Global markets stood on edge as the conflict in Iran upended energy markets and muddied the outlook for the global economy. Interest rate markets repriced as market participants processed the notion that hostilities and the closure of the Strait of Hormuz could last longer than expected. Entering the year — prior to direct US/Iran conflict — the growth, inflation, and policy mix was viewed as a “goldilocks” environment. This was marked by moderate economic expansion, declining inflation, and a Fed on track to cut rates, alongside the risk that cuts could be deeper if the labor market weakened further, and little to no probability assigned to near‑term interest rate hikes. With the introduction of an oil shock, the “right tail” — the possibility of a rate hike — has entered market pricing. Market volatility has created opportunities for active positioning.

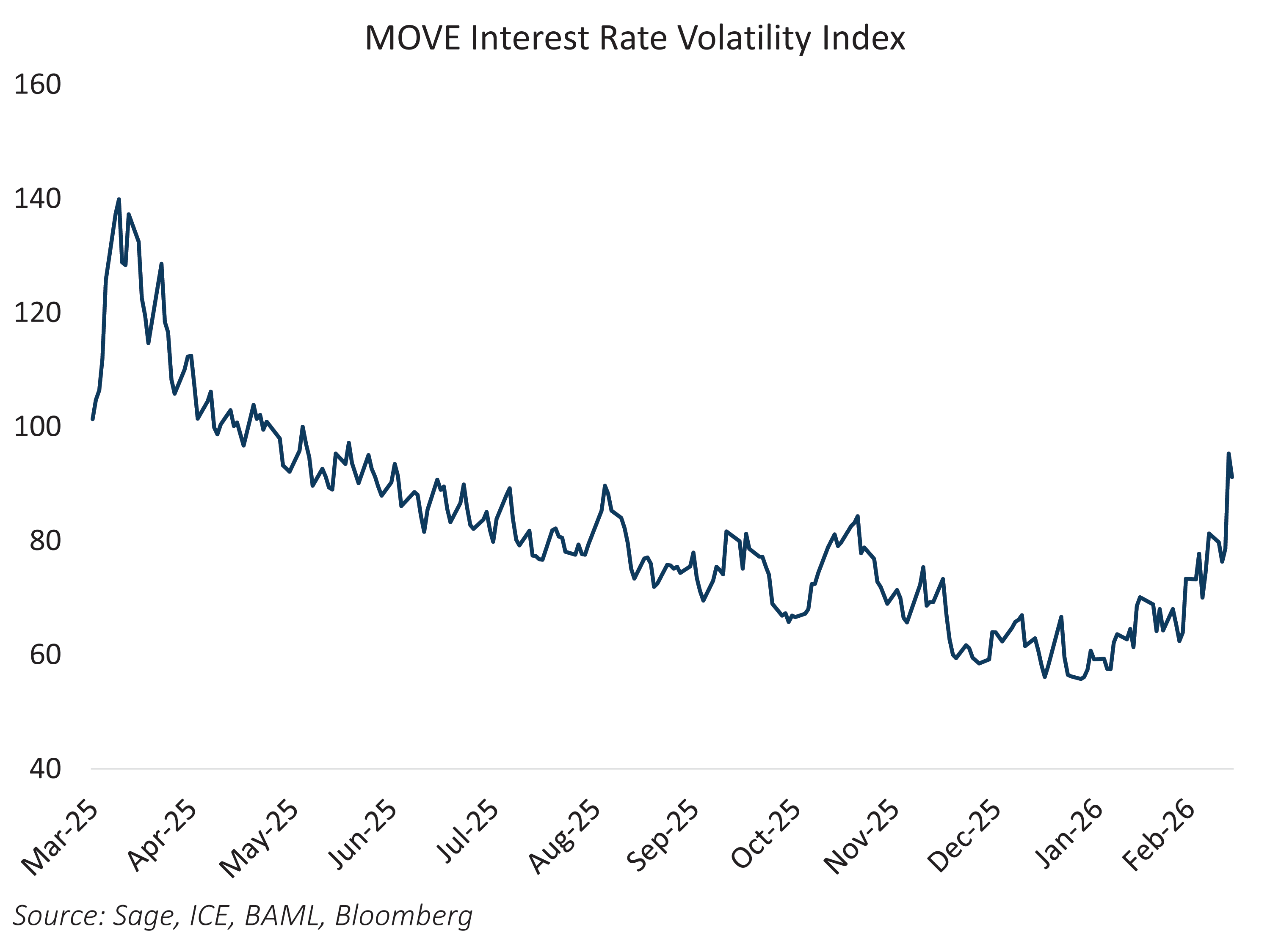

Interest rate markets continue to price rate cuts this year, with one 25 basis point cut from the Fed priced through January 2027, though the range of potential outcomes around that path has widened. Rate volatility has increased, reflecting uncertainty around inflation dynamics and policy reaction. The MOVE Index, which tracks implied volatility in interest rate markets, has risen in recent weeks after a period of decline following Liberation Day, signaling renewed uncertainty around the rate outlook.

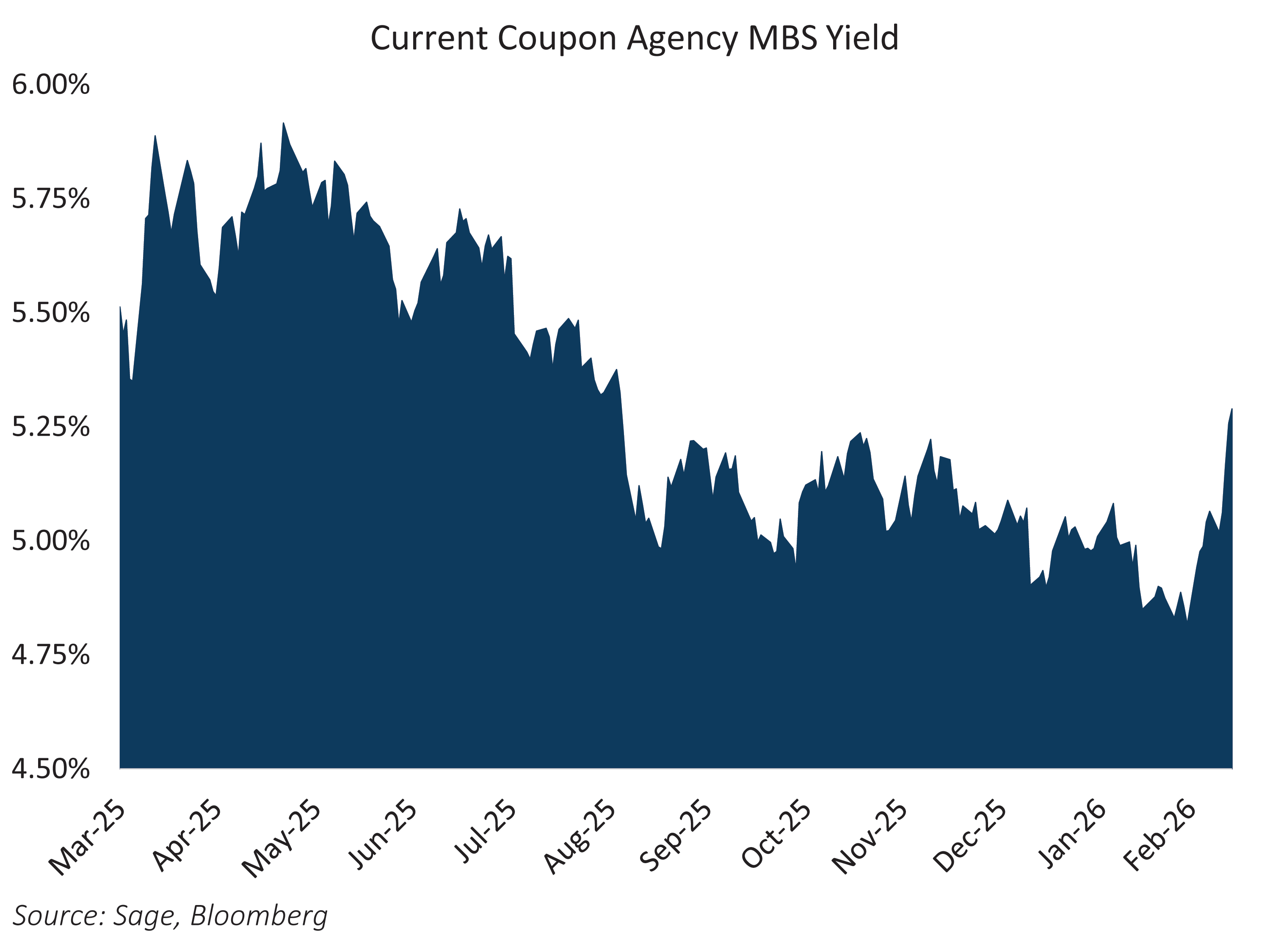

As discussed in prior Notes from the Desk, periods of rising interest rate volatility tend to pressure agency MBS, given the prepayment option embedded in the structure and the resulting negative convexity. This episode has followed a familiar pattern, with MBS underperforming after a strong stretch of outperformance in the back half of 2025. The accompanying chart shows yields on current coupon agency MBS rising alongside the increase in Iran‑driven interest rate volatility, reflecting both higher rate uncertainty and wider spreads.

The recent cheapening in MBS represents an opportunity rather than a shift in trend. While an oil shock will weigh on end‑consumer spending, the inflation impact remains constrained, as shelter carries greater weight in the inflation basket and continues to trend lower. At the same time, downside risks to growth persist, with labor market softness and credit concerns remaining present across the economy, reinforcing the case for the Fed to remain on hold or stay the course in modestly lowering rates.