generally improved across sectors and coupons.

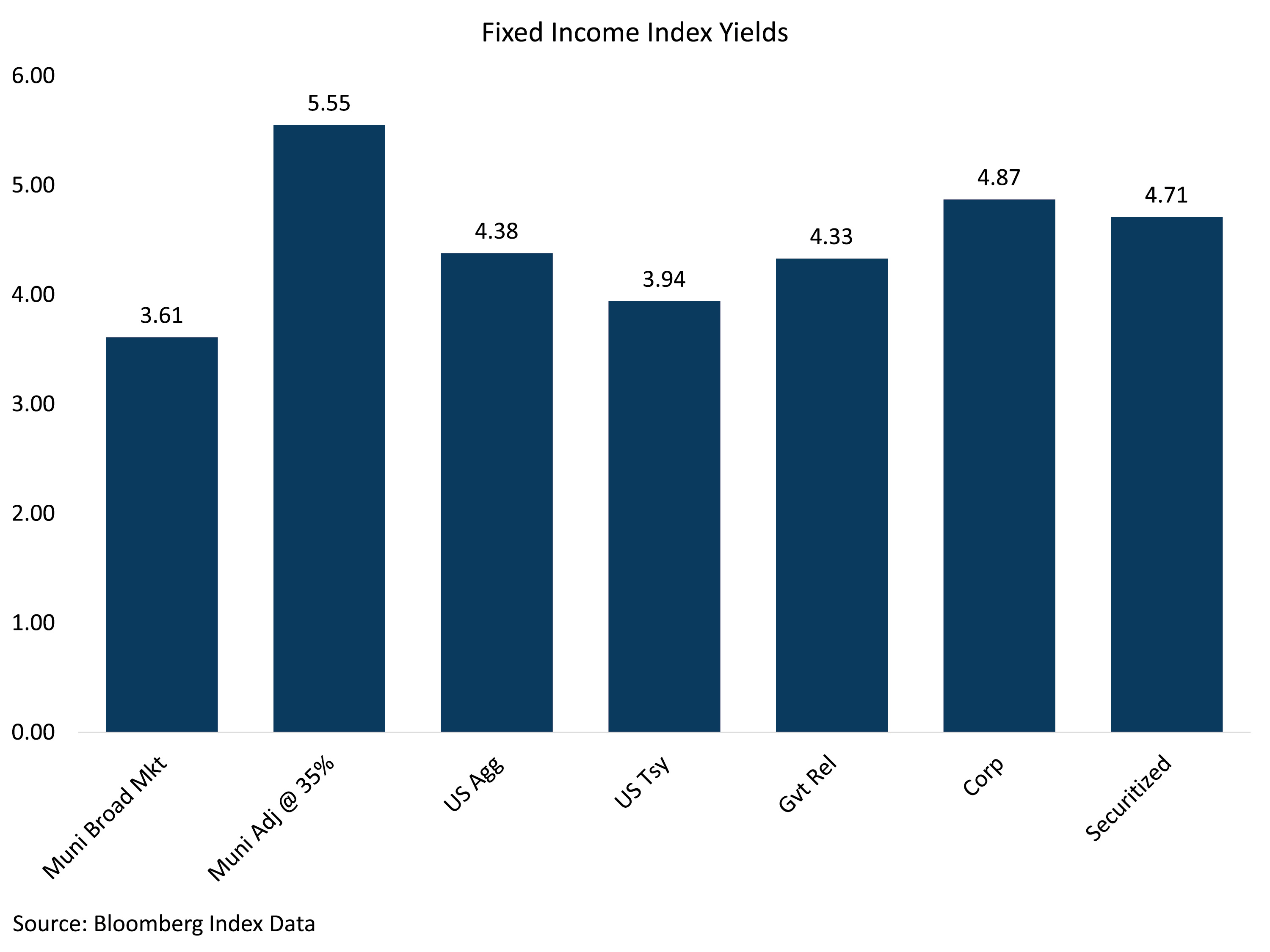

Year-to-date gross supply reached $546 billion, 15% above 2024 and 29% above the five-year average. Tax-exempt supply totaled $499 billion, up 14% over 2024 and 49% above the five-year average, whereas taxable supply of $47 billion was 32% higher than 2024 but 46% below the five-year average.

Taxable-Equivalent Yield Advantages in High-Tax States

High-tax states like California offer strong credit quality and favorable taxable-equivalent yields (TEYs), providing price protection. For example, University of California bonds yielded 2.72% on 10-year maturities, significantly outperforming Texas A&M University bonds with a TEY near 6.00%, more than 100 basis points above Texas equivalents. The TEY advantage is even greater in 15-year maturities. Local credits in these states are particularly valuable due to scarce over-allocations and negative spreads to AAA reference spots, reflecting strong demand for tax-exempt status.

Municipal Credit Outlook

Standard and Poor’s highlights potential headwinds for certain sectors in 2026, noting a 30% chance of recession. State and local general obligation (GO) bonds have shown resilience historically, with stable outlooks but caution for governments that have spent down surpluses and school districts with lower reserves dependent on state funding. During the 2008-09 recession, state and local GOs underperformed the broader market, while in the brief 2020 recession, GO bonds outperformed, aided by federal aid and employment recovery. Current 2025 returns show state credits gaining 4.3%, while local GOs returned 3.9%, slightly below the broad market. Lower credit quality bonds may face more risk in economic downturns, as indicated by the single-A rated muni index trailing the broad market by 400 basis points during 2008-09.