Last week’s central bank decisions reinforced the end of the global rate-cutting trend, a view we highlighted in a prior note. On Thursday, the Bank of Japan (BOJ) raised its benchmark interest rate by 25 basis points to 0.75%, marking its highest level since 1995. Japan’s steady rate hikes come after ending its negative interest rate policy last year. The central bank is trying to curb inflation, which has stayed above its 2% target for nearly four years, while managing concerns about tighter financial conditions amid a large stimulus program.

Against this backdrop, other major central banks are signaling different paths. At its December meeting, the European Central Bank (ECB) kept rates unchanged, as widely expected, but surprised markets by upgrading its growth outlook — raising the possibility that its next move could be a hike after a pause. The ECB’s rate-cutting cycle appears to be over. Meanwhile, the Bank of England cut rates as expected, though the decision was narrowly split at 5-4. While the overall direction remains toward easing, the BOE indicated that future cuts will be a ‘closer call.’

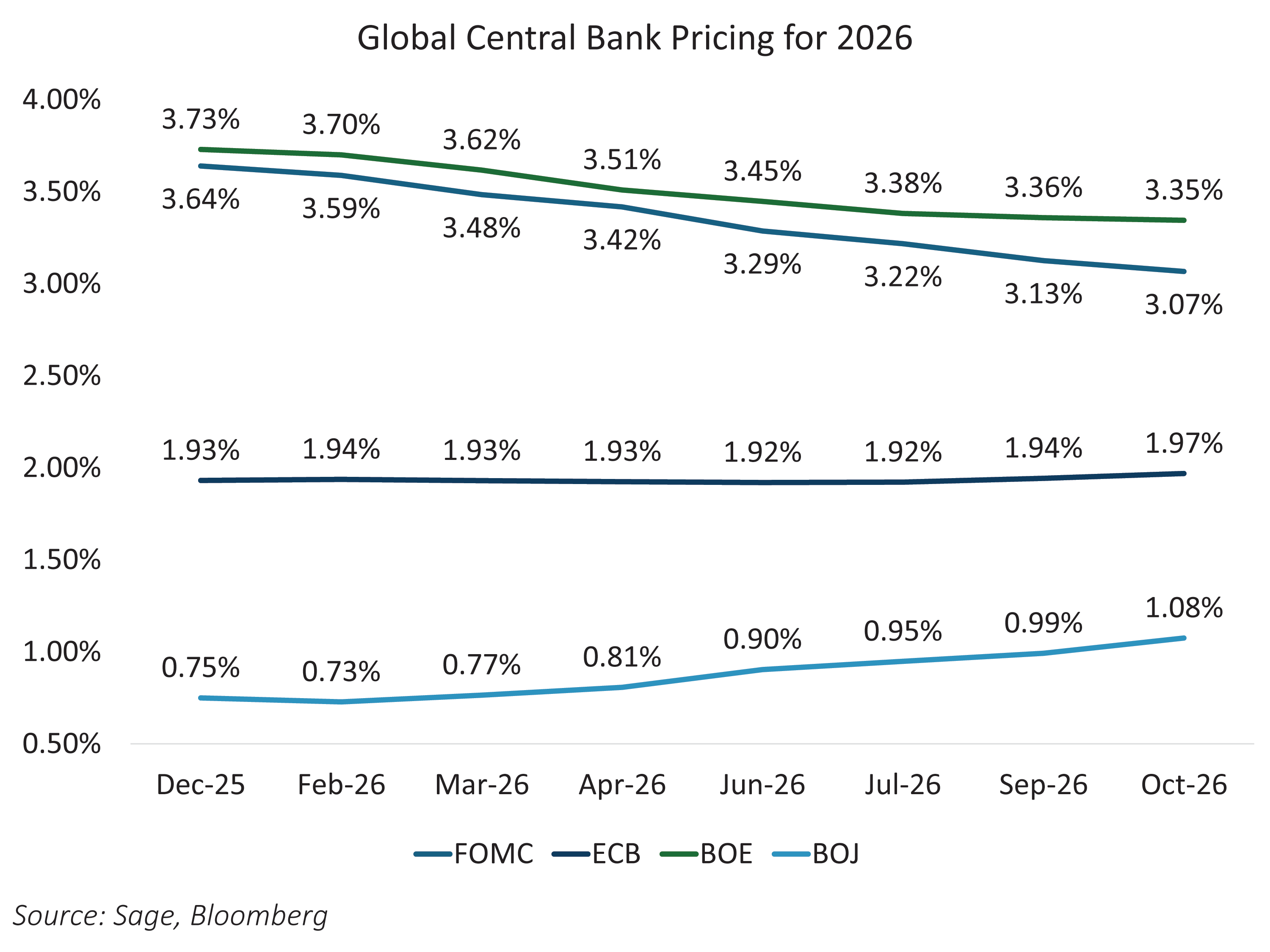

As we look ahead to 2026, surveying central bank pricing across the world’s major economies will provide a useful baseline for expectations. Global policy rates should remain stable next year as central banks pause to assess the impact of recent cuts in an environment of limited fiscal restraint.

Viewing the cross section of central bank expectations is clear — policy rates are expected to move very little next year. The fed funds rate is currently in the 3.5% to 3.75% range, and interest rates markets are pricing two additional cuts next year to around 3.0%. The BOE is priced for one additional rate cut, and the ECB is expected to be on pause for all of 2026. The BOJ is expected to hike rates by 25 bps next year.

As we move into 2026, monetary policy will likely take a back seat, with fiscal concerns coming to the forefront — especially as the US approaches midterm elections in November. The economic backdrop remains expansionary, and inflation continues to trend lower in the US, while Europe and Japan face the challenge of economies that may be running too hot. For fixed income investors, this environment points to a “coupon year” — a period when returns are driven primarily by the income, or coupon, from bonds rather than price appreciation. With policy rates expected to remain stable and limited room for further rate cuts, capturing yield will be key, and investors should focus on building portfolios that can harvest steady income as the main driver of total return.